How managerial discretion impacts the

organizational performance of municipal

corporations

Master Thesis within Business Administration

NUMBER OF CREDITS: 30 ECTS PROGRAMME OF STUDY: Civilekonom

AUTHORS: Olof Amade Nylander & Alexander Gjersvold JÖNKÖPING May, 2020

Abstract

Master Thesis within Business Administration

Title: How managerial discretion impacts the organizational performance of municipal corporations

Authors: Olof Amade Nylander & Alexander Gjersvold Tutor: Timur Uman

Date: May 2020

Keywords: Municipal corporations, Performance, Managerial Discretion, Contingency Theory, Upper Echelon Theory, Control Systems, Triple Bottom Line, Organizational Performance

Municipal corporations play an important role in our society by providing socially needed services to its citizens. The performance of those corporations are important as the services impact our way of living. When examining the performance of municipal corporations, the social and environmental aspects need to be considered along the financial aspect, considering their multifaceted nature of organizational goals they are expected to achieve. Managerial discretion has previously been used to explain the outcomes of firms as it would allow the CEO to shape the organization in the most beneficial way.

The purpose of this thesis is to examine how managerial discretion impacts the organizational performance within a municipal corporation and how different management control systems affect that relationship. The research is done using a quantitative method of surveys sent out to CEOs of municipal corporations working within the utility industry of Sweden and by using the financial reports of these companies for the fiscal year 2018.

The results show a positive significant relationship between managerial discretion and financial performance but no significance regarding the social or environmental performance. The usage of traditional management control systems had a negative effect on the relationship between managerial discretion and financial performance.

The thesis contributes to the literature as it strengthens the notion that managerial discretion impacts organizational outcomes. Furthermore, it examines how different types of control systems impact that relationship.

Acknowledgements

Firstly, we would like to thank our supervisor Professor Timur Uman. During the supervisions, he guided us along the way by being clear, collaborative, and motivational to keep on going.

Secondly, we would like to thank our opponents in the seminars as their feedback has been of great value to the thesis. Thirdly, we would like to thank the CEOs who took the time in their busy schedule to respond to the survey as their participation was crucial to the thesis.

Finally, we would like to thank our family and friends for their support during this intensive period of time.

Jönköping, May 2020

___________________________ ___________________________

Table of Content

1.0 Introduction ... 9

1.1 Background ... 9

1.2 Problematization ... 12

1.3 Purpose and Research Question ... 16

1.4 Delimitations ... 16

2.0 Literature review ... 17

2.1 Performance (Triple bottom line) ... 17

2.2 Managerial discretion... 20

2.2.1 Managerial discretion and organizational performance ... 22

2.3 Contingency theory ... 23

2.4 Upper Echelons Theory ... 23

2.5 Management Control systems ... 24

2.5.1 TPMCS ... 25

2.5.1.1 TPMCS role in the relation between CEO MD and Organizational Performance ... 26

2.5.2 NPMCS ... 27

2.5.2.1 NPMCS role in the relation between CEO MD and Organizational Performance ... 28

2.6 Overview of theoretical model... 29

3. Method ... 30 3.1 Research Approach ... 30 3.2 Research Method ... 30 3.3 Research Strategy... 31 3.4 Data collection ... 32 3.5 Sample Selection ... 32

3.6 Analysis of non-response bias ... 33

3.7 Operationalisation ... 34

3.7.1 Dependent variable - organizational performance ... 34

3.7.2 Independent variable - managerial discretion ... 37

3.7.3 Moderating variables - control systems ... 37

3.7.4 Control variables ... 38

3.8 Data analysis ... 40

3.9 Reliability, validity and generalizability ... 41

3.10 Information Evaluation ... 42

3.11 Ethical consideration ... 43

4.1 Descriptive statistics ... 44

4.1.1 Dependent variables ... 44

4.1.2 Independent variables ... 45

4.1.3 Moderating variables ... 46

4.1.4 Control variables ... 47

4.2 Spearman correlation Matrix ... 49

4.3 Multiple Linear regression analysis ... 52

4.4 Hierarchical moderating multiple regression analysis ... 55

4.4.1 Moderating effect TPMCS ... 56

4.4.2 Moderating Effect NPMCS.1 Reward Systems ... 58

4.4.3 Moderating Effect NPMCS.2 Work environment ... 60

4.5 Hypothesis... 63

5.0 Discussion ... 64

5.1 Organizational performance... 64

5.2 Managerial Discretion and organizational performance ... 66

5.3 Moderating effect of the control systems ... 68

6.0 Conclusion ... 70 6.1 Overarching Conclusion ... 70 6.2 Theoretical Contributions ... 72 6.3 Practical Contributions... 73 6.4 Empirical contributions ... 74 6.5 Limitations ... 76 6.6 Future research ... 77 7.0 References ... 78 Appendix ... 86

Appendix 1 Translated survey ... 86

Appendix 2 Checklist ... 89

List of figures

Figure 1 Overview of theoretical model

Figure 2 Standardized Two-Way Interaction effects TPMCS and Perceived Financial Performance

List of tables

Table 1 Analysis of non-response bias

Table 2 Descriptive Statistics factual and perceived performance Table 3 Descriptive Statistics managerial discretion

Table 4 Descriptive Statistics Traditional management control systems Table 5 Descriptive Statistics New Public management control systems. Table 6 Rotated Component Matrix control systems

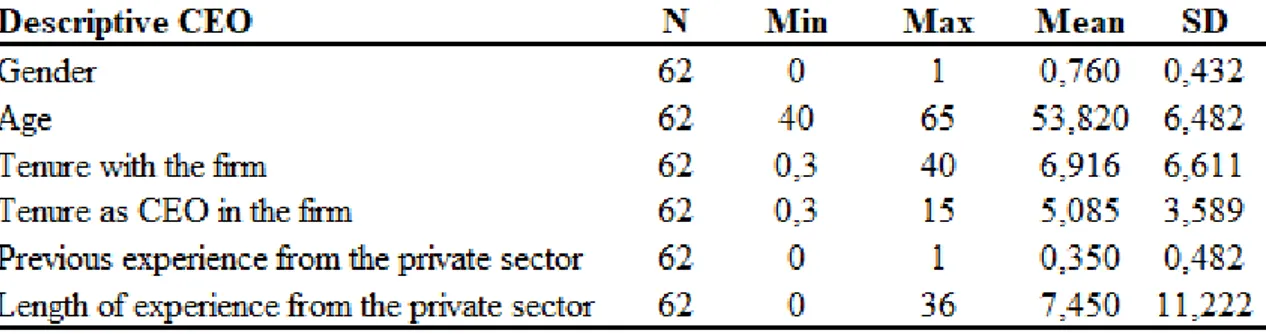

Table 7 Descriptive statistics of new moderating variables Table 8 Descriptive Statistics CEO information

Table 9 Descriptive Statistics industry

Table 10 Descriptive Statistics part of the country Table 11 Descriptive Statistics firm size

Table 12 Spearman Correlation Matrix

Table 13 Multiple regression analysis on factual financial performance Table 14 Multiple regression analysis on factual social and environmental Table 15 Multiple regression analysis on perceived performance

