The shift from professionalism to commercialism in the

auditing profession

“Everything in our society is commercialized”

MASTER THESIS WITHIN: Business Administration – Accounting & Marketing NUMBER OF CREDITS: 30 ECTS

PROGRAM OF STUDY: Civilekonom

AUTHORS: Liza Bruze & Weng-San Angie Lee

TUTOR: Mart Ots

ii

Abstract

Title: The shift from professionalism to commercialism in the auditing profession Authors: Liza Bruze & Angie Lee

Tutor: Mart Ots Date: 2020-05-18

Key Terms: “Auditor’s perceptions”, “Marketing Activities”, “Professionalism”, “Commercialism”

Background: The auditing profession is in constant change and marketing activities such as advertising has gone from being prohibited to become a legal activity within the profession. The Swedish auditing profession has for a long time been protected by laws and regulations. With the increased use of marketing activities in the profession, researchers claim that the profession has shifted from professionalism to commercialism. Research has argued the positive and negative outcomes of increased marketing activities within the profession where the auditors have had mixed perceptions regarding this increase.

Purpose: The purpose of this thesis was to examine Swedish auditors' perceptions toward the shift from professionalism toward commercialism within the auditing profession.

Method: By using a qualitative research methodology six (6) semi-structured interviews with active auditors in Sweden were conducted. In-depth empirics were collected where an inductive approach was adopted to approach the data collected.

Conclusion: Seven themes of perceptions were identified: (1) Marketing as a tool in a more competitive market, (2) Marketing should be used for brand awareness, (3) Marketing is not my responsibility, (4) Auditing is a trust profession, (5) The most important marketing tool is the word of mouth, (6) Seeing clients is not marketing, and (7) Marketing activities do not affect the professionalism. It was found that marketing activities had been perceived to become more positively accepted overtime where the auditors implied that duality between professionalism and commercialism should be applied.

iii

Acknowledgments

The authors are sincerely grateful for the many individuals who have engaged in the progress of this thesis.

Firstly, we would like to give our sincere gratitude to the auditors who set their time aside to make the completion of this thesis possible in uncertain times of COVID-19.

Secondly, we would like to thank our supervisor Mart Ots for his guidance and appreciated advice during the development of this thesis. He has been very helpful, and his advice has improved this thesis greatly. The same goes for our fellow students who have given us valuable insights and constructive criticism during our seminars.

Liza Bruze Weng-San Angie Lee

Jönköping International Business School May 2020

iv

Table of Contents

1. Introduction ... 1 1.1 Background: ... 1 1.2 Problem ... 3 1.3 Purpose ... 4 1.4 Research question ... 4 1.4.1 Research Question ... 4 1.5 Disposition ... 5 1.6 Delimitation ... 5 1.7 Definitions ... 5 2. Literature review ... 7 2.1 Audit Profession ... 72.2 Professionalism and Commercialism ... 9

2.2.1 Professionalism ... 10

2.2.2 Commercialism ... 10

2.3 Marketing in the Accounting Profession ... 12

2.4 Auditor’s perceptions toward marketing activities ... 14

2.5 Relationship marketing ... 17 2.6 Technology ... 18 3. Methodology ... 19 3.1 Research philosophy ... 19 3.2 Scientific method... 19 3.3 Approach ... 20 3.4 Research design ... 20

v

3.4.1 Exploratory research design ... 20

3.5 Data Collection ... 21

3.5.1 Sampling ... 21

3.5.2 Interviews ... 22

3.5.3 Interview guide ... 24

3.5.4 Pilot Interview ... 25

3.5.5 Presentation of the interviewees ... 25

3.6 Data Analysis ... 26

3.6.1 Data processing... 27

3.7 Protection of Personal Data ... 28

3.8 Trustworthiness ... 28 3.8.1 Dependability... 28 3.8.2 Credibility ... 29 3.8.3 Transferability ... 29 3.8.4 Confirmability ... 29 4. Findings ... 31

4.1 Marketing as a tool in a more competitive market ... 31

4.2 Marketing should be used for brand awareness ... 32

4.3 Marketing is not my responsibility... 34

4.4 Auditing is a trust profession ... 35

4.5 The most important marketing tool is the word of mouth... 36

4.6 Seeing clients is not marketing... 38

4.7 Marketing activities do not affect the professionalism ... 39

vi

5.1 Marketing as a tool in a more competitive market ... 41

5.2 Marketing should be used for brand awareness ... 42

5.3 Marketing is not my responsibility... 43

5.4 Auditing is a trust profession ... 44

5.5 The most important marketing tool is the word of mouth... 44

5.6 Seeing clients is not marketing... 45

5.7 Marketing activities do not affect the professionalism ... 46

6. Conclusion and Discussion ... 48

6.1 Conclusion ... 48

6.2 Implications ... 49

6.2.1 Theoretical implications ... 49

6.2.2 Managerial implication ... 49

6.2.3 Ethical and societal implications ... 50

6.3 Limitations ... 51

6.4 Future Research ... 51

References ... 53

Appendix ... 61

1

1. Introduction

The following section presents the background to our thesis and then evolves into a problematization. These parts are underpinned by the purpose which will be given at the end of this chapter.

1.1 Background:

In 1977, two young auditors in the US were charged for violating the auditors’ code of ethics when they advertised their services in a local newspaper (Ellingson, Hiltner, Elbert & Gillett, 2001). The American Institute of Certified Public Accountants (AICPA) clearly stated in its Code of Professional Conduct (Code) that advertising is prohibited within the profession.

“A member shall not seek to obtain clients by solicitation. Advertising is a form of solicitation and is prohibited.” (Ellingson et al., 2001, p. 69).

However, due to similar cases in other professions and outside pressure, the Supreme court ended up ruling in favor of the two auditors. This resulted in a rewrite of the rule where advertising was no longer a violation of the auditor’s professional code, but direct solicitation of clients was still prohibited (Ellingson et al., 2001).

“A member in the public practice shall not seek to obtain clients by advertising or other forms of solicitation in a manner that is false, misleading, or deceptive. Solicitation using coercion, overreaching, or harassing conduct is prohibited.” (Ellingson et al., 2001, p. 70).

As advertising activities have been prohibited within the profession, this has not affected the Swedish auditors much as all limited companies in Sweden have been required to perform an audit. However, the law of statutory audit for all limited companies in Sweden was abolished in November 2010, which affected around 250 000, or 72%, of the Swedish limited companies (Prop. 2009/10:204). The abolishment of the statutory audit requirement implied that small limited companies in Sweden were able to choose whether they wanted to perform an audit or not. The reason for the abolishment was for the government to provide smaller companies with a better

2

opportunity to succeed in the competing market (SOU 2008:32). On the other hand, this meant a major setback for auditors who had been practicing in a market where job opportunities were the least of their issues. The abolishment of the statutory audit implied that auditors had to find new ways to attract clientele as they were no longer a certainty for most companies. This entailed auditors to focus more on marketing activities and maintaining relationships to convince their clients to keep the auditing service (Broberg, Umans & Gerlofstig, 2013).

