AI and the

controller

profession

MASTER THESIS WITHIN: General Management NUMBER OF CREDITS: 15

PROGRAMME OF STUDY: Engineering Management AUTHOR: Jesper Lindblad & Christo Monell

JÖNKÖPING May 2021

Address: Visiting address: Phone number:

Box 1026 Gjuterigatan 5 036-10 10 00

551 11 Jönköping

Acknowledgements

Many people have helped over the last six months, and we would like to take this opportunity to thank them.

First and foremost, the deepest thank you to Anette Johansson. We could not have done this without you. Thank you for the support and the encouragements.

A big thank you to Daniel Pittino, who supervised us during the process. A warm thank you to Lina Ek and Sanna Ström who introduced us to the people behind the AFAIR initiative. A big thank you to Annika Engström who believed in us. A big thank you to the participants from the companies for making the data collection process straightforward.

To all of AFAIR, good luck in the next coming years.

Jönköping May 2021

_________________________ _________________________

i

Master Thesis in Management

Title: AI and the Controller Profession: Impact and challenges in the manufacturing industry

Authors: Jesper Lindblad and Christo Monell Tutor: Anette Johansson and Daniel Pittino Date: 2021-05-24

Key terms: Artificial Intelligence, AI, AI readiness, AI implementation, AI maturity, AI challenges, controller, controlling, digitalization, digitization

Abstract

Background: The trends towards a more digitalized world are ongoing and has a meaningful impact on both society and business. The emergence of Artificial Intelligence (AI) is transforming industries and challenging them to change. The controller profession is a profession that handles a lot of data. Digitization is set to affect professions by increasing the data flows. With a lot of task that are highly data-intensive, the controllers job is to interpret and anlyze the raw data they have available with different tools, models and software to deliver to decision-makers within the company. The current tools and methods that the controllers are utilizing for analyzing internal data coming from ERP-systems such as SAP or Oracle, are becoming outdated. With the rise of digitization and AI, it is believed that companies can create added value through more precise forecasts that are built upon data from inside and outside the firm. The rise of digitalization and AI shows a change in the expected skill profile of a controller, but the new picture of the controller is still uncertain.

Purpose: The purpose of this study is to examine the expected change in the role of controllers in different manufacturing companies that is anticipated to occur with the implementation of AI and challenges that it may bring.

Method: To understand the phenomenon of how the role of the controller is changing due to AI and the challenges it may bring, and to fulfill the study’s purpose qualitative research was conducted. The empirical data is collected through 11 semi structured interviews with controllers, theoretical experts in both Business Administration and AI, as well as BI consultants. The empirical data was analyzed through thematic analysis.

Conclusion: Conclusions of this study confirm already existing theory but also adds to it. The controller’s most important skills, such as financial and analyzing skills will remain to be important in the future. The changes in the role of the controller due to digitalization is already taking place in big manufacturing companies and it is clear that controllers have started to improve their IT-skills due to this. The role of the controller will move increasingly towards what is described in literature as the business partner role. The controller needs, due to AI, enhance and learn certain types of skills such as AI knowledge and “human skills”. The challenges found connected to the implementation of AI are both on an organizational and a individual level, examples of them are creating a vision and guidelines for the controllers to follow in order to enhance participation in the change progress, as well as creating both time and opportunity for the individuals to improve their knowledge on and understanding of AI.

ii

Table of Contents

1. Introduction ... 5

Background ... 5

Problem Definition ... 6

Purpose and Research Questions ... 7

2. Frame of Reference ... 8

Artificial Intelligence ... 8

2.1.1 AI maturity model ... 9

Views on the controller’s competence profile, role, and skillset ... 10

2.2.1 The impact of digitalization on the controller’s profession ... 11

2.2.2 Future Challenges of Controllers ... 11

Change Management ... 13

Method ... 15

3.1 Connection between Research Question and Method ... 15

3.2 Research philosophy ... 15 3.3 Research approach ... 16 3.4 Research Design ... 16 3.5 Data collection ... 17 3.6 Sampling ... 19 3.7 Data analysis ... 19 3.8 Trustworthiness ... 20 3.9 Ethical consideration ... 21 Empirical findings ... 23

4.1 Empirical Data Analysis ... 23

4.2 Results ... 24

4.3 Theme 1 – Controller characteristics now and in the future... 24

4.4 Theme 2 – AI Knowledge & Attitudes ... 26

4.5 Theme 3 – Controller challenges ... 28

4.6 Theme 4 – Organizational challenges ... 30

5. Analysis ... 32

5.1 How is the role of the controller changing due to the implementation of AI in manufacturing companies? ... 32

5.2 What are the challenges relating to the change that comes with the implementation of AI on individual and organizational level? ... 34

6. Discussion ... 37 6.1 Discussion of Results ... 37 6.2 Discussion of Methodology ... 37 6.3 Implications ... 40 6.3.1 Theoretical Implications ... 40 6.3.2 Practical Implications ... 40

iii 6.4 Limitations ... 40 6.5 Conclusion ... 41 6.6 Further Research ... 42 7. References ... 43 8. Appendix... 47

iv

List of Figures

Figure 1: AI maturity model (Gartner, 2018). ... 9

Figure 2: Schäffer and Weber's (2019) model for challenges of digitization for the controller. ... 12

Figure 3: Data collection method used for answering research questions. ... 15

Figure 4: Visualization of the research design, model adopted from Myers (2013). ... 17

Figure 5: Schäffer and Webber (2019) suggestions for new competencies for the controller (7) with the study's contribution in red. ... 34

List of Tables

Table 1: Interviewee information. ... 18Table 2: Six phases of thematic analysis (Braun & Clarke, 2006) ... 20

Table 3: Quality criterion described, based on (Lincoln & Guba, 1985), inspired from (Eriksson, 2014) ... 21

Table 4: Ten principals of ethical practice, adapted from Bell & Bryman (2007). ... 22

Table 5: First order themes, Sub themes and Themes ... 23

Table 6: Lincoln and Guba's (1985) quality criterion and how the criteria were met. ... 39

List of Appendices

Appendix 1: Interview Guide Appendix 2: GDPR Consent Form

Introduction

5

1. Introduction

In the following chapter the background and problem definition are presented followed by the purpose and research questions.

Background

The trends towards a more digitalized world are ongoing and has a meaningful impact on both society and business (Karenfort, 2017). The trends of digitalization and Artificial Intelligence is transforming industries, making traditional companies outdated and challenging them to change (Canals & Heukamp, 2019; Iansiti , 2020; Kerzel, 2021).The rise of digitalization, and especially advanced digitalization, such as Artificial Intelligence, in the following referred to as “AI” for short, is expected to change working methods in many industries at the same time as it will create completely new professions in different kind of firms (Oesterreich & Teuteberg, 2019). Daugherty and Wilson (2018) suggest that AI will boost human talent and improve processes and end products through cooperation between humans and machines.