Table 16 Hierarchical Linear Regression Model TPMCS - Factual Performance Table 17 Hierarchical Linear Regression Model TPMCS - Perceived Performance Table 18 Hierarchical Linear Regression Model NPMCS.1 - Factual Performance Table 19 Hierarchical Linear Regression Model NPMCS.1 - Perceived Performance Table 20 Hierarchical Linear Regression Model NPMCS.2 - Factual Performance Table 21 Hierarchical Linear Regression Model NPMCS.2 - Perceived Performance Table 22 Hypothesis overview

List of abbreviations

CEO - Chief Executive Officer

EBITDA -Earnings before interest, taxes, depreciation, and amortization EP - Environmental Performance

GRI - Global Reporting Initiative FFP - Factual Financial Performance FSP - Factual Social Performance

FEP - Factual Environmental Performance MCS - Management Control Systems MC - Municipal Corporation

MD - Managerial Discretion NPM - New Public Management

NPMCS - New Public Management Control Systems PFP - Perceived Financial Performance

PSP - Perceived Social Performance

PEP - Perceived Environmental Performance

TPMCS - Traditional Management Control Systems TBL - Triple Bottom Line

9

1.0 Introduction

The introduction consists of the background of the research topic, followed by the

problematization. Based on those, the purpose of the paper and the research questions are presented, followed by the delimitations.

1.1 Background

Sweden has 290 municipalities which vary notably in size as the largest inhabits close to a million citizens while the smallest sits at around 2 500 citizens. They all have certain requirements to provide for its citizens like education, housing, water and electricity, in addition to having the ability to affect the tax rate for its citizens. Municipal corporations (MC) are used as a tool for municipalities to perform their intended services in an external entity that is fully or partially owned by the local government, e.g. the municipality. The MC competes against companies in the private sector while simultaneously trying to serve the best public interest of the municipality. MCs in Sweden face the same legislation as other limited liability companies (or any other legal form of business) while also having to adapt to the Municipality Act introduced in 1991 which among other things limits the profit seeking ability of MCs, exceptions apply for certain industries, e.g. the electricity industry (Ellagen, 1997:857). It also states that a corporation controlled by the municipality needs to serve a purpose for its citizens, and that they are limited to only operate within their own region. The marketization of municipal responsibilities is created with the goal of implementing the efficiency and effectiveness from corporations as outlined in the New Public Management (NPM) by Christopher Hood in 1991. The shift towards using more corporations to deal with the responsibilities of local government has started since the 1980s and has spread across Europe (Argento, Grossi, Tagesson, & Collin, 2010

)

. In Sweden, it has created issues where the financial aspects of a corporation have challenged the social responsibilities of a municipality and public access to official documents that municipalities must follow.

Being in the public eye, MCs are under a lot more scrutiny than other corporations because they are in the business of public service and have far more stakeholders that are dependent on them. MCs also must follow the principle of public access (Tryckfrihetsförordning, SFS 1949:105) as any other part of the government meaning that journalists and citizens have

10 considerably more access to information compared to other companies. In December 2019 a newly formed MC that handles the garbage collection in three different municipalities had to be saved from bankruptcy by the respective municipalities (Boström, 2020). Since the MC had monopoly of this service within the municipalities, they were forced to back them, as otherwise no one would handle the garbage collection within the region. Swedish municipalities take up a large part of the nation's GDP as in 2018 it contributed to 14% of the total (SCB, 2019), with MCs contributing considerably. The performance of MCs is important for the public to avoid similar situations where municipalities have to cover their losses, especially when taking into account that roughly 80% of Swedish municipalities are facing budget deficits and cost cutting in areas such as schools and healthcare (SKR & SVT, 2019). Considering the number of stakeholders within the municipalities and being a large part of the country's economy, the performance of the MC becomes an important area to examine.

Unlike most private companies where financial performance is the end-all goal, MCs have goal multiplicity, which means that they are pursuing multiple goals and outcomes, where public service is their perceived primary goal regardless of what sector the MC is operating within. When trying to assess the well-being and performance of a firm, one tends to go the route of using performance measures, which are a given part of the assessment of any firm, regardless of which sector the firm operates in. When carrying out the analysis, the focus usually lies with the financial performance. However, financial performance does not capture the entirety of the firm's performance, especially MCs, which do not identify financial performance as the ultimate outcome (Uman, Smith, Andresson & Planken, 2018). Even though profitability is the main purpose of a limited liability company, in the case of MCs, the profitability and financial performance of the corporation is very important, but primarily as a means to stay afloat and avoid previously mentioned situations where the municipality has to save the MC from bankruptcy. Municipalities and their corporations also have to adhere to the self-cost principle (Kommunallagen, 2017:725, 2:6) which means that they are only allowed to charge the same price for a service or product as it costs to provide it, meaning that in theory there should be no profits but there are exceptions for certain industries like the electricity industry (Ellagen, 1997:857). If the focus does not lie with maximizing profits and paying out dividends to its owners, what is performance in MCs given their status in society and the multiplicity of their goals?

11 Among their multitude of goals, public service quality and non-financial performance such as the ability to efficiently allocate resources in order to satisfy the needs of the stakeholders within the municipality (Uman et al., 2018), which constitutes as social performance, are two of the performance aspects that are perceived to be vital for a MC. Especially when considering the industries that MCs operate in, e.g. water, garbage, energy and housing which are all crucial to society. Another performance aspect which is also regarded as important in Sweden is the environmental performance, particularly for the MCs as they are concerned with the long-term wellbeing of the municipality while also trying to be a role model for private firms in their environmental and social impact (Knutsson, Mattisson, Ramberg & Tagesson, 2008). The social and environmental performance measures and highlights the firm’s success in meeting its corporate social responsibilities to various stakeholders, such as shareholders, customers, and society (Turban and Greening, 1997). Along with the financial performance of the firm, the three aforementioned measures are encapsulated in the Triple Bottom Line (TBL) framework. Pressure from the many stakeholders MCs are accountable to such as citizens and government have furthered the need for the TBL framework (Elkington, 1998) within MCs. TBL allows for organizations to consider the broader perspective while measuring performance, impact and outcomes, which results in creating greater business value for the firm if their performance is in line with stakeholder expectations (Elkington, 1998).

But what affects all the aspects of performance in an organization? Previous research has looked at the top management team (TMT) (Norburn & Birley, 1988), others have looked at CEO characteristics (Jenter & Kanaan, 2015) or firm characteristics like strategy and structure

(Otley, 1999). There are many different ideas of what could affect the performance, but what actually is it? Different aspects may explain types of performance, but there is a perceived lack of a holistic view, what could that holistic view be?

12

1.2 Problematization

The measurement of organizational performance is expected to be vital for all organizations to evaluate the actions taken by the firm and its managers (Durst, Hinterregger, Zieba, 2019). The term organizational performance is a multidimensional one since it encapsulates the performance of the corporations as a monolithic unit, instead of focusing on one aspect of the corporation’s performance. The organization is performant when it is efficient and effective at the same time. Therefore, the organizational performance is a function of two variables, efficiency and efficacy (Taouab & Issor, 2019), especially for MCs considering their goals multiplicity and that MCs are responsible for vital functions for the society, if they are not performing well it can have devastating effects as the municipality might have to bail them out.