The abolishment of the statutory audit requirement in Sweden in 2010 applied to all small limited companies under the presumptions that at least two of the following three requirements were met for two consecutive years:

• On average, not more than three employees

• Assets that do not exceed 1.5 million Swedish crowns. • Revenue that does not exceed 3 million Swedish crowns. (Bolagsverket, 2018)

The number of audits performed decreased after the implementation of the abolishment as many newly founded limited companies in Sweden chose to not include an audit in their financials, unless they had expansion plans. According to an authorized auditor who is a member of the Institute for the Accountancy Profession in Sweden, FAR (Föreningen Auktoriserade Revisorer), implied that the decrease in the number of audits performed might have been due to the lack of marketing activities by auditors that explains the necessity of performing an audit to the public (Neij, 2017). It was predicted that the banking industry would demand audits from companies that applied for a loan to strengthen the information provided on their financial statements (Neij, 2017). This in turn would keep the number of audits performed stable despite the abolishment. However, as the banking industry has not seen the necessity of demanding an audit from the limited companies, the actual number of audits has decreased. Hence, most of the small limited companies that existed before the abolishment have chosen to keep the audit, whereas newly founded companies have not found the necessity in hiring an auditor (Neij, 2017).

3

The abolishment of statutory audit in Sweden for small limited companies has made auditors more aware of marketing activities to stay competitive on the market. A change in the auditors’ professional code of conduct and a developing market has resulted in more marketing activities within the auditing profession. In addition, some researchers imply that this change in the profession has resulted in a shift in the market where the auditing profession has moved from professionalism to a commercialized market. A shift from professionalism to a commercialized market implies that auditors are today more focused on self-serving economics rather than focusing on the interest of the public (Guo, 2016).

1.2 Problem

Marketing activities are receiving more recognition as tools for auditors and firms to compete on the market. This is especially applicable since accounting firms are following the regulations and policies of the profession which have not been accepting toward certain marketing activities.

According to Broberg et al. (2013) a dilemma has arisen due to a balance where auditors must maintain a close relationship with their clients while at the same time uphold the professional values. Prior studies by Clow, Stevens, McConkey, and Loudon (2009), Ellingson et al. (2002), and Heischmidt et al. (2002) have researched the factors of marketing activities and auditors' attitudes towards the shift in the profession. However, these studies are dominated by quantitative measures which lacks a deeper understanding and insight of auditor’s perceptions.

Increased marketing activities have been argued to affect different aspects of the auditing profession such as shifting the profession toward commercialism. Researchers (Imhoff, 2013; Wyatt, 2004; Zeff, 2003a, 2003b; Palepu and Healy, 2003; and Healy and Palepu, 2003) are concerned that focus on less typical marketing activities such as the use of marketing professionals and advertising could decrease professionalism. Hence, more research is needed as the perspective of professionalism and commercialism in Sweden is scarce.

4

1.3 Purpose

Most of the existing literature has studied the accounting profession in the US. Therefore, the purpose of this thesis was to examine Swedish auditors' perceptions toward the shift from professionalism toward commercialism within the auditing profession.

As researchers have explored auditor’s perceptions toward marketing activities and argued for a shift in the profession from professionalism toward commercialism, no research has to our knowledge studied the auditor's perception of the shift in the profession from a professionalism-oriented market toward becoming a more commercially professionalism-oriented market. Studies such as Broberg, Umans, and Skog (2018) have conducted a study to conceptualize commercialization in the Swedish audit profession by quantitative measures. However, none of the research to our knowledge have gone to ask the professionals in the Swedish profession how they perceive the shift in the market using a qualitative study.

This thesis could be of importance as it will aim to assist with understanding and reasoning behind auditor's motivation in the use of marketing activities. Increased use of marketing activities within the profession might cause a conflict between an auditor and the society’s perception of what is acceptable and not within the restrictions of the profession (Guo, 2016; Liesegang, 2008).

1.4 Research question

1.4.1 Research Question

“What are auditors’ perceptions of marketing activities as the auditing profession shifts from professionalism to commercialism?”

1.4.2 Perception

A belief or opinion often held by people and based on how things seem (Cambridge Dictionary, n.d.).

5

1.5 Disposition

The remainder of this paper is structured such that we present delimitations and definitions before presenting literature regarding the accounting profession and the view on marketing activities. The paper then continues to present the method chosen, a short presentation of the interviews conducted, and an analysis of the interviews. The last part of the paper includes a discussion, conclusion, and suggestions for future research.

1.6 Delimitation

The study focused on auditors in the Jönköping area, where all auditors were of interest. The reason for not only choosing authorized auditors who have been working in the profession for a longer time, and who might have had more knowledge regarding the increased use of marketing activities, was to receive a broader perspective on the issue from auditors with different backgrounds. Many studies have implied that younger professionals who have just entered the market have historically been more accepting of marketing activities (Broberg et al. 2013). Therefore, the mix between authorized and non-authorized auditors were of interest as they contributed different knowledge and expertise to the subject.

1.7 Definitions

Accounting Profession = Auditing Profession Public (certified) Accountant = Auditor

Authorized Auditor = Certified Auditor

Accounting firm = Auditing Firm

Big 4 firm = PwC, Deloitte, KPMG, EY

Perception = A belief or opinion often held by people and based on how things seem (Cambridge Dictionary, n.d.). Auditor → Generalized to the profession, can be both authorized

6

and non-authorized auditor.

7

2. Literature review

The following chapter will review the existing theory about professionalism and commercialism in the auditing profession and examine what previous studies have found regarding auditor’s perceptions regarding marketing activities. The chapter covers the impact of marketing activities from previous literature in the auditing profession.

2.1 Audit Profession

The main purpose of the audit started due to the separation between investors and managers concerning the dependence of capital (Öhman & Wallerstedt, 2012). Investors required assurance of well-managed capital if they were to invest in new companies. Therefore, auditors are hired by clients to review their financial statements where the auditor is expected to be independent and provide an unbiased evaluation (Guo, 2016). Hence, the role of an auditor is to verify the accounting information prepared by the management. This is to enhance the credibility of the financial statements and to detect and report misstatements in the company’s accounts (Watts & Zimmerman, 1986; Elizabeth DeAngelo, 1981). By verifying the accounting information, the auditor can enhance the credibility of the company’s financial statements toward outside investors. A key element in measuring the quality of an audit is by determining the auditor’s independence. According to Wines (2011) independence is described as:

“Independence in fact exists when auditors are actually able to act with objectivity, integrity, impartiality and freedom from any conflict of interest” (p.7).