There are many definitions to AI, and it can be difficult for one to get a grasp of what the expression means. The most established definition of AI is, the ability of digital technology to perform tasks associated with intelligent beings or humans (Copeland, 2020; Zhu et al., 2020; Stuart & Norvig, 2016; McCarthy et al., 1955), this definition leaves a lot of space for interpretation to the person who reads this definition. One fundamental part of AI is the ability to learn new things on its own (Copeland, 2020; Stuart & Norvig, 2016). This ability is a part of what can be defined as machine intelligence which is the machine's ability to mimic the intelligence of humans along with other parts such as logical reasoning, planning actions and discovering potential opportunities or gaps (Stuart & Norvig, 2016). Heaton et al. (2017) states that machine learning utilizes large sets of data to first learn and then make predictions from what the AI has learned. They continue by claiming that this type of AI can be made to function without human interaction and can analyze multiple sets of diverse data such as economic, legal, and demographic data to provide a valuable estimation often better than provided by humans. The emergence of digitalization is set to affect a lot of businesses and professions by increasing the data flows, one profession that already handles large amounts data is the controller (Bragg & Roehl-Anderson, 2011). The role of the controller is something that has been through changes ever since it was first described in the first empirical study of the role, over 50 years ago, where task such as scorekeeping, attention directing and problem solving were identified (Lindvall, 2017). Bragg and Roehl-Andersson (2011) compares the controller to a ship’s navigator, he or she has to keep the CEO (the captain) updated with the performance of all departments within the company such as product sales, costs and profits while also having an eye on the impact of regulations related to the firm. The definition is in line with the one given by Verstegen et al. (2007) i.e., that the controller supports and advises the management of the firm in realizing their economic and their goals.

The role of management accountants and controllers (although there can be a difference between the management accountant and the controller, this report uses the two descriptions interchangeably and the definition being the one previously mentioned in the background) today vary greatly in different organizations, with the responsibilities and work tasks ranging from governing and regulating the accounting department to providing support for the CEO and board in strategical financial decisions (Hartmann & Maas, 2011). With a lot of task that are

Introduction

6

highly data-intensive, the controllers job is to interpret and anlyze the raw data they have available with different tools, models and software to deliver to decision-makers within the company. It is expected that controllers today need to have a high analytical ability and excellent IT-skills to manage the increasing data flows (Brands & Holtzblatt, 2015). The current tools and methods that the controllers are utilizing for analyzing internal data coming from companies ERP-systems such as SAP or Oracle, are becoming outdated and are hard to utilize with the new types and amounts of data (Brands & Holtzblatt, 2015).

Traditionally, the controller’s data analysis tasks are limited to structured data coming from internal programs e.g., ERP systems and Excel spreadsheets (Brands & Holtzblatt, 2015). One way of combining data from these different kinds of software within the company is by utilizing Business Intelligence tools, in the following referred to as “BI” for short, these BI tools are used in order to retrieve and analyze data, to be able to transform it into graphs, charts, and other types of visuals that controllers may use to easily help managers in making quicker decisions (Pratt & Fruhlinger, 2019). Bhimani and Willcocks (2014) believe that to only relying on historical data for decisions is insufficient. With the rise of digitization and AI, it is believed that companies can create added value through more precise forecasts that are built upon data from inside and outside the firm (Brands & Holtzblatt, 2015). Even though AI and BI are similar in many aspects and can build on each in order to create synergy effects, it is important to know that they are separate and distinct technologies (Toptal, 2018). There have been discussions about possibly infusing AI technology into BI tools as a way of not only increasing BI tools capacity and range, but also easing the implementation of AI into organizations (Korolov, 2018).

AI is already on its’ way to become a part of the financial departments within organizations as Kokina and Davenport (2017) notes that AI already made its debut in basic accounting tasks. A survey conducted by Xiaohui (2019) shows that not only entry-level accountants are experiencing change of work focus due to AI. Several articles and publications from books, journals, and other types of media from recent years points out a change in the expected skill profile of a controller (Schäffer & Weber, 2019; Bhimani & Willcocks, 2014; Payne, 2014). Advanced IT knowledge is argued to become an increasingly important skills for controllers, some even call it a "must have" for the future controllers (Bhimani & Willcocks, 2014; Payne, 2014; Karenfort, 2017). In contrast to this, Oesterreich and Teuteberg (2019) question the increased importance of these IT skills for the controllers, they claim that it is up to the organizations to decide if they want to have these ‘next level controllers’ or if they want to hire specialist for the data analytics and other IT specific topics. Lindvall (2017) believes that it is important that the IT solutions and the organization develops in a synchronized way, so that the IT knowledge matches the IT solutions and controllers will be able to use the tools they have available. The full impact of digitization on the role of the controller is still unclear as it is an ongoing process (Möller et al., 2020). Based on these findings, we believe there are incentives to investigate how controllers are experiencing the change that is set to come with the implementation of AI.

Problem Definition

As AI makes its way into today’s organizations it will boost human talent and improve processes and end products through cooperation between humans and machines (Daugherty & Wilson, 2018). This will have an impact on society (Karenfort, 2017), but more specifically, it will change and create new types of work (Oesterreich & Teuteberg, 2019). The controllers individual work assignments and roles differs depending on the size of the companies they work for today and will continue to be diverse in the future (Brands & Holtzblatt, 2015). Companies

Introduction

7

are set to change their strategies and work procedures to accommodate for the emerging changes that AI brings, with as many as 85% of CEOs worldwide believing that AI will affect their businesses in the near future and that they will invest heavily into AI technology (Cottenie & Liedekerke, 2019; Nanterme & Daugherty, 2017). AI is set to affect controlling tasks such as consolidation, reporting, internal control, and analytics, leading the controller to focus on more value creating task closer to decision-makers within the companies (Deloitte, 2018).

The controller, who uses a lot of data (Bragg & Roehl-Anderson, 2011), has a role that is destined to change (Bhimani & Willcocks, 2014; Payne, 2014; Karenfort, 2017). How the controller’s role will change, and in which directions it will change is up to the companies and their strategic approach towards AI and inclusion of controllers in these strategy efforts (Oesterreich & Teuteberg, 2019).

Purpose and Research Questions

As can be seen in the background and problem definition digitalization and AI is set to make its’ ways in today’s organizations (Daugherty & Wilson, 2018). AI will have an impact on society, but more specifically, it will have an impact on the role of the controller (Karenfort, 2017;Bhimani &Willcocks, 2014; Payne, 2014). How the role will change is still unclear, and it is up to the organizations to decide (Oesterreich & Teuteberg, 2019). As most of the previous research has mainly focused on digitalization (Oesterreich & Teuteberg, 2019; Schäffer & Weber, 2019), we believe that it should be investigated how AI will affect the controller’s role, thus the purpose of this study is:

To examine the expected change in the role of controller in different manufacturing companies that is anticipated to occur with the implementation of AI and challenges that it may bring.

To get to the core of the controllers’ role and the change which AI is set to bring forth, the first research questions is:

How is the role of the controller changing due to the implementation of AI in manufacturing companies?

By understanding what types of changes that the controllers in manufacturing companies are facing with the implementation of AI, we also want to examine the challenges related to it, which leads us to the question:

What are the challenges relating to the change that comes with the implementation of AI on individual and organizational level?

With this purpose and questions, the research desires to be able to create a better understanding for the change of the controller role that the implementation of AI brings. Through a better understanding, we also desire to discover what challenges that the change may bring.

Frame of Reference

8

2. Frame of Reference

This chapter contains literature forming the basis of the frame of reference. The theories address Artificial Intelligence, Digitalization’s change on the controller function and Change management.

Artificial Intelligence

AI is viewed by many as a disruptive technology that will reshape the business landscape (Kerzel, 2021). In multiple surveys, as many as 85% of CEOs worldwide believe that AI will change how they conduct business in the near future and that they will invest heavily into AI technology (Cottenie & Liedekerke, 2019; Nanterme & Daugherty, 2017). Businesses such as Spotify, Facebook, and Amazon have already implemented AI into their organizations. They utilize machine learning algorithms creating suggestions for new music, connections, or purchases for the customers based on their past behaviours and preferences (Nanterme & Daugherty, 2017). Other examples of AI technologies being used presently, is Amazons Alexa which utilizing speech recognition in combination with machine learning and Tesla’s self-driving cars using machine vision also in combination with machine learning and other technologies (Nanterme & Daugherty, 2017). Exhibiting the huge potential of machine learning and the possibility of using it in a vast array of different businesses and organisations (Kerzel, 2021).