MCs must ensure that the stakeholders in their municipality can rely on the MC providing them with needed services delivering the services and reaching expected outcomes efficiently and effectively. They must perform to the satisfaction of the stakeholders, while also performing well enough financially to keep them afloat and following the self-cost principle (Kommunallagen, 2017:725, 2:6). Additionally, they are regarding the TBL framework, since their diversity of goals usually is in line with environmental and social sustainability (Jörby, 2002). While considering the multifaceted nature of performance, one might wonder what drives the MC to perform in all aspects to the satisfaction of the stakeholders? In the context of municipal corporations, you have a situation where sole or shared ownership belongs to the municipalities, however, the real owners, the citizens are very dispersed, but are to be seen as owners since the purpose of a municipality is to service them (Sørensen, 2007). Citizens provide the capital by paying taxes to the municipality that gets distributed among the different services required to keep the society running. The citizens are also represented by politicians on the board, in fact 92% of the board in a MC is based on their political profile (SOU 2015:24, p.344) and given their political agenda, they have different ideas of how the organization should be run. When politicians are appointed on the board, differences are cast aside, as they are required to work in the best interest of the MC. As elections are held every fourth year there could be shifts in the ruling majority of a municipality and therefore result in a change of agenda and strategic directions within the MCs. This further adds another dimension of dispersion. In a situation like this, with dispersed and diffused ownership, one could argue that a strong leader is important to manage the short-term management while implementing the more long-term

13 directions from the new board. It could be argued that keeping the CEO around in times of changes would be important to the success of the MC. In US context this results in the duality role of the CEO and chairman (Donaldson & Davis, 1991). However, this is not allowed by law in a MC, yet the dispersion suggests that the CEO has a very strong position in relation to the dispersed owners and dispersed board.

Researchers have traditionally focused on the effects of the TMT as a single unit – implicitly treating the CEO as equally powerful and influential as other top managers (Hambrick and Mason, 1984), and that has also been the case when studying TMTs and MC outcomes (Uman et al., 2018). However, the TMT usually reports directly to the CEO, and the CEO has the authority to fire other top managers, therefore one can argue that implicitly treating the CEO as an equal to other senior managers will yield an misrepresented image of the role of the senior executive. Based on this assumption, the focus of this study is on the CEO and his/her role in driving the performance of the organization. The CEO, who has operational responsibility and by extension is responsible for the organizational performance, plays the key role in controlling, organizing and directing the entity and strategically orienting it towards achieving the goals of the entity (Castanias & Helfat, 1991).

But what about the CEO is it that drives performance? Researchers have looked at different characteristics like the managerial focus (Smith & Uman, 2015), while others have looked at which characteristics and abilities could affect the performance (Kaplan, Klebanov, & Sorensen, 2008). There are still contradicting views on the importance of a CEO but as argued by Finkelstein, Hambrick, & Cannella (2009, p. 26) the importance relies on the amount of leeway available to the CEO, and on the strategic decisions and actions made by the CEO which are of strategic importance and later are reflected in the organizational performance. This view was first introduced in 1987 by Hambrick and Finkelstein called managerial discretion (MD). The definition of MD is the amount of latitude of actions that a manager has when it comes to actions decided by the CEO in any given situation. The paper was introduced to deal with the debate among organizational theorists whether organizations have control over their own destiny or not. MD was brought forth as the explanation for these differences as the leeway available to the top executives varied and therefore so did their impact on the organization. Shen and Cho (2005) later added to the definition by mentioning that MD also includes the latitude of objectives which stipulates how much leeway the CEO has to pursue their own interests rather than the stakeholders. MD has its importance in the academic world

14 as high leeway should increase the performance (Finkelstein & Boyd, 1998; Finkelstein & Hambrick, 1990 & Frederickson, 1999) but it has mostly been researched in the context of private corporations where the performance is mostly focused on the financial aspects and it has previously been used to explain a wide range of outcomes within organizations. Some examples include executive turnover (Shen & Cho, 2005), CEO compensation (Finkelstein & Boyd, 1998) and environmental commitment (Aragón-Correa, Matı́as-Reche, & Senise-Barrio, 2004). The public sector has had a tradition of being governed politically, which became particularly complex with the emergence of different management cultures. The attempts to separate administration from policy increased the presence and need of MD (Karlsson, 2019).

CEOs can shape their own discretion in different manners. To solely have the opportunity for latitude of action is insufficient, CEOs must also recognize that it is there to be used (Karlsson, 2019). Effective CEOs find and create options that are not accessible for others. This may be done through insights, persistence, or sheer willpower. For the CEO in a low MD situation, there is not a strong connection between current performance and a belief in the correctness of current organizational strategy and leadership profiles. In instances with low discretion, performance is derived from uncontrollable factors, such as the environment (Finkelstein, et al., 2009). A high level of MD increases the ability of the CEO to influence firm performance directly and significantly on organizations, as a high level of MD entails different options for the CEO to choose from. Considering the multiplicity of options available, the CEO might be able to make more weighted and at the same time better decisions. Ultimately, the level of MD paired with the experiences and preferences of the CEO substantially influence what happens to their firm.

The role that the CEO plays in shaping conditions and processes both inside and outside the firm, impacts the ability of the firm to perform according to the strategic choice theory which refers to "the process whereby power holders within organizations decide upon courses of strategic action" (Finkelstein, et al., 2009). The range of actions available for a CEO is wide and covers everything from how to allocate resources efficiently, their ability to make decisions and action, and form the organization is bar none (Child, 1972). However, the CEO does not operate in isolation, the decisions made or even considered by the CEO are affected by the current structure and values within the organization. A strategy that works for one firm is not directly transferable to a similar corporation, as the culture and structure of the organization might be completely disparate. In any given organization there are control systems that affect

15 the way the organization operates, elements like planning and the structure are examples that top executives use to control the decisions that its subordinates make (Malmi & Brown, 2008). Management control systems (MCS) have evolved from providing financially quantifiable information to include a much broader perspective, e.g. information related to customers, competitors etc., to assist managerial decision making, combined with an array of decision support mechanisms and social controls (Malmi & Brown, 2008). Management controls are multifaceted, they are necessary to ensure that the objectives of the organization are being worked towards, and safeguard against the risks that management or employees will do something that is detrimental to the organization or failing to do something they should do. However, MCS also are used when instilling the culture of the organization (Malmi & Brown, 2008).

The different management control systems grouped together by Malmi and Brown (2008) are used to control the subordinates but will also affect the top executives as well. Elements that have been called traditional public management control systems (TPMCS) (Uman et al., 2018) include administrative and planning which impacts the latitude of actions available to the CEO that he/she needs to adjust to. Just as with the marketization of MCs, new public management also has impacted the control systems with the new public management control systems (NPMCS) (Uman et al., 2018) as it incorporates the idea of reward systems and measurements of performance (Hood, 1991). These components will interact with the discretion of the CEO and combined they will affect the performance. It is important for an organization to have a fit among their usage of control systems and the MD, in an environment of high discretion the CEO should be judged by the performance of the organization which is why NPMCS like performance measures and reward systems would be of great importance. If the focus lies on the usage of budgeting and planning the manager is not able to showcase their ability in the decision-making as actions are already planned out.