Some research has implied that independence is a key attribute within the profession (Gendron, Suddaby & Lam 2006).

Guo (2016) argues that the independence of an auditor might be biased if the auditor is financially dependent on their client since auditors are hired to examine the financial accounts of their clients toward outside investors. The independence of an auditor is vital to the public’s confidence as the auditors are the ones with the power of detecting misstatements in the financial accounts. If the

8

independence of an auditor is compromised, this affects the whole auditing profession in a negative way (Arya & Glover, 2014). The independence of an auditor could also directly affect their reputation and professionalism as the quality of their previous audits will come into question (Arya & Glover, 2014). This can be seen from historical cases of corporate fraud, such as Lehman Brothers and the Enron scandal where the auditors have not detected or reported cases of misstatements in the financial accounts by their clients. Corporate fraud scandals such as the previous mentioned, will most likely also reduce the value of the auditor’s services (Watts & Zimmerman, 1986). Therefore, Selling (2015) indicates that professionalism needs to be reasserted over commercialism.

A study by Herda and Lavelle, (2013) investigated auditor's commitment to clients where the findings revealed that value-added audit services were important as the clients seek information and recommendations beyond the core audit service. Perceived fair treatment from clients induces a social exchange between the auditors and the clients. Further, high-quality relationships between the auditor and the client tend to lead to a higher quality of service beyond the classical requirements of the audit itself.

The difference between a “regular” auditor and an authorized or certified auditor in Sweden is that an authorized- or certified auditor has more knowledge in the subject compared to a “regular” auditor. To become authorized, an auditor in Sweden must perform three years of theoretical studies and at least three years of practical studies at an accounting firm with a supervisor before taking a test at the Swedish audit inspection (FAR, n.d.; Revisorinspektionen, n.d.). After the test have been approved, the auditor can identify themselves as an authorized auditor (Revisionsinspektionen, n.d.). The authorized auditors are then qualified to perform audits on all types of companies, whereas a “regular” auditor has certain restrictions on what types of companies they can perform audits on. The differences mainly lay with middle- and large-sized limited companies where only an authorized auditor can perform the audit (FAR, n.d.).

9

2.2 Professionalism and Commercialism

Research implies that the accounting profession is constantly changing following the regulatory, social, and economic environment where the profession is operating (Gunz & Thorne, 2017). Accounting firms have noticed a shift from professionalism to commercialism as they are today more obliged to please the clients in their demands (Ketz, 1996; Picard, Durocher & Gendron, 2014; Suddaby, Gendron & Lam, 2009). The profession has also attracted young professionals to the industry which have contributed to the shift of the profession as the young professionals have not been operating in the profession when certain marketing activities have been prohibited and therefore are more open toward the idea of performing marketing activities (Broberg et al. 2013).

Professionalism signifies serving the interest of the public whereas commercialism implies that auditors are more focused on the self-serving economics (Guo, 2016). Malsch & Gendron (2013) have argued that the shift from professionalism to commercialism has arisen due to the double institutional culture that the profession’s capacity allows for. The profession is on one end trying to preserve the professional legitimacy, whereas the other end is stepping outside the traditional boundaries of the profession to generate new sources of profits (Guo, 2016). As a result of this, auditors have been redefined as versatile experts due to the identity transformation of the profession (Picard, Sylvain & Yves 2018). Suddaby, Cooper & Greenwood (2007) argue that the protection and promotion of capital markets are today more valuable than the interest of the public, which has been a contributing factor to the shift in the profession.

A debate regarding whether the profession is more commercialized or professionalized has been discussed for a long time. Researchers imply that a conflict between audit quality and audit pricing exists, where audit quality represents professionalism, and audit pricing represents commercialism (Sweeney & McGarry, 2011). It has also been questioned whether the profession should uphold the traditional principles of staying “professional” or moving toward a more commercialistic profession (Liesegang, 2008).

10 2.2.1 Professionalism

Professionalism is usually characterized by certain attributes and distinguishing features of the profession such as acquiring special skills, pieces of knowledge, and a code of ethics (Barrainkua & Espinosa-Pike, 2018). Larson (1979) implies that professions, according to social scientists, refer to occupations with special power and prestige. This is because professions obtain certain knowledge and competence in areas that are connected to the central needs and values of the social system. The auditors are loyal toward serving the public and go beyond material incentives which imply that professionals work in a professionalized market. In contrast, Evetts, Muzio, and Kirkpatrick (2011) imply that sociologists define professionalism as differentiated as a special means of organizing work and controlling workers.

Nevertheless, Evetts et al. (2011) continue to argue that government projects to promote commercialized and organizational forms have changed the meaning of professionalism over time. Organizational methods, principles, and strategies affect and transform identities, structures, and practices of professions (Evetts et al., 2011). Continuity and change are two elements of professionalism that have been discussed as it is important to understand the changes that have been made, while at the same time considering what needs to remain for the professionalism to survive its occupational value. Another aspect that redefines the occupational value of professionalism within a profession, is the professional's interpretation of their work and their working relationships (Evetts et al., 2011). Evetts et al. (2011) also found that professional work can be viewed as commodification because the service products that are being offered are defined to be marketed, price-tagged, evaluated individually, and remunerated. Correspondingly, Gunz and Thorne (2017), and Zeff (2003a; 2003b) found significant evidence that commercialism is negatively and seriously impacting the professionalism in the accounting profession due to the constant need to deliver services.

2.2.2 Commercialism

The auditing profession has been argued to have shifted from professionalism to a commercialism-oriented market due to the profession’s focus on profitability and service, rather than on ethical

11

values (Wen, 2019). Gendron et al. (2006) conclude in their research that there is a decline in the auditing profession’s core ethical values. This is a result of growing greed within the profession according to Wyatt (2004) and Gendron et al. (2006). Freidson (2001) have argued that efficiency and profitability are the main objectives of an organization, whereas high-quality service is the main goal of the accounting profession. Sori, Karbhari, and Mohamad (2010), and Sharma and Sidhu (2001) implies in their research that commercialization in the profession has arisen due to non-audit services that are being offered by accounting firms in addition to the audit, such as consulting services. Since globalization and competition on the audit market have become fiercer, this has pushed accounting firms to offer non-audit services to differentiate themselves on the market which has become an increasing concern regarding auditor independence (Craswell, 1999; Quick & Ben-Rasmussen, 2005). Studies imply that the joint provision of audit and non-audit services offered by accounting firms compromises audit quality and independence (Sori et al., 2010). This is the result of a more commercialistic oriented target as firms are more focused on generating profits (Guo, 2016).