One of the issues with AI is the many definitions, creating confusion or difficulty understanding what AI technology is and what it can do (Kerzel, 2021). With the most established definition of AI being the ability of digital technology to perform tasks associated with intelligent beings or humans (Copeland, 2020; Zhu et al., 2020; Stuart & Norvig, 2016; McCarthy et al., 1955), leaving a lot of space for interpretation to the person who reads this definition. Especially since it is even hard for researchers in psychology to agree on a unified definition for human intelligence (Canals & Heukamp, 2019). Understanding of AI and how it can be used, is a key factor for successful adaptation of AI into businesses and organizations (Kerzel, 2021). The currently most successful application of AI is machine learning, where the AI system either can learn by itself or with the help of human input, often through interaction with a large number of users from outside of the organization, a method called crowdsourcing (Canals & Heukamp, 2019). However, the crowdsourcing method is seldom preferred in business uses as the data often is sensitive and therefor confidential or the problems are so complex that it becomes difficult to create scenarios where outside users can interact (Canals & Heukamp, 2019). What is also important to consider for organizations who are looking to gain competitive advantages from applying AI, is that the AI used in businesses today is applied in narrow business cases, specifically designed for AI to be successful (Canals & Heukamp, 2019). They describe this type of narrow AI, also called weak AI or ANI, as the first step of three in an AI evolution, where the following two steps are general AI, also called AGI and Artificial Super Intelligence, also known as ASI (Barrett & Baum, 2016).

Examples of ANI is digital/virtual assistants, factory robots, and healthcare support systems, which are performing a specific task e.g., interpreting and performing voice commands, assembling a car, or helping a doctor to analyze an x-ray (Canals & Heukamp, 2019). For AGI there are no examples as it has not yet been developed, but in essence it would be able to perform

Frame of Reference

9

any type of tasks, similar to any human (Canals & Heukamp, 2019). Researchers are not in agreement on when this type of AI is going to be developed with predictions being in the span of 20 to 100 (Stuart & Norvig, 2016). ASI is described as the next level from AGI, this type of AI is more intelligent than human beings in all areas and fields (Barrett & Baum, 2016). 2.1.1 AI maturity model

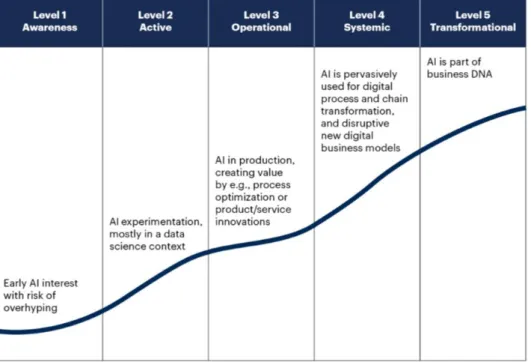

AI readiness can be described as “the preparedness of organizations to implement change involving applications and technology related to AI” (Alsheibani et al., 2018). Jöhnk et al. (2020) claims that if organizations are capable of correctly determining its AI readiness and draw the right conclusions before AI related proceedings, organizations can minimize risk and make better AI related decisions. They add that to implement AI requires constant assessment of AI readiness factors. Additionally, Ellefsen et al. (2019) believes that organizations first should recognise their own readiness before implementing AI. They continue by claiming that AI maturity models are advantageous to use for assessing one’s AI readiness. Several AI maturity models exist, they contain four or five levels, the lowest level in the models is described as a situation where no AI is applied (GAO, 2016; Pringle & Zoller, 2018; Gartner, 2018). This report is based on Gartner’s (2018) AI maturity model, since they are believed to be one of the thought leaders within AI (Preimesberger, 2007; Privateer, n.d.).

According to Gartner (2018) an AI maturity model can help with establishing a strategy for AI, their AI maturity model contains five levels of maturity: Level 1: awareness, Level 2: Active, Level 3: Operational, Level 4: Systematic, Level 5: Transformational. See Figure 1. After the figure, a more detailed description on the levels follows.

Figure 1: AI maturity model (Gartner, 2018).

Level 1: Organizations in level 1 are aware about AI but have not routinely used AI. These organizations often show excitement towards an implementation of AI. The organization

Frame of Reference

10

discusses ideas for how to use AI, but not strategies. Organizations in this level often speak more of AI than they understand.

Level 2: AI can possibly be seen in pilot projects. Meetings are being held about AI where AI expertise is shared, standardization discussions are starting to take place.

Level 3: At this level, the organization have at least one AI project, experts and the right technology are available at the company. AI has its own budget and a senior responsible owner. Level 4: The new digital projects in the company are considering AI. People in the company within the process and application department understand the technology. AI applications interact efficiently in the company and through the business systems.

Level 5: Companies on level 5 have AI implemented in the whole organization (Gartner, 2018). According to Gartner (2018) organizations that have implemented AI estimates it taking four years, while companies that are yet to have an AI project launched anticipates the time being less than two years. The problem can lie within the hype for AI, logistical and strategic challenges (Gartner, 2018).

Views on the controller’s competence profile, role, and skillset

The role of controllers is a well-researched topic, and it is highly recognized that the role varies greatly in different organizations, with highly diverse expectations towards controllers within the organizations as well (Hartmann & Maas, 2011; Schäffer & Weber, 2019). It is not only the role that varies, but also the tasks and responsibilities, Mouritsen (1996) has identified 18 separate tasks, while Siegel et. al., (1999) has identified up to 30 separate work tasks that are performed by controllers in different organizations. Bragg & Roehl-Anderson (2011) has identified the following six responsibilities and job functions that are among the most common for controllers of today:

• Planning: Who does what, how and when in the accounting department is a part of the controller’s job, as well as supporting other departments in their budgeting processes. • Organizing: Another responsibility is organization of the accounting department giving

opportunity to accomplish their work. Procuring work force talent, office supplies and both computer hardware and software.

• Directing: Ensuring that the staff members of the accounting department work properly together to achieve the goals and plans that has been set up by the controller.

• Measuring: One of the responsibilities is measuring the financial performance of the firm, to make sure that the goals are met, and possible errors are detected.

• Financial Analysis: Reviewing, analyzing, and coming up with recommendations for management to make strategic financial decisions.

• Process Analysis: Further responsibilities of the controller is reviewing and analyzing of processes, making sure that they performed with profitability and efficiency.

In a quantitative study by Oesterreich and Teuteberg (2019) they analyze the competence profiles of over two thousand German controllers and management accountants on the business social media platform XING, with regards to their academic degrees, business analytics and IT skills. The top three business analytics skills mentioned in the study where, business intelligence (7,6%), statistics (2,2%) and modelling (1,8%), with the top three IT skills being in programs such as, SAP (40%), Office (21%) and Excel (16%) (Oesterreich & Teuteberg, 2019). Oesterreich and Teuteberg, (2019) concludes that there is an apparent gap between

Frame of Reference

11

controllers current and future skills with regards to their business analytics competences, but at the same time they question whether the ideal skillset that has been set up is realizable in practice.