As aforementioned, most studies are on private corporations and have been set in North America or the UK. The public status and scrutiny of the MCs in Sweden comes with increased pressure on the MC being well-run. Considering the importance of MCs to Swedish society, them being responsible for delivering services that are vital for society to properly function. The gap of research on the corporate governance of MCs in Sweden is apparent and needs to be filled. Additionally, of the variety services delivered, the choice fell on municipal energy, water and waste, since there is a perceived research gap concerning the corporate governance

16 of these industries as previous research conducted here has mostly been focused on the public housing, where MCs are highly represented (E.g. Chanko & El-Bazi, 2019 & Gårdh & Zyrlite, 2019).

1.3 Purpose and Research Question

The purpose of the paper is to explore how CEO’s managerial discretion relates to organizational performance of municipal corporations and how this relationship is contingent on and moderated by management control systems in use.

RQ1: How does the CEO’s managerial discretion relate to organizational performance of municipal corporations?

RQ2: How management control systems moderate the relationship between CEO’s managerial discretion and organizational performance in municipal corporations?

1.4 Delimitations

One limitation of this paper is that it will only look at the managerial discretion of the CEO in a MC, instead of researching the entirety of the top management team. The assumption that this study focuses on, is that the CEO and her/his role in driving performance of the firm. By delimiting the paper to this assumption might be an oversimplification of triggers and driver behind performance.

17

2.0 Literature review

The literature review presents the main underlying theories and concepts of the thesis, which are the performance, triple bottom line theory, managerial discretion, contingency theory and controls systems. Thereafter, these theories will be related to each other in different aspects and will merge into three proposed hypotheses.

2.1 Performance (Triple bottom line)

The concept of performance is a vital one when researching corporations of any nature. Performance is a perception of reality that can be both subjective and objective in nature and measurement, which may serve as an explanation of the multitude of critical reflections on the concept and its measuring instruments. Due to the subjective nature of performance, there are multitude of definitions attributed to the concept of performance, leading to a concept that is very broad (Darwish & Potočnik, 2015). Researchers have adopted both objective and subjective measures for assessing performance: objective measures involve using accounting data, while subjective measures involve the perceptions of managers when it comes to the performance of their firm. Whichever route is adopted, the goal is to explain what factors contribute to the superior performance of firms compared to their business rivals (Darwish & Potočnik, 2015).

The MC is the embodiment of the hybridization of the public and private sector, forming a hybrid organization (Collin & Tagesson, 2010). This hybridization of the public and private sector also represents a clash of competing institutional logics, in this case the market, corporation and state logics are mixed into a single entity. Each institutional logic is distinguished by particular organizing principles, practices, and symbols that influence organizational behavior (Thornton, Ocasio & Lounsbury, 2012). This means that the MC operates in a business-like manner and is governed with a political perspective in order to reach the objective of providing public services with public funding (Grossi, Thomasson, Kickert, & Randma-Liiv, 2015) while facing the multiplicity of goals and by adhering to different institutional logics, diverging performance goals may arise while dealing with the complexity of the different institutional logics embedded in the corporation.

The task of measuring and conceptualizing organizational performance in the context of a hybrid organization such as the MC, presents added complexity since one cannot directly adopt

18 and transfer concepts and measurements from the previous literature on entities that are wholly public or wholly private (Grossi, Reichard, Thomasson, & Vakkuri, 2017). According to the self-cost principle, MCs are not allowed to organize with the goal of making a profit in mind, and thus rendering financial performance as more of a control for the MC to stay afloat than an end-all goal (Kommunallagen, 2017:725, 2:6). However, there is a special legislature for certain industries that provides vital services for society, such as the Water Act and the Electricity Act that stipulate that MCs should be run in a businesslike manner (Vattenlag, 1983:291; Ellagen, 1997:857), thus emphasizing on the financial performance of the MC. However, MCs face multitudes of goals and outcomes when operating. Among their goals and outcomes, societal interests are expected to be at the forefront, which is often considered from a political viewpoint for sake of referencing and evaluating (Knutsson et al., 2008). Public service quality and non-financial performance such as the ability to efficiently allocate resources in order to satisfy the needs of the stakeholders within the municipality (Uman et al., 2018), are two examples of the performance aspects that are perceived to be vital for a MC. The performance of a MC depends on the ability of the firm to continually show its purpose and provide desirable outcomes to all its stakeholders (Knutsson et al., 2008). In order to face the continuously growing need and pressure from the stakeholders to explicitly communicate the performance of the MC the use of a strategic approach was adopted in the public sector. However, the implication of the decision made is that the objectives of the organization are ambiguous and considering the number of stakeholders which have ambiguous expectations, there is a large variance of expected results among the stakeholders (Knutsson et al., 2008).

The ongoing climate has raised questions about environmental issues on the political level in Sweden, and social issues are always on the agenda for the politicians, regardless of their political stance. There is pressure from the owner - the municipality (and by effect the state), from the mass media and from the stakeholders to commit to and comply with business practices which favors sustainability (Tagesson, Klugman & Ekström, 2013). The MC must meet the aforementioned pressure while still adhering to the Municipality Act which states that the objective of the MC is to provide services and facilities that are for the members of the municipality, however, the purpose of the MC must be public good and cannot be profit maximization (Kommunallagen, 2017:725, 2:1+7). Considering the goal multiplicity of MCs and their role in Swedish society, the fact that MCs are meant to serve as good examples for other firms and the fact that MCs are being scrutinized, the TBL serves a means to meet that

19 pressure and provide the Swedish companies with a good example on how to keep both sustainability and organizational performance in mind while running the firm. Organizational performance can also be referred to as the completion of a firm when compared to the goals and objectives of the organization (Almatrooshi, Singh & Farouk, 2016), in other words, their success is determined by the completion rate of their objectives and outcomes.

Value creation for stakeholders in hybrid organizations like MCs is the sum of social, financial and environmental performance outcomes (Ponte, Pesci & Camussone, 2017). The value creation itself is represented by the MC simultaneously pursuing all three objectives (Szekely & Knirsch, 2005) which creates difficulties in conceptualizing performance of MCs (Maine, Florin-Smauelsson, Uman, 2020). If MCs tries to focus on one facet of performance over the others, there is a risk for the MC to drift (Jones, 2007). If the MC loses sight of their intended mission, to serve the public, and goal multiplicity, and too much emphasis is being put on making profits, then the phenomena ‘mission drift’ occurs (Jones, 2007). However, if too much emphasis is being put on the social and environmental performance, which entails attention being diverted away from the financial performance by the MC, ‘revenue drift’ might occur, (Ebrahim, et al., 2014). The balancing act of their goal multiplicity, adds to the complexity of performance in a MC, however, what represents performance in MCs?