In contrast to the research question, “What are auditors’ perceptions of marketing activities as the auditing profession shifts from professionalism to commercialism?”, where it is implied that the profession has shifted to commercialism, some studies have argued that commercialism is not new within the profession, and rather imply that it is and have been part of the profession for a long time (Broberg et al., 2013). The study by Broberg et al. (2013) also argued that increased use of marketing activities has helped eliminate the distance between auditing and marketing activities in the profession.

According to Wen (2019) there is a research gap regarding the understanding of commercialism on the micro-level of auditors on an individual level. Wen (2019) examines the construction of the commercial self in a Big 4 accounting firm in China. Findings have indicated three different factors that are reappearing which include the client relationship, value-adding, and career to be dominant in constructing individuality of the personal brand in a Big 4 accounting firm (Wen 2019). The standardization of professionalism was described to rationalize the implementation of more commercialistic elements (Wen, 2019). In the Swedish auditing profession, there has been one

12

study by Broberg et al. (2018) who have tried to attempt to conceptualize commercialization in the context of Swedish accounting firms.

Friedson (2001) have discussed the negative associations of commercialization where firms are driven by profitability due to stakeholder needs. Friedson (2001) implied that in terms of commercialization, professional identity has a negative association because of the focus on the stakeholder need. The organizational identity, on the other hand, has a positive association with commercialization because it identifies with the financial gains and is driven by profitability (Friedson, 2001).

The abolishment of the statutory audit requirement in Sweden has been one contributing factor shifting the profession from a market-driving to a market-driven profession. The market-driving strategy implies taking customers, competitors, and a broader market condition into account (Wilden, Gudergan & Lings, 2019). Firms that are market-driving therefore proactively change the structures and behaviors of the market to improve their competitiveness by changing the conditions of the market, for instance through introducing new products. The market-driven strategy, on the other hand, focuses on the firm’s understanding and reaction to the want and needs of the customers within the given market (Wilden et al., 2019). Hanlon (1996) means that those operating in the profession: accounting firms and auditors, must be commercially aware to be able to operate the different strategies. Therefore, Hodges and Young (2009), and Broberg et al. (2013) argues that engagement in marketing activities are important in this profession where the use of pure business skills is crucial to keep existing clients, while at the same time attracting new ones (Jönsson, 2005).

2.3 Marketing in the Accounting Profession

Marketing activities and marketing of auditors have historically violated the auditor’s code of ethics (Clow et al., 2009; Heischmidt, et al., 2002). This has been regarded as immoral and unprofessional (Heischmidt et al. 2002), which is why auditors have relied heavily on networking and reputation to attract new clients (Ellingson et al., 2001). Ellingson et al. (2001) imply that

13

subtle techniques of marketing of services within the profession have existed long before there was a change in the code. The change of the code still had many auditors question the development of marketing their services due to the public perception of the profession (Brozovsky & Mautz, 1996). Auditors that had been practicing in the profession for a longer time, and especially those who practiced in large and established firms were reluctant toward applying marketing activities to their responsibilities (Dyer & Shimp, 1980; Clow et al., 2009). Marketing activities within the auditing profession has long been argued to affect audit quality, pricing, and the competition on the market negatively for authorized auditors (Brozovsky & Mautz, 1996). Clow et al. (2009) also found a significant number of auditors who believed that marketing of the profession would affect prices and therefore, also affect the quality and independence of the profession negatively.

Comanor and Wilson (1974) have concluded that it is hard if not impossible to foretell whether marketing activities would affect audit quality or not. The quality of an audit is based on whether any errors or irregularities are made, and if these errors and/or irregularities are being discovered. Therefore, it would be impossible to predict the quality of an audit before the conduction of the audit service (Comanor & Wilson, 1974). Hence, the reputation of an auditor might have a bigger impact on the quality provided by an auditor rather than their involvement in marketing activities. If there have been discoveries of errors or irregularities, the auditor that performed the audit might be perceived as performing a lower quality service in comparison to an auditor that has not been discovered with errors or irregularities in the performed audits.

Furthermore, there has been a significant increase in the use of marketing activities within the auditing profession since the lift of the ban in the auditors’ Code of Professional Conduct. Marketing activities have slowly grown into becoming more and more accepted over time, both among those working in the profession but also among those outside the profession (Brozovsky & Mautz, 1996). As most auditors would agree to the positive effects of the increased use of marketing activities within the profession, this has also raised questions about whether the increased competition that marketing activities have generated has impacted the auditor’s professionalism and objectivity. Studies by Imhoff (2013), Wyatt (2004), Zeff (2003a, 2003b), Palepu and Healy (2003) and, Healy and Palepu (2003) have shown that auditors have become

14

more competitive due to the deregulation of advertising activities within the auditor’s code of ethics. The concern has then led to speculations regarding whether this has contributed to a loss of professionalism in the accounting profession due to the audit failures of detecting corporate fraud around the world. Imhoff (2003) argued that the deregulation of advertising services within the profession resulted in a negative shift where costs were cut, audits were streamlined, and audit services turned into a commodity. Additionally, marketing activities have been considered to obtain high costs, appear unprofessional toward the client and more importantly, the costs of conducting marketing activities were outweighing the benefits of conducting them (Clow et al., 2009). Comanor and Wilson (1974) implied that marketing is a substitute for higher quality goods by lower quality producers and therefore, allows for a decrease in market efficiency and consumer utility. Other studies have indicated that marketing activities, such as advertising, have been regarded as untruthful by consumers as it attempts to persuade people into consuming unnecessary goods and services (Calfee & Ringold, 1994).

As marketing activities are taking a larger part in the auditor’s professional responsibilities, the question regarding how the audit services should be marketed have been discussed. It has been implied that the best way to market professional services such as auditing services should be the equivalent to the marketing of tangible goods such as food, cars, or coffee machines (Ellingson et al., 2001). Whereas the other end has argued that there is a difference between the marketing of goods and that of services. Therefore, it has also been debated whether the value of the service changes the marketing strategy, and if it does, different strategies should be implemented toward the marketing of different professional services (Ellingson et al., 2001). Strategies to market auditing services should not be the equivalent to marketing of banking services. Hence, the marketing of professional services cannot be generalized over various professions (Ellingson et al., 2001).