With regards to the complexity of the role, plenty of researchers has created personas to help describe the different types of roles that controllers typically possess (Hartmann & Maas, 2011). Some examples of this are, Hoppers’ (1980) description of controllers as bookkeepers and service aids, and Jablonsky et. al. (1993) descriptions of controllers as corporate policemen and business advocates/partners. Where the roles as bookkeepers and corporate policemen aims to describe controllers whos’ main role is reviewing and controlling the finances of organizations (Hartmann & Maas, 2011). While the roles of service aids and business partners aims to describe controllers whos’ main role is providing guidance and support to management in strategic financial decisions (Hartmann & Maas, 2011). However, these roles are rarely mutually exclusive as the controllers’ balance between and switch in and out of multiple roles in their daily work (Schäffer & Weber, 2019).

2.2.1 The impact of digitalization on the controller’s profession

The digital transformation of firms’ financial departments is an ongoing process, that is set to be both challenging and long (Chandra et al., 2018). Professionals have argued that the potential influence of the digital transformation on finance and controlling functions is set to be immense (Möller et al., 2020). There are many possibilities that comes with digitalization such as automation of data conciliation, advanced financial planning analytics, automated data visualization to support business decisions and so on (Chandra et al., 2018). However, there are some possible obstacles for the digitalization of firms which can include inadequate IT-readiness, ambiguous RPA-vision, and an unprepared data fragmentation process (Stefanova et al., 2020). Möller et al. (2020) suggests that controllers should take part in the implementation of the companies’ digital strategy as they usually are the highly involved in future planning strategies of the companies such as the organizational structure and business model.

This far, AI has mainly been a tool for automating easier, repetitive, low-level accounting and auditing task, such as data acquisition, balancing accounts and spotting anomalies in transactions, freeing up accountants for more value creating tasks (Kokina & Davenport, 2017). In these cases, an AI technique called machine learning has been utilized, which requires both structured tasks as well as structured data (Kokina & Davenport, 2017; Gandomi & Murtaza, 2015). The finance department does not necessarily have to learn everything about different types of AI-technology by themselves but will be able to learn how to use these technologies with the help of data scientists who should work closely with the department (Möller et al., 2020). Lindvall (2017) argues that the controllers are too limited in their in their self-development and exchange of knowledge both within and outside the organization and believes that further cooperation and collaboration would benefit both the individual controller as well as the organization.

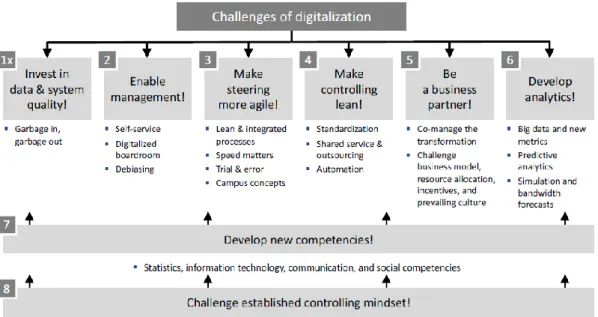

2.2.2 Future Challenges of Controllers

In the chapter “Digitalization will radically change controlling as we know it” in their book “Behavioral Controlling”, Schäffer and Weber (2019) states that the controllers must adapt their job profile, competencies, and mindset in order to adapt to a digitalized business world. They state that there are eight challenges of digitalization for controllers, see Figure 2. They propose that it should be in the controllers’ interest to be in charge of preparing this change and tackle these challenges, in order to remain as a fundamental part of their organizations. The eight

Frame of Reference

12

challenges proposed are the following: (Schäffer & Weber, 2019, p. 160) 1) invest in data & system quality, 2) enable management, 3) make steering more agile, 4) make controlling LEAN, 5) be a business partner, 6) develop analytics, 7) develop new competencies and 8) challenge established controlling mindset. The challenges are described in more detail below.

Figure 2: Schäffer and Weber's (2019) model for challenges of digitization for the controller.

The eight challenges of digitalization for controllers stated by Schäffer and Webber (2019), is lead off with what is probably the most vital one. The first challenge is investing in data and system quality, i.e., making sure that you are properly managing the firms’ data, which is more crucial than ever in a digitalized business world. The expression “garbage in, garbage out” is used to describe the importance of the data being put into the system, the result it has on the data being pulled out of the system and the conclusions being drawn from it. Traditionally, data management has been an integral part of the controller’s role and will continue to be so, with an even greater importance due to the amount and types of data available.

The second challenge is about enabling management, both upper and middle managers, by providing them with access to the information systems. Traditionally, the controllers have been the gatekeepers of this information, but due to the high pace of business today they need to provide access to real-time updated KPI’s (key performance indicators) necessary for their day-to-day business. The third and fourth challenge is somewhat intertwined, not procedurally intertwined, but the goal of the challenges are the same, making controlling task more simple, efficient, and standardized. The agile process is focused on working with short iterations and small work-packages performing smaller tasks at a higher pace, while the lean process is focused on creating a better workflow, by sometimes either refining or even removing tasks. The fifth challenge has been a topic for controllers for quite some time even before digitization but has gained ever more attention due to the fact that companies’ structures are being changed by it. The high pace of business today has made the organizations flatter and more open today, giving the controllers the opportunity to act as an intermediator transferring information between departments and working closer together with upper management acting as a business partner. In order to do this, the controllers need to tackle the sixth challenge by creating analytics that process company data in real-time and create output. The controllers cannot any

Frame of Reference

13

longer be dependent on only small amounts of data provided in the firm’s financial statements in order to keep up with competition.

These six challenges will lead to the seventh and eight challenge for controllers. The role of the controller will inevitably change and thus also bring about changes not only in the skills or competencies needed by controllers, but also change in the current controlling mindset (Schäffer & Weber, 2019).

Change Management

With the rapidly and constantly developing business environment of today, the need for change within companies and organizations is considered to be more crucial than ever (Todnem, 2005). However, in order for change efforts to be successful, it has to be managed. Moran and Brightman (2001, p. 111) has defined change management as “the process of continually renewing an organization’s direction, structure, and capabilities to serve the ever-changing needs of external and internal customers”. It is not only costumer needs that is bringing about change in the organisations, but also technological advancements. AI technology is one thing that is going to bring about change in business, in a survey conducted by PWC 85% of global CEOs recognised AI as something that will change how businesses are being run in the coming five years (Cottenie & Liedekerke, 2019).

Change comes in many different size, shapes, and forms, it affects all different types of organizations, no matter if they are big or small, in all kinds of industries (Todnem, 2005). In his review of change management literature Todnem (2005) has identified different types of change depending on factors such as rate of occurrence, how it has come about and the scale of the change. To begin with the three main types of change defined by the rate of occurrence is continuous, discontinuous, and incremental change. Whereas change defined by how it comes about is divided into four types planned, emergent, choice and contingency. Finally, change defined by scale is divided into four different types, incremental adjustment, fine-tuning, modular transformation, and corporate transformation. To conclude, these different types of change needs different kinds of strategies, approaches, and management from the organizations (Todnem, 2005).

A model that addresses emergent change, which AI would be considered to be, is Kotter’s' (1996) “Eight-stage process for leading organizational change and the transformation that comes with it”. Kotter’s’ model is considered to be one of the most extensively recognized models in change management (Wentworth et al., 2018; Pollack & Pollack, 2015). The eight stages suggested for leading organizational change are the following (Kotter, 1996, p. 21):

1. Establishing a sense of urgency. 2. Creating the guiding coalition. 3. Develop a vision and strategy. 4. Communicating the change vision. 5. Empowering broad-based change. 6. Generating short-term wins.