Financial performance is represented by the financial measurements in the financial statements, as previously discussed, the main aspect of the financial measurements is measured without profit maximization in mind, however depending on the industry, that changes. Ambiguity arrives when considering the social and environmental performance. Environmental performance (EP) has been defined as a “multidimensional construct” by Schultze & Trommer (2012), which represents the degree to which firms are able to live up to the stakeholders’ expectations of the MCs environmental work. This is done by the usage of different indicators, such as the use of raw materials (Schultze & Trommer, 2012). For a MC in the utility sector the use of various EP indicators such as emissions released, becomes vital in measuring their EP, however emphasis is also being put on implementing sustainable ways to operate (Tagesson et al., 2013), which can be translated into measuring the use of recyclable materials, feeding into the sustainable circular economy.

20 For the social performance, there is ambiguity when considering the definition of it, multiple researchers have proposed various definitions (e.g. Wood, 1991; Clarkson, 1995). The argument made by Wood (1991) is that social performance is “a business organization's configuration of principles of social responsibility, processes of social responsiveness, and policies, programs, and observable outcomes as they relate to the firm's societal relationships.” This definition is inherently vague but covers all the aspects of social performance of a MC, e.g. such as having programs for the health of its employees. The social performance of the MC is tied to the degree to which they prioritize the societal interests, which pressure from stakeholders have ensured is high (Tagesson et al., 2013). This leads to the MCs’ principles and policies of social responsibility of ethical and human issues being translated into observable outcomes (Wood, 1991), in the form of programs, or actions taken to ensure the social responsiveness of the MC. The social and environmental performance measures and highlights the firm’s success in meeting its corporate social responsibilities to various stakeholders, such as shareholders, customers and society (Turban and Greening, 1997). Social and environmental performance along with the financial performance of an entity constitutes the three facets of TBL. The framework is highly adaptable since a universal method for measuring the TBL does not exist. Neither is there a universally accepted method for measuring each category of the TBL individually. This perceived weakness of the system can be perceived as a strength since it allows the user to alter it to the different needs of different entities (Elkington, 1998). Since the framework is so adaptable and serves the MC well as a performance measurement considering their multifaceted nature of organizational goals (Grossi et al, 2019) , and also serves as a tool to conceptualize the organizational performance of a MC, we argue that organizational performance consists of the three facets that are included in the TBL framework.

2.2 Managerial discretion

Researchers have looked many at different potential drivers of organizational performance. Aspects like a firm's strategy and structure (Otley, 1999), others have looked at TMT characteristics (Norburn & Birley, 1988) while others have only looked at the CEO within that TMT (Jenter & Kanaan, 2015). There are still contradicting views on the importance of a CEO in the outcome of a firm but as argued by Finkelstein, Hambrick, & Cannella (2009, p. 26) the importance relies on the amount of leeway available to the CEO, and on the strategic decisions

21 and actions made by the CEO which are of strategic importance and later are reflected in the organizational outcomes. This view was first introduced in 1987 by Hambrick and Finkelstein called managerial discretion. Defined as the latitude of actions that managers possess, it has had its importance within the business world but also for researchers (Finkelstein & Boyd, 1998). It has previously been used to explain a wide range of organizational outcomes (Shen & Cho, 2005; Finkelstein & Boyd, 1998). In a high discretion environment, the CEO has a wide range of actions available and is able to better showcase their knowledge in the decision-making process. Hambrick and Finkelstein (1987) argue that discretion is determined by three different aspects: managerial characteristics, the internal organization, and the task environment. All these aspects can help enable or constraint the latitude of actions that a manager has access to, where managers who are bound by the environmental and organizational constraints are unlikely to have an important impact on the performance. The manager characteristics which is the focus of this research is determined by aspects like their aspiration, tolerance of ambiguity and their beliefs regarding one's locus of control (Finkelstein & Hambrick, 1987).

The constraints that managers are faced with are primarily unstated, but they are also to a large extent known to the manager meaning that they are somewhat aware of which decisions they have available to them (Finkelstein & Hambrick, 1987). As decisions are often met with some resistance or opposing views, the authority of that side needs to be considered meaning that a large investor possesses more power and influence on the manager than a single employee or customer. This led Finkelstein and Hambrick to describe constraint as a function of “the perceived radicality of an action and the relative power of those who see it as radical. A decision that lies outside of an important stakeholders” zone of acceptance will lead to negative repercussions e.g. firing or demotion in response to said action. If there is a miss match among the zone of acceptance from the stakeholder and the MD there will be agency costs, for example in a situation where the zone of acceptance is larger than the managerial discretion stakeholders would want the manager to act with more risk potentially higher rewards (Ponomareva, 2016).

Shen and Cho (2005) noted that managerial discretion has different meanings in the management and economic literature. In management it refers to the options available to the executives while for economists it means their ability to pursue their own interests and incentives to undertake certain actions. This led to the idea of splitting the latitude into two areas, objectives and actions. Latitude of actions being the one close to the initial idea by

22 Finkelstein and Hambrick which describes the range of strategic choices they must accomplish the goals of the stakeholders. From the actions perspective a manager's capacity to operate and influence the outcome is of importance. Objectives, however, describe the ability to pursue the manager's own interests rather than the stakeholders without getting any consequences of their actions. Within this view agency theory proposes that managers have an incentive to act in their personal interests rather than the best interests of the stakeholder (Jensen & Meckling, 1976).

2.2.1 Managerial discretion and organizational performance

The CEO is hired to work on behalf of the owners and is judged on his or her ability to achieve the goals and outcomes set by the owners. In a MC ownership belongs to the citizens of the municipality (Sørensen, 2007) so the ownership is very dispersed which highlights the importance of the CEO to set a clear direction of the organization with all different political preferences from the board. For a CEO to actually have an impact on the organization they will need some leeway for strategy decisions (Hambrick & Finkelstein, 1987) and in public organizations MD has been found to be substantial, particularly in years of poor performance where managers remained in charge with the confidence of the board (Cragg and Dyck, 1999).