2.4 Auditor’s perceptions toward marketing activities

A year after the Supreme Court ruling of the ban on advertising in the auditing profession, a study was conducted that showed that only 7 percent of certified public accountants (CPA:s) in the US

15

had any intentions of performing any marketing activities (Markham, Cangelosi & Carson, 2005). One of the reasons for this low number was due to the negative perceptions that accountants had toward marketing activities, but also due to the negative impact it might bring to their image and credibility by the public (Clow et al. 2009). According to a study performed in 1991, half of the accounting firms that had been in business for more than ten years in the US implied that they would never conduct any marketing activities. The study also showed that there was a much higher ratio of marketing activities within accounting firms that had started their business after the ban on advertising was lifted (Ott, Andrus & Ainsworth, 1991). It is argued that younger accounting firms and younger auditors had a different view when it came to the combination of the auditing profession and marketing activities. Auditors that had been practicing for a longer time still believed that advertising was against their code (Broberg et al., 2013). The younger auditors that had not experienced the rule before 1978, had not regarded this dilemma and instead viewed this as a great opportunity to strengthen their image (Ott et al., 1991). Eventually, auditors have acknowledged marketing activities as an essential tool for the success of the firm (Ellingson et al., 2002). Smith and Smith (1998) implies that the necessity of auditors to market their services was widely acknowledged among accountants according to a study ten years after the ban was lifted. However, marketing activities must be performed professionally to not cross the fine line that exists between the two activities to stay professional.

A positive change in the auditors’ attitudes toward the marketing of their services has been acknowledged. There has been a shift where the accounting profession for many years had a prohibition against advertising as it was considered unethical because auditors should attract customers with their professionalism (Jönsson, 2004; Clow et al., 2009). The abolishment of the Swedish law regarding marketing activities together with a positive change in auditors' attitudes toward marketing has generated the increased use of marketing activities such as the use of marketing professionals, advertisement, and marketing tools (Clow et al., 2009). Further, it has created new opportunities within marketing activities which have increased the auditor’s awareness of marketing their services (Tang, Moser, and Austin 2002; Clow et al., 2009). According to Ellingson et al. (2002) auditors believe that marketing plays an important role in the accounting profession both now and in the future. Auditors value marketing as an important

16

success factor of the firm where there is a need for auditors to be personally involved in the marketing process (Ellingson et al., 2002). Further, the study indicated that marketing with personal contact was more successful than advertising activities. This statement aligns with Moser, Colvard, and Austin’s (2002) argument that marketing is relevant to some extent when providing information, but most clients have still chosen to depend on the factors; reputation and referrals to appoint an auditor. Therefore, auditors need to understand the consumer’s attitudes and beliefs concerning their marketing efforts. The main suggestion for auditors is to provide the clients with information about services offered and conducting a strong image in marketing (Moser et al., 2002).

Positive attitudes regarding marketing activities have as previously mentioned, not always been regarded in this way. After the ban was lifted on advertising activities, auditors were very skeptical toward conducting marketing activities as it was perceived to harm the profession considering the generally accepted auditing standards (O’Donohoe et al., 1991; SFS 2005:551). The negative attitudes of the auditors could be linked to misconceptions that the auditors had regarding marketing activities (O’Donohoe et al., 1991). For instance, some auditors were reluctant toward marketing activities as it was perceived to be beneath them. The marketing activities were considered as requiring little expertise, strategic planning nor management commitment, where small amounts of resources could provide instant results (Isaacson, 1987). Another reason for the negative reactions to marketing activities becoming a part of the professional responsibilities of an auditor was due to the fear of the “unknown”, where the majority of the certified auditors were unable to visualize themselves as salespeople according to Diamantopoulos, O’Donohoe, and Lane (1989). However, Diamantopoulos et al. (1989) also found that certified auditors were more accepting of marketing activities for each year that passed due to the increased exposure of marketing activities within the profession.

Challenges in the accounting profession are many. Jayalakshmy et al. (2005) argue that the auditors must accept the challenges they are facing to retain their trust and transparency toward the market. Entering the twenty-first century, auditors must be willing to adjust their attitudes towards the client where professionalism should be in the foreground (Jayalakshmy et al., 2005).

17

The auditors that prefer marketing tend to be younger males according to Markham et al. (2005). Nevertheless, marketing activities have today become more accepted as the profession has gained new auditors to the market, where the auditors with a positive attitude towards marketing tend to spend more time on those activities (Broberg et al, 2013; Heischmidt et al., 2002). Additionally, marketing activities such as using social media for personal branding have also become more recognized in the business world which has contributed to the shift in the profession (Labrecque, Markos & Milne, 2011).

Clow et al. (2009) have studied the attitudes of auditors in relation concerning marketing activities in the profession. The study was first conducted in 1993 and then replicated in 2004 to see if there were any differences in attitudes during this period. By comparing the two studies, Clow et al. (2009) found significant evidence where the auditors disagreed more with the statement that if marketing of their services would have been more widely used, large and established firms would grow bigger and smaller firms would become less competitive. Therefore, it was concluded that auditors do not perceive marketing of the auditing profession to be very significant when it came to competitiveness. On the other hand, a recent study by Picard et al. (2018) implies that marketing activities have always been part of the auditing profession. As previously mentioned, auditors have historically relied heavily on networking and reputation to keep current clients, while at the same time attracting new ones. These activities are perceived as marketing activities since they are performed to attract new clients by marketing the personal brand (Picard et al., 2018). However, Scott and Rudderow (1983) argue that there is a fine line in the marketing activities that are performed professionally to preserve current clients while at the same time attracting new ones.

2.5 Relationship marketing

Depending on the accounting firm, different marketing activities are being performed. Larger firms tend to be more aggressive in their advertising methods using telemarketing and television commercials, whereas smaller firms do not apply the same aggressive methods due to the lack of financial funds (Heischmidt et al., 2002). Firms of smaller sizes often believe that word of mouth is the most efficient way of promotion. Auditors that are not comfortable with performing

18

marketing activities will most often deviate from performing them (Heischmidt et al., 2002). Reputation and referrals are more valuable than the price charged for the services. Traditional, firms have maintained a customer base by referrals where a company develops a long-term relationship with its customers (Heischmidt et al., 2002). The relationship marketing is the main strategy for auditors as they build a relationship and future loyalty with the customers to ensure that a stable and profitable relationship is created (Ravald & Grönroos, 1996).

2.6 Technology

Technological developments have helped the profession to shift its focus toward commercialization, where technology has introduced new tools to the market such as web-pages, e-mails, video conferences, and digitalized systems (Ellingson et al., 2001; Rezaee, Elam & Sharbatoghlie, 2001; Kumar, 2018). With the evolvement of technology introducing new tools to the auditors, it has also changed the way in how auditors perform their tasks (Kumar, 2018). Digitalization has made it possible for auditors to communicate with current and future clients through various media, where they are now more accessible. The development of technology has eased the work of the auditors by digitalizing systems (Kumar, 2018) and their clients are now able to be more independent without having to rely on the auditor.