7. Consolidating gains and producing more change. 8. Anchoring new approaches in the.

These eight stages are developed to create an understanding throughout the organization of the need for change, but also to ensure that the change is sustainable in the long term. So, that the organization does not return to its old ways after the most active part of the change work is

Frame of Reference

14

completed or has lost momentum (Kotter, 1996). To avoid doing things in the same way as always, an issue called path dependency, organizations need to actively work on the technologies and structures that may be hindering their employees (Greener, 2002).

Research method

15

Method

In the following section the methodological framework used for this report is presented. First, we present the connection between the research question and the method. Moreover, our philosophical standpoint, the research approach and design, the data collection and data sampling methods are presented, as well as the method for data analysis. Lastly, we highlight trustworthiness and ethical considerations.

3.1 Connection between Research Question and Method

The methodology of research should be appropriate to the research questions (Easterby-Smith et al., 2018). To answer the research questions in this study, empirical data has been gathered in the form of qualitative interviews, see Figure 3.

Figure 3: Data collection method used for answering research questions.

3.2 Research philosophy

To have a clear sense of one’s reflexive role in research methods, one has a duty to understand the philosophical underpinnings of one’s research (Easterby-Smith et al., 2018). Additionally, a research philosophy in accordance with one’s own belief of reality creates a strong research design (Mills et al., 2006). The philosophical underpinnings referred to are ontology, epistemology, methodology and methods and techniques. In the following ontology and epistemology will be reviewed, as well as our standing.

According to Easterby-Smith et al. (2018) ontology is the “basic assumptions that the researcher makes about the nature of reality” (Easterby-Smith et al., 2018, p. 109). The purpose in this thesis to examine the expected change in the role of controllers in different manufacturing companies that is anticipated to occur with the implementation of AI and to understand the related challenges. The data collected is in the form of qualitative interviews, which reflects the individuals own truth from their own perspective (Easterby-Smith et al., 2018; Patel & Davidsson, 2011). These experiences are believed to depend on the interviewee’s previous experiences, workplaces, education or the like. Thus, we accept that there are multiple truths. The acceptance of this idea places the research in the ontological position of relativism. Relativism is according to Easterby-Smith et al. (2018, p. 114) “an ontological view that

Research method

16

phenomena depend on the perspectives from which we observe them…”, which is in line with our standpoint.

The different views on ontology are usually linked to certain epistemologies (Easterby-Smith et al., 2018). A relativistic ontological position is often linked to an epistemological position in social constructionism. The epistemological position of social constructionism is based on the idea of reality being decided by people rather than by other factors, therefor it is of importance to value the way people perceive their realities (Easterby-Smith et al., 2018). The qualitative interviews this research depends on lifts and values those different perspectives from different individuals, hence the epistemological position taken by the researchers is social constructionism.

3.3 Research approach

With focus on experiences of the expected change in the controller role and challenges related to the expected change, the study is of an explorative nature; hence an inductive approach is believed to be suitable. An inductive approach moves from data to theory, in practice this means that an object in reality is studied and that the empirical findings about it formulate theory (Patel & Davidsson, 2011). The experiences around an expected change due to AI is not well related to any accepted theory, which benefits an inductive approach, where one draws conclusions from observations in reality (Easterby-Smith et al., 2018). Although, Dubois and Gadde (2002) states that it is important to consider theory, but that one should not be held back by following what previous theory says. In the case of this thesis, theory has been taken into account to make sense of data, however, theory has been used carefully to not create any biases. An inductive approach is according to Bryman and Bell (2015) suitable to constructionist philosophy and qualitative methods. To relate back to the philosophical position we hold, it lies in social constructionism and our decision is to adopt qualitative methods.

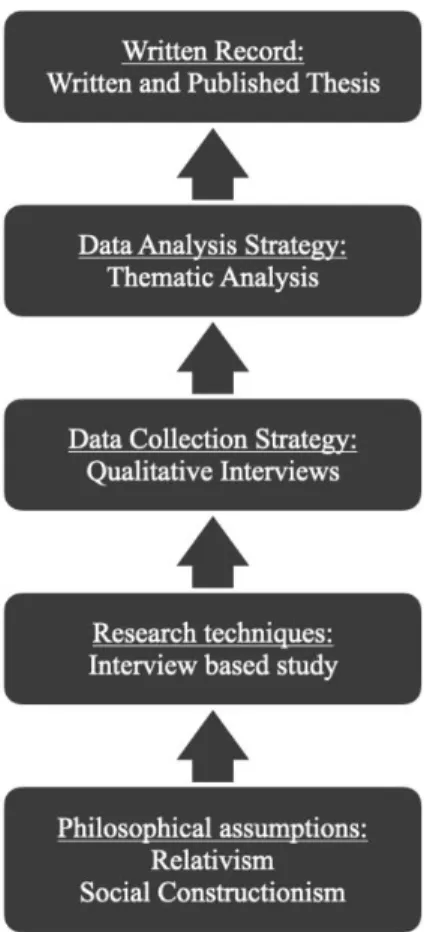

3.4 Research Design

Research design should according to Myers (2013) be described to provide a description of the sections of the research project. The description should contain the philosophical assumption, adapted research method, data collection techniques, data analysis, and the way that the material is displayed, together with how the findings are planned to be published (Myers, 2013). This far, we have described our philosophical stand, our inductive approach and touched upon the qualitative interviews that is meant for the data collection. To visualize the whole research design, a figure inspired by Myers (2013) is used, see Figure 4.

Research method

17

Figure 4: Visualization of the research design, model adopted from Myers (2013).

This study serves as a preparatory study for the research project PrepAIr, which is the introductory part of the larger research project AFAIR, which has given us the opportunity to access the partner companies and their employees for data collection. AFAIR (Ambidexterity, Flows and AI for competitive Responsiveness) is in turn a part of Jönköping University's research and educational environment SPARK, which is in place to promote companies' development of knowledge-intensive products, services, and processes. The purpose of AFAIR is to investigate how AI can help organizations to streamline flows and in their work with creating new client offerings. Further the purpose is to investigate how organizations currently are handling this technology development and how they can introduce and use AI-based tools at a strategic level. Overall, the research initiative aims to understand the mechanisms that affect the organization's readiness of a potential AI transformation.

3.5 Data collection

The report relies on primary data in the form of qualitative interviews. According to Easterby-Smith et al. (2018) qualitative interviews are suitable when the aim of the interview is to gain information in context about the interviewee’s perspective on a specific phenomenon (in this case, the expected change in the controller function due to AI). Thus, the data collection method has been in the form of qualitative interviews.

Interviews have been held in a semi structured way. Having the interview semi structured gave us comparable data (Easterby-Smith et al., 2018). Narrative interviews have been used in order to create rich descriptions and avoid missing important pieces of the studied phenomenon (Belgrave & Charmaz, 2012). Having the interviews semi structured and in a narrative form

Research method

18

tend to give more personal answers, which is considered suitable, also, it should be mentioned that interviews is a form of data collection that is subjective (Tracy, 2013; Gillham, 2005). To create the interview questions, the research questions were revisited, as suggested by (Easterby-Smith et al., 2018). Since the interviews should cover as much as possible and be semi structured, a topic guide has been crafted, see appendix 1. The topic guide has three topics, controller, AI and BI. Some of the topics were discussed in two manners, in one hand the topic only, and later combined into one topic, e.g., AI and controller became the topic AI+Controller, to get answers regarding the topics together. The topics also had predetermined sub-questions in case of the interviewee not opening up for deeper discussions. One of the strengths of having a narrative interview with a topic guide is that interviewees can come with new perspectives on topics (King & Brooks, 2017).