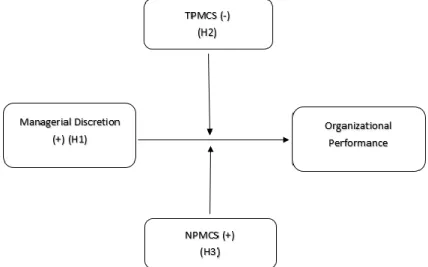

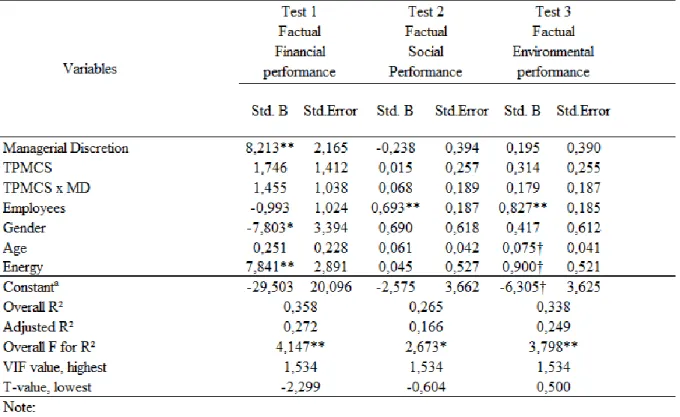

The link between MD and firm performance has been studied and proven quite extensively following the publication by Finkelstein and Hambrick in 1987, most have shown that higher MD has led to an increase in firm performance (Agarwal, Daniel & Naik, 2009; Lilienfeld-Toal & Ruenzi, 2014). When managers are given a higher amount of discretion, they are able to shape and develop the organization in the most efficient way based on their expertise and experience, showcasing their importance to an organization. Performance in MCs differs from normal firm performance because of their goal multiplexity of working for its citizens rather than just profits but the work of a CEO should remain similar to the work within the private sector as the objective is to achieve the goals set by the board. Thereby we present our first hypothesis:

Hypothesis 1:

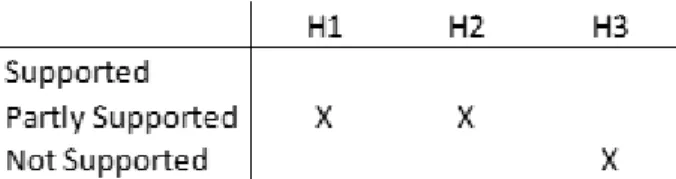

Higher perceived managerial discretion will lead to a higher organizational performance for municipal corporations.

23

2.3 Contingency theory

The internal and external environment will be always different for companies meaning that there is no perfect answer on how to run them. Structural contingency theory states just that, there is no ideal way to structure an organization or make decisions, it is based on the internal and external environment that will always be unique (Otley, 2016). Contingency theory began in the 70s as an attempt to explain the differences in management styles and how those came about. In an overview of the contingency theory in 1980 by Otley he concluded that “a contingency theory must identify specific aspects of an accounting system which are associated with certain defined circumstances and demonstrate an appropriate matching” (p.413). Focusing on the last part, it is important to find the right strategy within the current structure. As for measuring the matching of strategy and structure has caused issues, but it has been done by looking at the performance, good match causing a good performance and the other way around (Otley, 2016).

The theory stipulates that there are specific factors that will influence the relationship between dependent and independent variables of an organization's outcomes (Fiedler, 1967). This means that everything within an organization is affected by many different elements many of which cannot be accurately defined or measured. These internal and external elements will affect what type of control systems should be used by the organization to achieve the best possible performance (Kloot, 1997) and the final outcome of the organization should be used to determine if there is a good fit among the structure and the strategy used by the organization (Otley, 2016).

2.4 Upper Echelons Theory

With the same purpose as the contingency theory, the upper echelon theory attempts to explain why organizations act in the way that they do. It draws the link that a manager's background will in the end affect the outcomes of the organization (Hambrick & Mason, 1984). Hambrick & Mason (1984) argues that background characteristics like age, education and experience are considered to have an impact on the strategic choices made in various ways based and therefore

24 impact the performance of an organization. There are also psychological values that are more difficult to measure and observe like a person's values which affect the way we act and affect decision making (Hambrick & Mason, 1984). Therefore, Hambrick & Mason (1984) posits that the background characteristics serve as proxy measures psychological factors such as values, that influences the strategic direction and choices managers utilize (Olson, Parayitam & Twigg, 2006). Hambrick & Mason (1984) argues that strategic choices that are consistent with the environmental demands of the firm leads to positive outcomes. However, in this study the intention of selecting CEOs as part of the research lies not with the demographics or the psychological of the CEO, but rather that CEOs have a significant impact on the strategic corporate choices made within a firm which affects the organizational outcomes (Hambrick & Mason, 1984), which in turns affects the control systems and the internal processes used to obtain the desirable organizational performance in MCs.

2.5 Management Control systems

MCS have a long history as a topic of academic research, which has brought along multiple descriptions and definitions of what MCS is; some overlaps with others and others are very different (Malmi & Brown, 2008). David Otley provided his description of what an MCS is in 1999, he claimed that the MCS is a tool designed to provide useful information that facilitates managers in performing their jobs, and to assist the organization as a whole in developing, directing and sustaining desired employee behavior (Otley, 1999). This description by Otley (1999) is in line with the contingency-based research that regards the MCS as a passive tool designed to assist the decision making of the manager (Malmi & Brown, 2008). However, this view is not shared by Malmi & Brown, as they argue that MCS do not operate in isolation, and that organizations use large and complex combinations of MCS, therefore they studied MCS as a package (Malmi & Brown, 2008). The contingency-based perspective suggests that there is not a universally applicable system of MC in place, but that the choice of appropriate MCS will depend upon the specific organization and the circumstances surrounding it. A central contingent variable is the strategy and objectives that an organization decides to pursue, these objectives are very likely to heavily influence the choice of performance measures to be used (i.e. the desired outcomes) (Otley, 1999).

25 This study has adapted a blend of the perspective presented by Otley and Malmi & Brown by focusing on two management control systems which have been referred to as traditional public management control systems (TPMCS) and new public management control systems (NPMCS) by Uman et al. (2018). The NPMCS which concentrates on output control and performance is influenced by the NPM reforms highlighted by Hood in 1991. While the TPMCS has an emphasis on the inputs of the organization like planning and administrative control (Uman et al., 2018).

2.5.1 TPMCS

Planning is an essential part of input control, since the process of planning sets out goals and outcomes for the organization to work towards, thus affecting the decisions and actions that managers and employees make. The planning control is contingent on the idea that by setting consistent goals, organizations can attain these goals more effectively. Actions are often planned out over a set time period to determine how your progress compares to what was planned out in the beginning (Malmi & Brown, 2008). The use of set actions and goals is central for the TPMCS since it provides the CEO and the organization with clarity regarding the direction of the organization. Planning control contains and emphasizes both long- and short-term plans, short-short-term plans are represented by operational goals and long-short-term by strategic goals. Budgeting is central to, and the foundation of, MCS in most organizations and its use is almost universal. This is due to its ability to intertwine the goals, both short- and long-term, of the organization into a comprehensive plan which serves many different purposes (Malmi & Brown, 2008). As illustrated by Merchant and Van der Stede (2007) planning and budgeting often goes together but planning can include tasks that have little to no financial aspects, such as operational planning which produces task lists which are used by management to decide what employees do and how to do it (Malmi & Brown, 2008). The CEO may enforce the awareness of the previously set goals in order to ensure that the individuals in the organization know the expectations placed upon them (Uman et al., 2018).

The other major aspect of TPMCS is administrative control, which is a system that monitors and directs the behavior of the employees of an organization through the organizing of groups of said employees. The systems also entail who are made accountable for employee behavior (Malmi & Brown, 2008). Administrative control refers to control through lines of authority and

26 responsibility, and among other things, organizational structure. As argued by Malmi & Brown there are three different aspects of structure: policies and procedures, organization structure and governance structure (Malmi and Brown, 2008). Policies and procedures include what Merchant and Van der Stede (2007) call action controls, which includes pre-action reviews and action accountability, it is used to specify how decisions within an organization should be made. Organizational structure is the arrangement of individuals and functionality between departments, as argued by Flamholtz (1983) it contributes to the control by increasing the predictability of the employees. Lastly the governance structure is composed of the board structure and different management groups, the scheduled meetings creating expectations and deadlines to live up to.