Paperless audits will in the future become a necessity as more clients change to paperless systems. Most procedures will be transferred online, changing the nature of traditional auditing. Spraakman, O’Grady, Askarany, and Akroyd (2015) and Granlund (2007) argue that the auditing profession can no longer survive without its technological developments. Information technology systems are going to leave more time for high-level tasks where the auditor can focus on understanding the client's business. Further, excessive time will be available to help the client develop measurable objectives. This enhances the opportunity for the auditor to offer a wider range of services to their clients in the financial statement audit (Bierstaker et al., 2001).

19

3. Methodology

This chapter aims to describe the methodological approach taken to understand auditor’s perceptions. The collection of data in this paper will be the foreground for the analysis of auditor’s perception of marketing in the auditing profession. To answer the research question, several theories and methods choices must be made.

3.1 Research philosophy

When selecting an appropriate research philosophy, the choice was made between positivism and interpretivism. Positivism focuses on the objective and to generalize human interaction which is ill-suited for reflecting on the variability in human interactions (Bryman & Bell, 2015). Interpretivism contrasts positivism with an understanding of human behavior and a logic that reflects the humans against the natural order (Bryman & Bell, 2015). Therefore, the philosophy chosen for this study is the interpretivism as it differs humans from the natural sciences and let the researcher study human behavior with an empathic understanding. The philosophy allows researchers to conclude human’s interest in a study and doing so by observing individuals from the inside. Access to reality is through the participant’s lived experiences and not the forces that act on it. The interpretive philosophy requires the researcher as a social actor to see differences between people (Bryman & Bell, 2015). Since the attitudes and argumentations of the auditors are expected to be of different nature it is suitable to implement the study with an interpretivist approach.

3.2 Scientific method

The purpose of this thesis was to examine auditor’s perceptions of the shift in the auditing profession. The aim was to deepen the understanding and insight by a phenomenological approach that strands from interpretivism. The phenomenological philosophy studies the human experience based on the premise that human experience itself is naturally subjective and decided by the context in which people live (Goulding, 2005). Further, Goulding (2005) proposes that the phenomenological method is suitable for topics within the field of marketing and when using an

20

in-depth qualitative method. Via a phenomenological philosophy, deeper insight and understanding of the auditor's impression and observation transmits into attitudes through their own experience of reality. The phenomenological researcher has alone one source of data and thus it is the participant’s view and experiences where it is taken as a fact. Therefore, it is important to select participants only if they have lived the experience (Goulding, 2005), hence, auditors with work experience in the auditing profession.

3.3 Approach

There are two main ways to how a researcher chooses to approach research problems. The approaches are, deductive and inductive approach, where the deductive approach builds upon a clear structured theory (hypothesis), whereas the inductive approach draws upon empirical conclusions (Saunders, 2016). The deductive approach is appropriate for quantitative studies as it is difficult to let the researcher interpret the process. The inductive approach, on the other hand, is appropriate for qualitative studies as the approach alone is stated by empiricism with no theoretical perspective. These two approaches can be considered as the ideal approaches which sometimes can be difficult to fulfill (Alvehus, 2019). Considering this knowledge, our study will emerge from an inductive approach.

3.4 Research design

3.4.1 Exploratory research design

As this thesis seeks to investigate the phenomena of the perceptions of auditors by text and informational data, an exploratory approach will be used. The exploratory study is useful when there is a need for clarifying an issue or a problem (Zikmund & Babin, 2012). To further answer the research question includes searching the literature and interviewing experts in the relevant profession. An exploratory approach allows for an in-depth open-ended answer, and unexpected outcomes can be probed for future information and a possibility to further analyze feelings and motivations (Saunders, 2016). The exploratory research is flexible and may be validated by further quantitative research in the future (Erickson, 2017) When the research design was implemented

21

the authors did consider the disadvantages of an exploratory approach. Hence, the result will not stay true for a whole population (Bryman & Bell, 2015).

The advantage of exploratory research is that it is flexible and easy to adapt to change. The researchers of exploratory research must be ready to shift the direction depending as new data appears and brings new insights. The research may at first begin with a broad scope and then become narrow as the research advances (Sauders, 2016) this was considered when conducting the interviews.

With an exploratory nature of research, the next step is to implement a suitable method to collect the data. Two common methods for a researcher is to either deduct a quantitative or a qualitative study. The pros with a qualitative research design are that it may provide insights and details about human behavior, emotions, and personal characteristics. Opposed to where a quantitative is generally about statistically verifiable correlations in populations where the result often is generalizable (Bryman & Bell, 2003). The expected information required for this thesis would be difficult to interpret into numbers and figures, hence the collection of data was in the form of words and text. Hence, a qualitative research design was conducted to answer the research question in the most appropriate way.

3.5 Data Collection

3.5.1 Sampling

A purposive sample was chosen (Bryman & Bell, 2015), as the researchers did not seek to sample participants at random order. The research question “What are auditors’ perceptions of marketing activities as the auditing profession shifts from professionalism to commercialism?” refers directly to a type of profession and people (auditors) which indicates of what sample is required to be collected. The purposive sampling is a fixed strategy as there is little to add on the sample when the research proceeds. According to the theory it is difficult to know the ideal sample size. With the further motivation that sample sizes in qualitative studies should be of the size that is large

22

enough for data analysis and theoretical saturation. However, it should not be of the size where the researchers are no longer able to conduct in-depth analysis (Bryman & Bell, 2015). Therefore, a sample of six auditors working at different accounting firms in Jönköping was sampled. The initial aim was to sample 10-12 auditors in Jönköping with regards to the researcher's ability to process enough relevant data following the timeframe set for this thesis. However due to the current circumstances a sample of six auditors was possible which was still considered as a relevant sample size to this study. With this knowledge the focus on the quality of each interview was highly prioritized and the interview guide was revised multiple times to collect the highest value from the interviews.

To sample the participants, the Google search engine was used to allocate all accounting firms in the Jönköping area. Keywords such as “Revisionsbyrå” Revisionsbyrå Jönköping”, “Revisor Jönköping”, “Revisorer Jönköping” and “Auktoriserad Revisor Jönköping” was used. When the accounting firms of Jönköping were allocated, a standardized email was sent out to all individuals which email address was found at the accounting firm’s websites. The requirement for our sample was that of auditors working in Jönköping with no requirements for a certain prerequisite of work experience. Firms of various sizes and characteristics were targeted to create the possibility to receive different insights and experiences. The individual auditors who accepted the invitation to participate in the study resulted in the sample selected. The date and time for the phone interviews were confirmed with every auditor by private email conversations.

3.5.2 Interviews

There are two main interview structures to adopt according to Bryman and Bell (2015) where the first is unstructured interviews and the second is a structured interview. The structured interview aims to ask the interviewee the same context of questioning for the interviewees to receive the same interview stimulus as any other participant. The unstructured interview rather builds upon a list of topics called an interview guide (Bryman & Bell, 2015). Additionally, there is a third interview structure that stems from the unstructured interview; semi-structured interviews, which was chosen for this study. The context of semi-structured interviews allows the researcher to have a series of questions were a variation of the sequence of questions may occur.