To get to the core of the purpose and to understand how the role of the controller is changing and challenges related to it, not only controllers were interviewed. According to Easterby-Smith et al. (2018) the constructionist believes that there are many realities, and that the researcher needs to gather information from several viewpoints and observers, hence theoretical experts in business administration and AI, as well as BI consultant were also interviewed to help paint a holistic picture of the phenomenon, since they have a different perspective on the role of the controller, a list of the interviewees can be seen in Table 1. That the study values different perspectives on the phenomenon can be seen as triangulation, according to Easterby-Smith et al. (2018) triangulation is the process of using different perspectives in order to increase confidence in the accurateness of the observations. In a social phenomenon such as AI, this is seen as highly appropriate.

When interviewing experts in an area, who have more knowledge than the interviewer, an elite interview is conducted. Here, the interview might go directions that has not been planned for, and that has to be in mind of the interviewer (Gillham, 2005). Gillham (2005) continues and states that in order to get this type of interviewee to become more open when answering, a transcription of the interview should be sent to the interviewee for review. The transcriptions were offered to the interviewees in the study, to follow Gillham’s (2005) guiding.

Table 1: Interviewee information.

Interviewee Title Described as in paper Workplace Format Time Lenght Data Collection Date

Pilot Regional Finance Manager Controller Manufacturing

company Zoom (video) 52 min

Semi Structured Interview 2021-02-12 Interviewee 1 Assistant Professor

Business Administration

Theoretical expert

Business Administration University Zoom (video) 66 min

Semi Structured Interview 2021-03-19 Interviewee 2 Assistant Professor

Business Administration

Theoretical expert

Business Administration University Zoom (video) 50 min

Semi Structured Interview 2021-03-24 Interviewee 3 Docent

Business Administration

Theoretical expert

Business Administration University Zoom (video) 32 min

Semi Structured Interview 2021-04-06 Interviewee 4 Professor

Computer Science

Theoretical expert

AI University Zoom (video) 54 min

Semi Structured Interview 2021-04-15 Interviewee 5 Digital Training Specialist BI Consultant Software company Zoom (video) 42 min Semi Structured

Interview 2021-04-21 Interviewee 6 Controller Controller Manufacturing

company Microsoft Teams (video) 50 min

Semi Structured Interview 2021-04-23 Interviewee 7 Business Intelligence

Consultant BI Consultant

Business Intelligence

company Zoom (video) 52 min

Semi Structured Interview 2021-04-28 Interviewee 8 Chief Controller Controller Manufacturing

company Microsoft Teams (video) 43 min

Semi Structured Interview 2021-04-28 Interviewee 9 Chief Controller Controller Manufacturing

company Zoom (video) 48 min

Semi Structured Interview 2021-05-03 Interviewee 10 Controller Controller Manufacturing

company Zoom (video) 49 min

Semi Structured Interview 2021-05-03

Research method

19

3.6 Sampling

The sampling of the interviewees with controllers was based on a non-probability, purposive sampling. According to Easterby-Smith et al. (2018) a purposive sampling is suitable when the researchers know what type of participants that are needed for the study. In the case of this thesis, we needed to interview controllers, hence the criteria for inclusion were to be a controller. The interviews have been conducted with controllers connected to the AFAIR project at Jönköping University. The study was presented in a preparation meeting with AFAIR connected companies, the companies that were interested in participation of the research declared it to us. We then made contact with two contact persons, at two different companies. The contact persons then provided two controllers each to interview.

The sampling of the interviews with BI-consultants was based on a non-probability, purposive sampling. The interviewees were chosen based on the criteria that they had weekly encounters with controllers, from a standpoint where they assist and support controllers with questions regarding BI tools.

The interviews with the theoretical experts in the Business administration and AI have been based on a non-probability, purposive sampling and snowballing sampling. Snowballing sampling is according to Easterby-Smith et al. (2018) suitable when interviewees are hard to find. In the beginning of 2021, our supervisors provided us with contact information to two theoretical experts in business administration and one in AI, those interviewees were asked to recommend other individuals who met the criteria of being part of the study, for the theoretical experts in business administration, the criteria were that they possessed knowledge about the controller function.

3.7 Data analysis

The analysis has been conducted through thematic analysis. Thematic analysis is used to identify patterns, organize and describe data. Easterby-Smith et al. (2018) states that to systematically and thematically structure data guides the analysis of qualitative data. It should also be noted that interviews are one form of data that is considered suitable for this type of analysis (King & Brooks, 2017; Easterby-Smith et al., 2018). The most important thing in thematic analysis is that the researchers are consistent throughout the process (Braun & Clarke, 2006). The thematic analysis is done via incremental steps seen in Table 2. These steps guided the research throughout the whole process. According to Braun and Clark (2006), the analysis is a process where the researchers move between phases until the result is complete. Summarized, Braun and Clark (2006) explains the steps in the following way:

Research method

20

Table 2: Six phases of thematic analysis (Braun & Clarke, 2006)

The data analysis began by reading and transcribing the interviews. The segments of data were then coded into words describing the data. This resulted into 70 codes, which later led to four themes. For a detailed description of how steps (1-5) were conducted, see chapter 4.1.

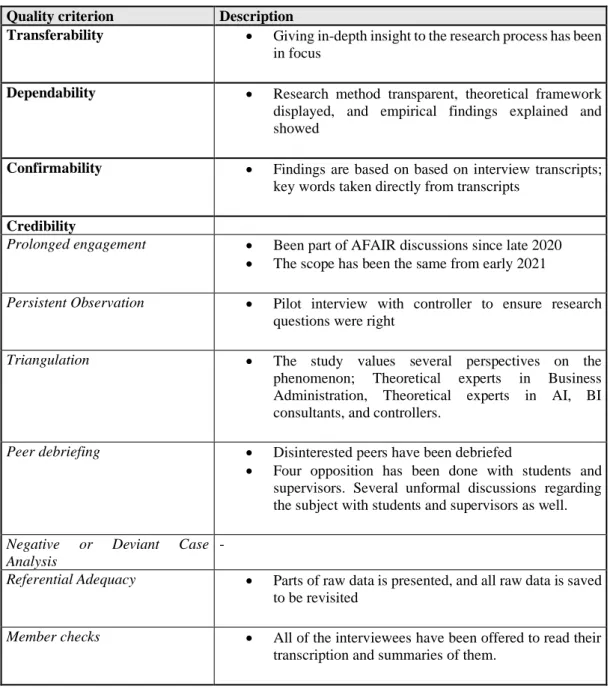

3.8 Trustworthiness

According to Easterby-Smith et al. (2018) quality in qualitative research depends on how researchers approach their research, from beginning to end. Researchers who conduct research in a reflexive and transparent way often produce good research, good qualitative research is systematic and thorough (Easterby-Smith et al., 2018) Hence, we have taken a systematic transparent approach. The approach can be followed in this chapter.