2.5.1.1 TPMCS role in the relation between CEO MD and

Organizational Performance

With high emphasis on planning, a manager's ability to make quick instant moves is limited as their actions are planned out and even if they feel like there is a better move available they cannot commit to it, or at least not to the fullest. This could impact the actions available to the CEO and the implementation of decisions as they have goals to fulfill and decisions that would hinder the ability to reach short term goals would not be implemented even though in the long run it might be the best option available.

Having a strong administrative control would yield clarity of command and clear procedures for employees how to perform their tasks, leaving the leadership to focus on leading the organization. Which may be perceived as beneficial for CEOs with a low perceived level of MD, as the strong administrative control hinders the CEOs MD, However, administrative control is inherently top-down, and may therefore be perceived as bureaucratic and narrow. This perception may yield an opposite effect of what the TPMCS intends to achieve, i.e. demotivating employees in their commitment and their effort to ensure that the goals of the organization are being met (Uman et al., 2018). Using the perspective of the TPMCS, we hypothesize the following relationship:

Hypothesis 2:

Increasing the use of TPMCS has a negative moderating effect on the relationship between perceived managerial discretion and performance

27

2.5.2 NPMCS

NPMCS which have an emphasis on output control and performance usually include two forms of control: performance and reward control. Performance control is usually exercised through financial and/or non-financial measurements as indicators of employee performance and budgets (Uman et al., 2018). In the context of NPMCS the budget is the foundation for performance planning and evaluation of actual performance compared to what has been planned (Malmi & Brown, 2008). The process of evaluation and feedback with the use of budgeting as a foundation gives managers of different organizational levels concrete information to act upon and modify the input so that the desired output is reached. Which is in their best interest, since they have responsibility and accountability for the performance of their employees and their ability to adhere to the budget, while the utmost accountability lies with the CEO. Performance control is among the most extensively used types of control in private and public-sector organizations (Malmi and Brown, 2008) and by setting goals that are performance oriented and systematically following up on them gives the staff freedom to decide on their own which method is best how to achieve these goals (Uman et al., 2018), which is in line with the NPM and in contrast to the TPMCS which perceives to leave little discretion to the mid-level managers and employees.

Reward control has its foundation in the idea that the presence of rewards will lead to increased effort and motivation from the employees to attain the goals of the organization (Malmi & Brown, 2008). And thus, reward control systems focus on achieving congruence between the goals of the employees and the organization and establishing various rewards for attaining the organizational goals (Uman et al., 2018) and by effect enhancing the productivity and efficiency of the organization. Reward systems are extrinsic or intrinsic in nature: extrinsic reward systems are usually the ones that come to mind since they are represented by monetary incentives; intrinsic reward systems are represented by non-monetary incentives, such as professional development opportunities (Malmi and Brown, 2008). Reward systems, especially the extrinsic ones because of the monetary nature, can be associated with increased competition between employees and/or different organizational units. This increase of the use of reward controls in public organizations might be problematic since some indications posit it may create competition that is detrimental to the corporation because of the competition being destructive (Uman et al., 2018). However, a study made by Kim (2010) of public-sector reward controls found that when combined with clear objectives from management it results in the organization

28 showing performance improvement. Reward control is associated with a clear incentive scheme that is appreciated by employees, especially in the public sector (Uman et al., 2018).

In the context of public organizations, NPMCSs that incorporate the aspects of performance and especially reward control is a relatively new phenomenon. The introduction and implementation of the NPMCS was made with the intention to improve efficiency and reduce the complexity that usually have been associated with entities in the public sector. NPMCSs do this by setting performance-oriented goals and continuously following them up, while providing clarity about the associated rewards for achieving the desired outcome (Uman et al., 2018).

2.5.2.1 NPMCS role in the relation between CEO MD and

Organizational Performance

With the use of NPMCS within an organization you get a better understanding of the value of employees and departments with the increased emphasis on performance measurements. With a clearer understanding of the value that different departments bring you can easily see the development that a CEO brings that can be compared to his precursor. If the performance is increasing, more confidence should be put in the CEOs decisions and the process of achieving those results should not matter as much. If there are rewards on the line for the CEO and the employees, they will be more motivated to work towards the goal of the stakeholders and the CEO should in theory be given more space to achieve those goals as it is in everyone's best interests. When an organization sets out goals for the employees and regularly monitors them, it gives the employees more freedom in how to achieve those goals and the use of rewards can also help improve the implementation of changes as it motivates employees to work in a way encouraged by the manager. Using the perspective of the NPMCS, we hypothesize the following relationship:

Hypothesis 3:

Increasing the use of NPMCS has a positive moderating effect on the relationship between perceived managerial discretion and performance

29

2.6 Overview of theoretical model

30

3. Method

This chapter will start with presenting the research approach, followed by the choice of method to conduct the research. The chapter also presents the research strategy, data collection, analysis of non-response bias and sample selection. Operationalization of the variables follows thereafter. The data analysis paragraph explains how the collected data will be analyzed. Lastly, the validity and the reliability of the data and the ethical

considerations will be presented.

3.1 Research Approach

The research model used for this thesis is based on pre-existing literature. It tests the relationship between different variables based on prior knowledge which is known as a deductive research approach (Bryman & Bell, 2011). This approach tests a known theory with the use of different hypotheses based on prior knowledge in a different environment and circumstances to see if the theory is still valid (Bryman & Bell, 2011). A deductive research approach is used as the concept of managerial discretion has not been used much in the context of municipal corporations and therefore the use of a deductive approach aims to explore the relationship between managerial discretion and the performance of municipal corporations. A deductive research approach also allows the researchers to test theories through the use of hypotheses that in return leads to more standardized and objective outcomes of the results (Bryman & Bell, 2011). The hypotheses are also often associated with measuring concepts through a quantitative research which is also the method used in this thesis. Given the time limit of our thesis a deductive research fits better given the nature of the approach compared to an inductive approach which requires more time to observe (Bryman & Bell, 2011)

3.2 Research Method

The purpose of this study is to examine how managerial discretion impacts the performance of municipal corporations and what effect traditional and new public control systems might have on that relationship. To test this, we developed and tested different hypotheses with the use of a quantitative method as is often used in with a deductive research approach (Bryman & Bell, 2011). Our quantitative study is a cross-sectional study based on partly a survey sent to the CEOs of municipal corporations within the energy, water and waste management sector and content from reports produced by the MCs. A quantitative research method gives us access to

31 a larger amount of data that can be easily gathered and furthermore presents a more holistic view of the population which increases the generalizability of the results (Saunders, Lewis & Thornhill ,2009). With a quantitative method there is a limitation in the possibility of getting a greater understanding of the subject but at the same time it decreases the possibilities of different interpretation of the same results compared to a qualitative study (Bryman & Bell, 2011).