23

To collect the primary data of this study, semi-structured interviews were conducted with auditors currently active in the auditing profession. In exploratory research design, semi-structured interviews are useful to find out what is happening and the concept to further present background material for the study (Saunders 2016). The semi-structured interview is relevant when the researcher is beginning the study with a clear target on what to study. A semi-structured interview was chosen since the structured interview does not allow for deeper discussions with the interviewee. The semi-structured interviews allow for more open-ended questions and do not require the interviewer to follow a certain list of questions. The interviewer uses a list of themes and key questions to follow where the use will vary differently among interviews. Semi-structured interviews are allowing the researcher to an open mind where concepts and theories can transmit from the data (Bryman & Bell, 2015).

Saunders (2016) stresses the importance of personal contact when interviewing rather than a questionnaire where there is no personal contact involved. The aim was initially to conduct face to face interviews at the auditor’s offices. Regarding the global health state of COVID-19 (Folkhälsomyndigheten, 2020) during spring 2020 when the study was conducted, a lot of firms ordered home quarantine for their employees. To make the interviewees feel safe during their interview, an additional email was sent out to each interviewee asking whether they preferred to conduct the interview face to face or digitally. Consequently, this was to make both parties of the interview feel safe and to assure that the result would not be affected by the risk of the participant feeling worried or unfocused during a face to face interview. All auditors choose to be interviewed by phone. Four of the interviews were conducted when the participants were working from home and the other two were conducted by a phone call to the auditor’s office. The reason for phone interviews rather than video calls was due to some technical difficulties where it was not possible to hold video calls with all participants. Additionally, some participants felt more confident conducting the interviews through the phone rather than video call as they had been sick for a few days and therefore did not feel confident to display themselves on camera.

The interviews were held in Jönköping for a two-week time period from the 19th until the 30th of

24

where the researchers could focus on the interview without being disturbed. The interviewees were able to choose the location that felt best for themselves as a result of the phone interviews.

3.5.3 Interview guide

According to Ryen (2004) an interview guide should be performed in the meeting between the interviewee and the researcher to better structure the questions and create an overview of the interview. This, to conduct the highest value possible from the interviews. The first set of questions were to be general questions to create a natural flow in the conversation and make the interviewee feel comfortable answering the questions. The purpose was further to create an understanding of the auditor's background and their experiences from their career. The next section of questions aimed to create an overview of the auditor's personal opinions and experiences of marketing and their services in the auditing profession. The last section of questions was asked to gather a deeper and richer understanding of how the auditor's reason regarding professionalism and commercialism and how marketing activities have affected this potential shift in the profession.

The interview guide is to be found in the appendix where it will be divided into different themes as described above. The introduction questions, background questions of the interviewee, and finally general questions about the auditing profession and marketing. The themes were based on the research question and were the foreground for the empirical analysis. The categorization of questions helped to get an overview and illustrate all answers easier during and after the interview.

Considering the busy time for the auditors the interview guide was sent out in advance for the auditors to prepare and plan accordingly to the interviews. Additionally, in contrast to previous literature that has distinguished between marketing and advertising activities, the term advertising activities have been included in the term marketing activities for this study. Therefore, the researchers of this thesis have generalized marketing and advertising activities to only marketing activities in the interview guide.

25 3.5.4 Pilot Interview

It is important to consider that the way the researcher interacts with the interviewee and ask questions will affect the data collected (Saunders, 2016). Since the researchers were not used to conduct interviews the first interviews might be a limitation of the collection of data. Therefore, a test interview was conducted beforehand. The test interview was conducted one week before the first interview by contacting an auditor within the social network of the researchers. The test interviewee was an authorized auditor with 30 years of experience in the profession working in one of the Big 4 firms. The test interviewee had experience from several offices and working in different roles within the firm. A phone interview was conducted with the test interviewee and was running for 25 minutes. After transcribing the test interview and documenting the answers were done, some changes were made to the interview guide to receive as much value from the future interviews as possible.

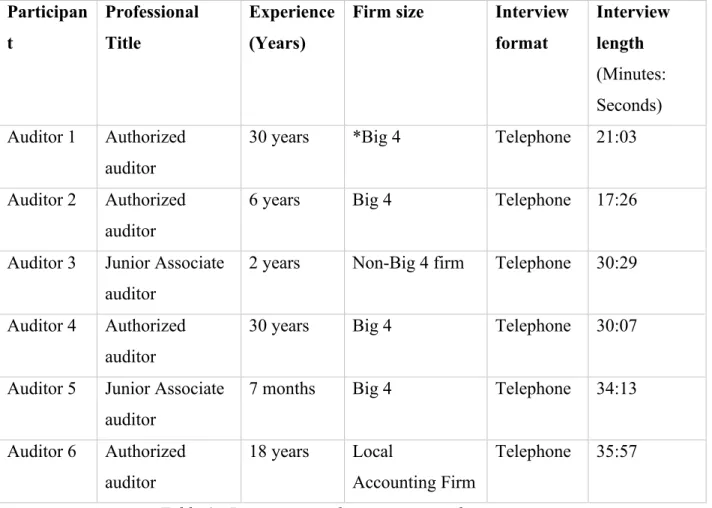

3.5.5 Presentation of the interviewees

A total of six authorized and non-authorized auditors were interviewed with different backgrounds and experiences in the profession as seen in table 1. The interviewed auditors worked at different accounting firms of different sizes where the newest auditor had been working in the profession for a few months whereas the oldest auditor had been working in the profession for over 30 years.

A common education amongst the interviewed auditors was their Degree of Master of Science in Business and Economics, besides for A1. A1 studied the relevant courses that were required to become an authorized auditor before taking an auditor’s test to become authorized. All auditors have experiences from working with all types of companies in terms of size and business forms.

26 Participan t Professional Title Experience (Years)

Firm size Interview format Interview length (Minutes: Seconds) Auditor 1 Authorized auditor

30 years *Big 4 Telephone 21:03

Auditor 2 Authorized auditor

6 years Big 4 Telephone 17:26

Auditor 3 Junior Associate auditor

2 years Non-Big 4 firm Telephone 30:29

Auditor 4 Authorized auditor

30 years Big 4 Telephone 30:07

Auditor 5 Junior Associate auditor

7 months Big 4 Telephone 34:13

Auditor 6 Authorized auditor

18 years Local

Accounting Firm

Telephone 35:57

Table 1 - Presentation of participants and interviews * PwC, Deloitte, KPMG, Ernst & Young

3.6 Data Analysis

The interpretation and analysis of the data collected were based on a model about thematic analysis which created an index for which main themes were used as guidelines when later using coding (Bryman & Bell, 2015). Coding allows for reviewing transcripts and is a central process in the qualitative analysis as it gives theoretical significance to relevant parts that help in organizing the data (Bryman & Bell, 2015).