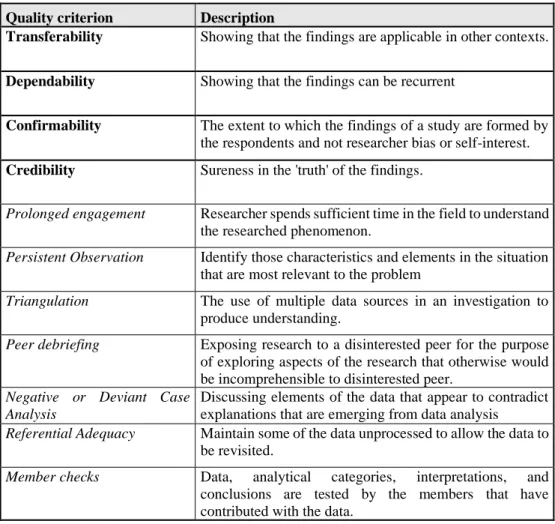

To establish quality in the study, not only is Easterby-Smith et al. (2018) arguments taken into account, but also Lincoln & Guba’s (1985) four criterions for reliability is used, i.e., Credibility (with seven sub-headings), Transferability, Dependability and Confirmability. These criteria followed by a description can be seen in Table 3. Lincoln & Guba (1985) argues that when evaluating research of qualitative nature, it is vital that the examiner gets the chance to evaluate the study and determine whether the result of the research is reliable or not. How the research has met these criteria can be seen in 6.2, it provides the basis for the examiner to determine the trustworthiness of the study.

Phase Description of process

1. Familiarizing yourself with your data

Transcribing data (if necessary), reading and re-reading the data, paying attention to occuring patterns.

2. Generating initial codes

Coding interesting features of the data in a systematic fashion across the entire data set, collating data relevant to each code. Documenting how patterns occur.

3. Searching for themes Combine codes into potential themes, gathering all data relevant to each potential theme.

4. Reviewing themes

Checking if the themes work in relation to the codes (Phase 1) and the entire data set, generating a thematic ‘map’ of the analysis. If analysis is incomplete, go back and find missing parts.

5. Defining and naming themes

Ongoing analysis to refine the specifics of each theme, and the overall story the analysis tells, generating definitions and names for themes and documenting what makes the themes interesting.

6. Producing the report

Selection of vivid, compelling extract examples, final analysis of selected extracts, relating back of the analysis to the research question and literature, producing a scholarly report of the analysis

Research method

21

Table 3: Quality criterion described, based on (Lincoln & Guba, 1985), inspired from (Eriksson, 2014)

Quality criterion Description

Transferability Showing that the findings are applicable in other contexts.

Dependability Showing that the findings can be recurrent

Confirmability The extent to which the findings of a study are formed by the respondents and not researcher bias or self-interest.

Credibility Sureness in the 'truth' of the findings.

Prolonged engagement Researcher spends sufficient time in the field to understand the researched phenomenon.

Persistent Observation Identify those characteristics and elements in the situation that are most relevant to the problem

Triangulation The use of multiple data sources in an investigation to produce understanding.

Peer debriefing Exposing research to a disinterested peer for the purpose of exploring aspects of the research that otherwise would be incomprehensible to disinterested peer.

Negative or Deviant Case Analysis

Discussing elements of the data that appear to contradict explanations that are emerging from data analysis

Referential Adequacy Maintain some of the data unprocessed to allow the data to be revisited.

Member checks Data, analytical categories, interpretations, and conclusions are tested by the members that have contributed with the data.

3.9 Ethical consideration

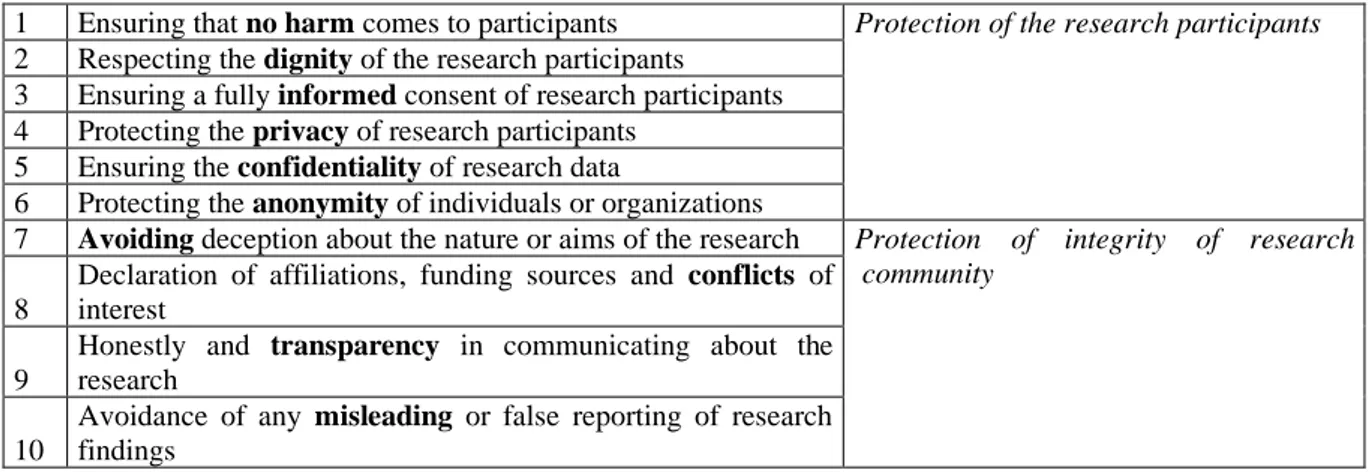

The research community in management research had a relaxed approach to ethical considerations until the 2000’s (Easterby-Smith et al., 2018). Easterby-Smith et al. (2018) discusses that the main goal is to ensure no harm to the participants of a study. Since people participating in interviews are exposed to different kinds of potential societal harms, the ethical aspects are considered of utmost importance to us. Also, the fact that we are gathering data from AFAIR-connected businesses makes it very important to not jeopardize the trust for Jönköping University or the research community in any kind of way. To avoid any kind of social problems occurring to the participants of a study Bell & Bryman (2007) suggest ten principles of ethical practice, described in Table 4.

Research method

22

Table 4: Ten principals of ethical practice, adapted from Bell & Bryman (2007).

1 Ensuring that no harm comes to participants Protection of the research participants

2 Respecting the dignity of the research participants 3 Ensuring a fully informed consent of research participants 4 Protecting the privacy of research participants

5 Ensuring the confidentiality of research data

6 Protecting the anonymity of individuals or organizations

7 Avoiding deception about the nature or aims of the research Protection of integrity of research community

8

Declaration of affiliations, funding sources and conflicts of interest

9

Honestly and transparency in communicating about the research

10

Avoidance of any misleading or false reporting of research findings

During the whole research process, we have had the above-mentioned principles in mind. To ensure that no harm came to the participants, not physically nor mentally, participation in the study was always voluntary. Prior to the interviews we informed the interviewee about the purpose of the research and the interview itself. This was done to make the interviewee understand the nature of the study and their role in it as well as how their interview was to be analyzed. The interviewees were also informed about their confidentiality in the study, to protect them from any discomfort. The participants of the study were also begged to fill in a GDPR consent form prior to the interviews, see appendix 2, to ensure that we were in line with the GDPR requirements. The interviews were recorded through Zoom or with a cellphone with the consent from the interviewee. Furthermore, the participants of the study were offered a full transcript of their interview for their consent to add or remove parts of the interview that they did not feel comfortable sharing.

Empirical Findings

23

Empirical findings

In the following sections, the empirical data analysis and the empirical data is presented. The data is collected through qualitative interviews.

4.1 Empirical Data Analysis

In the following a description of how the thematic analysis’ step 1-5 was conducted (Braun & Clarke, 2006).