3.3 Research Strategy

When developing the research strategy, it is important to consider the purpose of the study and research question, which for this study is to examine how managerial discretion impacts the organizational performance of municipal corporations. With that purpose in mind you begin to examine how that could be explored. Saunders et al. (2009) described different research strategies that can be used for an explanatory purpose. The different strategies are ethnography, archival research, action research, experimental study, grounded theory, case study, and survey study. With a survey the researchers are able to gather all the information that they deem to be relevant and useful (Bryman & Bell, 2011). The strengths of using surveys as the method of data collection is the access to a large sample size and therefore creates the possibility to generalize the results to the population (given no non-response bias). Considering the large sample size, it covers, the time and effort to gather the data is small compared to other methods (e.g. archival research or interviews) and the response will be instant (Bryman & Bell, 2011).

One of the most serious criticisms of survey research is that the questions asked are often so complex that the survey ceases to be the most appropriate method of data collection as additional information may be needed from the person answering to give an accurate answer (Chua, 1996). Another difficulty when using surveys is getting a satisfactory response rate from the population, in order to increase our chances of achieving a good response rate we used the Dillman method (1978) of sending two reminders to the recipients a week apart and also increasing our total population by using three different industries, instead of one which was the original plan.

32

3.4 Data collection

This research consists of both primary and secondary data to further explore this research purpose. Primary data has been collected using quantitative data through an online questionnaire. It is primary data because it has not been used for research purposes or published in any other manner before and is collected by the researchers themselves (Bryman & Bell, 2011). The survey included four demographic questions about the CEO, measurements of managerial discretion and control systems within the organization as well as their perceptions regarding the organizational performance of their firm. The survey in its entirety can be found in Appendix 1. In total the questionnaire which contained 30 statements, and all of them were measured on the seven-point Likert scale (1=lowest value, 7=highest value). The survey was sent to a total of 164 CEOs, of which 63 answers were received, which resulted in a response rate of 38,4%. However, one received answer had to be omitted since no financial data was available at the time of conducting the research.

Secondary data was collected from official reports like financial reports and separate sustainability reports produced by the organizations. To assist in the collection of the publicly available financial reports the database Business Retriever was used to gather the MCs’ financial data. The term secondary data is named that since the information is collected by someone other than the user of the data, usually secondary data is readily available to the public but that is not always the case (Bryman & Bell, 2011).

3.5 Sample Selection

This study will be performed on Swedish municipal corporations in the utility industry. Previous studies regarding hybrid organizations such as MCs usually focuses on the public housing sector. This study is meant to expand the available literature on MCs and corporate governance into different sectors within the utility industry, since the services provided by the MCs are essential for society to properly function. Additionally, there is a special legislature for certain industries that provides vital services for society, such as the Water Act and the Electricity Act that stipulate that MCs should be run in a businesslike manner (Vattenlag, 1983:291; Ellagen, 1997:857). These laws may affect the CEO has on the performance of the firm. The selection of companies was done by visiting the municipalities websites and looking for their MCs, all energy, water and waste corporations that the municipalities owned 50% or

33 more were included in the population. Reason for the 50% cut off is that the municipality needs to have control over the organization and ability to govern its usage and they are only affected by for example the municipality act, if the municipality owns the majority. The choice of these industries is that they are important and have a similar role in the society of providing crucial services and these services often overlap, meaning that one organization often works within multiple of the industries. Next, the website was searched for the name and email address of the CEO and later used with an online survey tool to send the survey and keep track of non-respondents.

3.6 Analysis of non-response bias

Non-response bias can occur when subjects who refuse to take part in a study, or who drop out before the study can be completed, are systematically different from those who participate (Wright, Stern, & Phelan, 2012). Meaning that the results extracted from the statistical testing of the sample can become non-representative,because the participants may disproportionately be associated with traits that may affect the outcome. When response rates drop below 70%, the non-response rate becomes a critical issue (Wright et al., 2012). However, non-response bias may still occur even at a 70% response rate (Wright et al., 2012). The response rate of the survey sent out to the CEOs is 39%, which is far below Wright et al.’s limit for non-response rate and risk for bias being a critical issue. Therefore, an analysis of the non-response bias was made, to test if it occurred in the collected sample. According to Wright et al. (2012), the probability of non-response bias having materialized in the data set can be assessed by a comparison of the characteristics of participants and non-participants (see table 1).

Additionally, to test if a non-response bias had occurred in the collected data set, an independent sample t-test was run on the firm size and the gender of the respondents and the non-respondents. The results from the t-test shows that there is no significant difference between the two tested groups, and therefore, there is no occurrence of non-response bias within the collected data set.

Additionally, a comparison is made, in line with Wrights (2012) recommendations, in the following table between the respondents and the non-respondents. Since there is no significant difference between the two, the probability of non-response bias occurring is deemed to be low. Which affirms the results extracted from the t-test.

34 Table 1 Analysis of non-response bias

3.7 Operationalization

3.7.1 Dependent variable - organizational performance

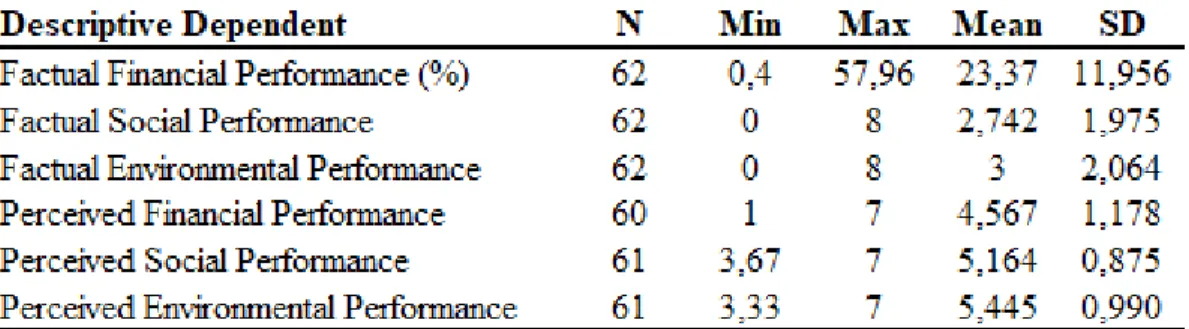

The measurement of performance was done in two ways, first a perceived performance from the view of the CEO of the firm. The other is objective measurements drawn from the financial reports produced by the organizations covering all three areas included within the TBL which is motivated by the multifaceted outcomes that municipal corporations strive to achieve.

3.7.1.1 Perceived organizational performance

CEOs who responded to the survey are asked to judge their own performance from a financial, social and environmental view. They are asked to judge their performance compared to similar companies and judge based on a seven-point scale of their compared performance, where a higher score represents better performance compared to similar companies.

The CEOs perceived financial performance (PFP) was judged on three different elements derived from Carmeli (2008) were they are asked to judge their performance compared to similar companies on a scale of 1 to 7. The following areas were examined:

Statement 1. Sale growth Statement 2. Return on sales Statement 3. Return on assets