The interview guide was divided into five main themes based on our research question. The transcribed interviews were then later printed out and thematic coding was then brought out based on an inductive approach. According to Saunders (2016) becoming familiar with one's data to find

27

recurring themes and patterns are important. Therefore, both researchers were present for all interviews. After each conducted interview, the researcher's started the transcription process and later made individual summaries of the data collected which was then compared to find similarities and differences in the interpretations of the interviews.

Coding was then used to manage and find patterns in the collected data. Coding is a valuable tool that allows the researcher to rearrange data collection into groups (Saunders, 2016). However, as some codes were identified early in the process, Saunders (2016) acknowledges the importance of re-reading the data collection as new codes might occur throughout the process.

Saunders (2016) stresses the importance of always referring to the research question when extracting possible themes from the coding. Seven themes were identified throughout the process of analyzing the codes. These themes were used as main categorize to provide an orderly and logical way to analyze the collected data. The seven themes were: (1) Marketing as a tool in a more competitive market, (2) Marketing should be used for brand awareness, (3) Marketing is not my responsibility, (4) Auditing is a trust profession, (5) The most important marketing tool is the word of mouth, (6) Seeing clients is not marketing, and (7) Marketing activities do not affect the professionalism. This categorization helped to get an overview of information and to illustrate all respondent’s answers better.

3.6.1 Data processing

According to Bryman and Bell (2015) it is important to document the answers when interviewing via multiple sources of interviewing tools. Therefore, recordings were implemented to not miss any important information that might have been provided as taking notes might not capture a full interview. After carefully asking the auditors for their consent, a mobile phone was used to record the interviews. The results benefit the analysis of what is being said at the interviews and the capturing of the respondent's own words and phrases. This allows the researcher to focus on asking the right questions and focusing on the tone of voice of the interviewee. The interviews were informed of the anonymity of their participation. Transcription was implemented shortly after

28

every interview with the help of the sound recording and notes taken by the researchers during the interview.

3.7 Protection of Personal Data

A General Data Protection Regulations (GDPR) template was filled out before the interviews were conducted to administrate personal data in a lawfully manner according to the principles of Jönköping University.

3.8 Trustworthiness

Reliability and validity are important factors to assess the quality of the research. Reliability refers to how well a study can be replicated by other researchers and if it will result in the same findings. Validity refers to the fit of the measures used, the rightness of the analysis of data, and the generalizability of data (Saunders, 2016). Researchers have tried to apply the concepts of qualitative research, while other scholars argue that it is not applicable. Therefore, the terms have changed in which sense they are used (Bryman & Bell, 2015)

Following there are four primary criteria for evaluating the quality of a qualitative study: dependability, credibility, transferability, and confirmability (Guba, 1981). The following paragraph will touch upon the criterions relevant for evaluating the quality equivalent to the quantitative research.

3.8.1 Dependability

Dependability is the parallel evaluation criterion to reliability (Saunders, 2016). The objective of dependability is the results to be consistent and the ability for them to be repeated over time (Guba, 1981). This stresses the importance of chapter three in this thesis. Further the dependability can be increased by recording all the changes of the emerging research to be understood and evaluated by other researchers (Saunders, 2016). For this thesis, continuous feedback was given by six other researchers and a supervisor via four mandatory seminars following JU’s thesis manual. Hence,

29

the authors could receive a continuous audit of the thesis comparing patterns and conclusions with the other researchers.

3.8.2 Credibility

The credibility of the research is to find out how true the findings are (Guba, 1981). The focus lies on ensuring that the right worthy representation of the research participant’s social realities matches what they initially intended. There are several techniques such as triangulation, peer debriefing, and member-checking (Saunders, 2016). Peer debriefing is somewhat similar to the external audit as aforementioned in 3.5.3 where the authors received continuous feedback from independent peers to ensure the quality of the research. To further ensure the quality of the research, triangulation of the findings was made. This was done by the collection of data from both internal and external sources (Guba, 1981). For this thesis it was important to find a thread between the interviews when creating the themes. Before the main data collection, the researchers as aforementioned in 3.5.4 conducted a pilot interview with an auditor with significant work experience of 30 years in the profession. This helped set a foundation and give valuable insights into the quality of the interview guide.

3.8.3 Transferability

Transferability is often referred to as the degree which the findings can be generalizable or transferred to another setting (Guba, 1981). The aim of this thesis is however not to be generalized but has instead focused on the possibility to be transferred to other contexts. Thus, it is the researcher's responsibility to do a full description of the research through research questions, research design, and context. Hence the reader is allowed to evaluate the transferability to a different context (Saunders, 2016). To achieve the best quality of this thesis, the reader is provided with our thorough description of the audit industry, the research design, and the research method.

3.8.4 Confirmability

Confirmability is referred to be the neutrality of the research where the issue of neutrality is often the objectivity of the research (Guba, 1981). To prevent bias, the researchers may establish a

30

confirmability audit (external audit for dependability) and document the research process thoroughly as aforementioned in 3.7.1 where the reader can follow the steps the researcher has taken in the research process. Hence, much focus has been put on developing an accurate and detailed methodology section as possible.

31

4. Findings

The findings will start with a presentation of the results based on a thematic structure of the interviews that were found during the transcribing process. The interviews were analyzed through seven themes.

The purpose of this thesis was to examine auditor’s perceptions of the shift in the auditing profession. Therefore, the research question: “What are auditors’ perceptions of marketing activities as the auditing profession shifts from professionalism to commercialism?” was to be answered with the help of the empirical findings. Seven themes were identified when analyzing the collected data to find the auditors’ perceptions of the marketing activities within the auditing profession. These were (1) Marketing as a tool in a more competitive market, (2) Marketing should be used for brand awareness, (3) Marketing is not my responsibility, (4) Auditing is a trust profession, (5) The most important marketing tool is the word of mouth, (6) Seeing clients is not marketing, and (7) Marketing activities do not affect the professionalism.

4.1 Marketing as a tool in a more competitive market

There are two factors for the increased use of marketing activities according to the auditors where the auditors perceived an increasing number of competitors on the market as the first reason for the increased use of marketing activities.

“The number of firms (private) have definitively increased and therefore more marketing activities over time” - A5

The second factor for the increased use of marketing activities in the profession according to the auditors were non-audit services that, over time, became available at accounting firms such as accounting-, tax- and corporate finance services. With non-audit services being introduced to the