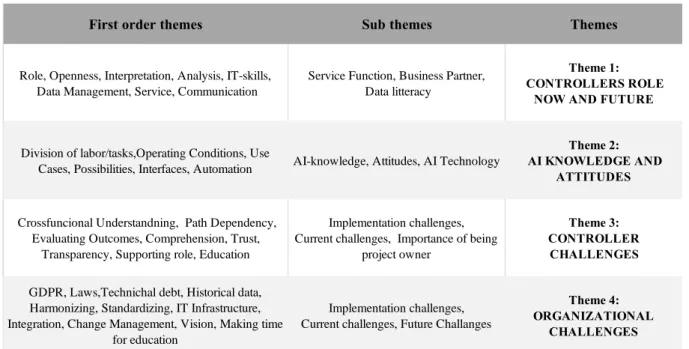

The data analysis began by reading and transcribing the interviews, similar to the familiarization step where the researchers read or listens to the interviews at least once (Braun & Clarke, 2006). When the transcriptions where done, an excel sheet was created. The empirical data analysis continued in Excel, where sentences and paragraphs from the transcriptions that potentially were connected to the research questions were identified and pasted into the Excel sheet in a systematic way. The segments of data were then coded into words describing the data, generating initial codes (Braun & Clarke, 2006). The codes and transcriptions were re-read to ensure that no codes were missed. This resulted into 70 codes. After re-reading the data and having thorough discussions about it, 29 first order themes emerged, a separate document was created where a definition of each theme was created, to ensure that the researchers had the same interpretation (King & Brooks, 2017). What constitutes a theme in this research is ‘recurrent and distinctive features of participants’ accounts, characterizing particular perceptions and/or experiences, which the researcher sees as relevant to the research question’ (King and Horrocks, 2010, p. 150). Sessions where we wrote the themes on a whiteboard to be able to structure them was conducted, this led to ten sub themes and from those, four themes emerged, of which theme 3 and theme 4 are closely connected, see Table 5.

Table 5: First order themes, Sub themes and Themes

First order themes Sub themes Themes

Role, Openness, Interpretation, Analysis, IT-skills, Data Management, Service, Communication

Service Function, Business Partner, Data litteracy

Theme 1: CONTROLLERS ROLE

NOW AND FUTURE

Division of labor/tasks,Operating Conditions, Use

Cases, Possibilities, Interfaces, Automation AI-knowledge, Attitudes, AI Technology

Theme 2: AI KNOWLEDGE AND

ATTITUDES

Crossfuncional Understandning, Path Dependency, Evaluating Outcomes, Comprehension, Trust,

Transparency, Supporting role, Education

Implementation challenges, Current challenges, Importance of being

project owner

Theme 3: CONTROLLER

CHALLENGES

GDPR, Laws,Technichal debt, Historical data, Harmonizing, Standardizing, IT Infrastructure, Integration, Change Management, Vision, Making time

for education

Implementation challenges, Current challenges, Future Challanges

Theme 4: ORGANIZATIONAL

Empirical Findings

24

4.2 Results

Based on the empirical data analysis, four themes on how the controller function is changing due to AI and challenges related to it emerged. Theme 1, (Controller Role now and future), and Theme 2, (AI knowledge and attitudes) relates mainly to research question 1: How is the role

of the controller changing due to the implementation of AI in manufacturing companies?

Theme 3, (Controller Challenges) and Theme 4 (Organizational Challenges) relates mainly to research question 2: What are the challenges relating to the change that comes with the

implementation of AI on individual and organizational level? Table 5 contains a detailed

version of the themes. While these themes and sub themes are divided based on our empirical data analysis, we acknowledge the fact that there are overlaps between them, no qualitative research promises arranged, stand-alone categories (Saldana, 2016).

4.3 Theme 1 – Controller characteristics now and in the future

Both the experts in business administration and the controllers being interviewed, named financial understanding and analytical skill as the most important skills for a controller to have today. Other skills being mentioned were data management, i.e., retrieving and gathering data from different systems within the organization, and supporting business, i.e., communicating and explaining the data to decisionmakers within the organization. Half of the controllers and all the experts talked about the developing role of the controller, where the role has gone from the main tasks being checking and controlling the financial data for errors, into a more active role within the organization where the controller interacts with different departments and decision-makers within the organization. One of the business administration experts described the role in the following way:

“The controllers have been dealing with the information, aggregating information and providing information to the top management in order for them to make decisions based on this information, I think the controller functions have changed quite a lot since then. I think it gained some more strategic importance. It’s controllers today that are also making decisions, that divides their parts of the decision-making together with the top managers. Some controllers enter the top management teams even. So, the control functions have been elevated. The controller’s role is much broader today than it used to be.”

This specific description of the controller and their advanced role was not entirely uniform with the role description made by other experts and controllers being interviewed. Most of the controllers mentioned that they were highly involved in the decision-making process, but mainly acting as support for management and not taking strategic decisions themselves. However, all the controllers being interviewed shared the view that the controller’s role had become much broader over the years, especially since there are controllers in even more areas than just the finance department. One of the controllers describe the role and what parts they felt where the most important in this way:

“The analytical ability is incredibly important. I also feel that it is important to be able to translate the analysis into something concrete that the business can then make a decision on. Then I also think that if you want to be efficient as a controller, you should also have qualities around stakeholder management, those parts you cannot get around, because the controller becomes a bit of the spider

Empirical Findings

25

in the web. Then it probably depends a bit on what form of controller you are also, because it can be that it can look very different.”

One of the business administration experts brought up that there may be a difference in the controllers view of their current and the future role, depending on their age, education, and professional experience, with the older controllers having a more traditional view:

“I do think that as a controller you need to have… You need to be able to go into the details of things. I mean it's nice to have a general interest for the business and so on. And it’s important to understand the business, but you also have to be ready to dig into the numbers so to say. I recently talked to an old colleague from my studies, and she is now a controller. She talked about that some of her younger colleagues who are very into this idea of a business partner role, might be a bit hesitant to dig into the analytical part. You know going into deviations when we look at this little item produced for this customer. Why did we have a deviation in material costs and go into that.”

Another part of the controller function that varied greatly was the tools they were using for data analysis and visualization. PowerBI, Tableu, Qlik, and Alteryx where among tools mentioned being used by controllers within their organization, but not necessarily by the controllers themselves. SAP and Excel were the two tools mentioned by all the controllers and the experts, as the standard tools for data management and analysis. The reasons for not learning these new tools are different, some of the controllers mention lack of time and learning opportunities as their main challenges, while others struggle to see the benefit and future use of the software both within the organization, but also if they change jobs and organizations. One of the controllers brings up the issue in the following way:

“There are other such tools and since, because they are doing so much with digitization now, it feels a bit like… Sometimes you talk about this tool and sometimes you talk about another tool. And then you become a little bit hesitant, should I really devote time to this. What if they decide another thing later? Not that time might be completely wasted… But right now, it feels a little, a little bit of uncertainty. “

Even though they are currently pre-occupied with their organization’s digitization efforts, the interviewed controllers were welcoming of AI. The controllers believed AI would free up their time from time-consuming repetitive tasks, such as data retrieval and low-level analysis, and give them more time for value-creating tasks that would bring more benefits to the organization. Some controllers had very high belief in AI and thought it would be able to help them with

“everything” when asked, while others had a more nuanced and detailed list of tasks, for

example:

“I think that with AI, the kind of pulling the data together will more or less, not be a big part of the controller’s task anymore because this is really something that AI can do even in a better way when you have the data available and the systems also available, so I think. That this is more less something that AI can totally take over. I also think the interpretation of the data is also something that AI can possibly do, by learning as well. But I think that developing new ideas to more or less act and react and be able not only to react, but to kind of have a