J

Ö N K Ö P I N GI

N T E R N A T I O N A LB

U S I N E S SS

C H O O L JÖNKÖPING UNIVERSITYC S R C o m m u n i c a t i o n & S M E s

Master Thesis within Entrepreneurship, Management & Marketing Author: Malin Eliasson

Senida Smajovic Tutor: Anna Blombäck Jönköping June 2009

Acknowledgements

The authors of this thesis would like to thank our tutor Anna Blombäck for her ad-vice and guidance during the process of writing this thesis. This thesis would not have been possible without you and your involvement. We would also like to thank our fellow students for their interest and feedback during all seminar sessions.

A big thanks to all the respondents from Smålandsbygg and Sköna Hem AB, who took the time from their busy schedules in order to answer our questions.

Malin Eliasson Senida Smajovic

Jönköping International Business School

Abstract

Purpose: The purpose of this thesis is to investigate how SMEs in the Småland region define and communicate their CSR activities towards their stakeholders.

Background: Corporate social responsbility is a topic that is widely discussed today. In many cases the CSR agenda has been adopted by many large corporations. However there is a demand from governmental bodies to spread this agenda further to include and engage small-to-medium enterprises (SMEs). The main reason for this approach is due to SMEs being the most frequent type of business in Europe and is often influential in the local communities (Castka, Balzarova, Bamber, Sharp, 2004).

There is also a demand from stakeholders to receive information about CSR. Research within the field of CSR Communication has mostly been focused on large corporations. Recently, the focus has shifted towards SMEs and it is still an emerging field. The research concerning CSR and CSR communication within the SME context is limited and therefore it is an important area that needs to be addressed.

Method: The purpose of this thesis was achieved by using the case study ap-proach. Two companies; Smålandsbygg and Sköna Hem AB were in-vestigated. Four respondents from each company were interviewed and the outcome of the interviews was analyzed together with the frame of reference.

Conclusions: According to the findings it is difficult to provide one common definition of CSR that can be applied for the two companies in the study. In general it might be difficult to provide a common definition of CSR in SMEs. According to previous research the way SMEs conduct their business is dependent on the owner and the personalities of the management. Consequently, there can be a variety of ways that SMEs are engaging in CSR or percieve CSR to be.

There are three different communication strategies when communi-cating CSR towards the stakeholders. It could be interpreted that both companies applied different communication strategies depending on which stakeholder they were communicating with.

Sammanfattning

Syfte:

Syftet med den här uppsatsen är att undersöka hur små och medelsto-ra företag definiemedelsto-rar och kommunicemedelsto-rar demedelsto-ras CSR aktiviteter gent-emot sina intressenter.

Bakgrund: Företagets sociala ansvarstagande, även kallat CSR, är ett omdiskute-rat ämne idag. I många fall har CSR agendan integreomdiskute-rats i de flesta stora företag. Emellertid finns det ett krav från statliga organ att spri-da denna agenspri-da vispri-dare och engagera små och medelstora företag. Den främsta anledningen för denna ansats beror på att små och me-delstora företag är den mest vanligt förekommande verksamheten i Europa och tenderar att vara inflytelserika i lokalsamhället. (Castka, Balzarova, Bamber, Sharp, 2004).

Det finns också efterfrågan från olika intressenter att få information om CSR. Forskning inom området CSR kommunikation har mest va-rit riktad mot större företag. Nyligen, har fokus skiftat till små och medelstora företag och är fortfarande ett område på frammarsch. Forskning inom CSR och CSR kommunikation i små och medelstora företag är begränsat och är ett viktigt område som måste uppmärk-sammas.

Metod: Syftet med den här uppsatsen uppnåddes genom att använda en fall-studie. Två företag; Smålandsbygg och Sköna Hem AB undersöktes. Fyra personer från varje företag blev intervjuade och resultatet från dessa intervjuer analyserades tillsammans med referensramen.

Slutsats: Enligt resultaten från studien är det svårt att tillhandahålla en allmän definition när det gäller CSR som kan appliceras i de två företag som var med i studien. Generellt sett kan det vara svårt att ge en allmän definition om CSR i små och medelstora företag överhuvudtaget. Ti-digare forskning visar att sättet som små och medelstora företag drivs på, påverkas av ägarna och ledningens personlighet. Följaktligen kan det finnas flera olika variationer om hur små och medelstora företag är engagerade i CSR eller hur de uppfattar CSR konceptet.

Det finns tre olika kommunikationsstrategier när man vill kommuni-cera CSR till olika intressenter. De två företagen i studien applikommuni-cerade olika kommunikationsstrategier beroende på vilken intressent de kommunicerade med.

Table of Contents

1

Introduction ... 1

1.1 Background ... 1 1.2 Problem discussion ... 2 1.3 Purpose ... 3 1.4 Disposition ... 32

Frame of reference ... 4

2.1 Previous research within the field of CSR and SMEs ... 4

2.2 Definition of CSR ... 6

2.2.1 Economic domain ... 7

2.2.2 Legal domain ... 8

2.2.3 Ethical domain ... 8

2.2.4 Other perspectives on CSR ... 8

2.2.5 Corporate Social Responsibility stances ... 9

2.3 Corporate Communication ... 11

2.3.1 Management Communication ... 11

2.3.2 Marketing Communication ... 11

2.3.3 Organizational Communication ... 12

2.4 Stakeholder theory and Communication ... 12

2.5 Strategic CSR communication ... 14

2.5.1 Stakeholder Communication Strategies ... 14

3

Research Design and Method ... 17

3.1 Research approach ... 17

3.2 Literature Review... 17

3.3 Data Collection ... 18

3.4 Qualitative Data collection ... 18

3.5 Case study approach ... 19

3.6 Selection of cases ... 20

3.6.1 Presentation of Case Companies ... 21

3.7 Qualitative Interviews ... 22

3.8 How the empirical material from the interviews was derived ... 24

3.9 Trustworthiness ... 24

3.9.1 Limitations of case studies as a qualitative sampling method ... 24

3.9.2 Validity ... 24 3.9.3 Reliability ... 25 3.9.4 Generalizability ... 25

4

Empirical findings ... 26

5

Analysis ... 37

6

Conclusions ... 43

7

Discussion ... 44

References ... 45

Table of figures

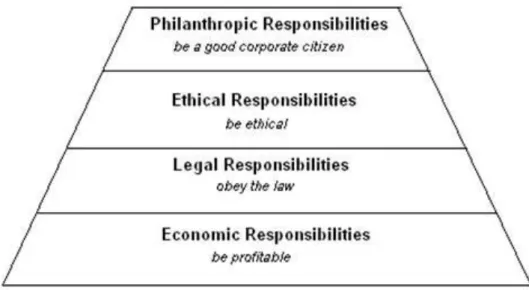

Figure 1 Carroll's Pyramid of CSR ... 6

Figure 2 The three-domain model of CSR ... 7

Figure 3 Three level Model of exchange and communication ... 12

Table 1 Corporate Social Responsibility Stances. ... 9

Table 2 Three CSR Communication Strategies ... 16

Table 3 Case Selection ... 21

1

Introduction

Companies have an important role in the development of society today because they offer products and services that are demanded by the public, while at the same time they gener-ate job opportunities. The companies‟ role in society has always been a subject of discus-sion, the opinions and ideas of what obligations and responsibilities a company should take on have changed over time (Grafström, Göthberg & Windell, 2008). During the 1990‟s companies like H&M, Nike and GAP were involved in scandals that were exposed by the media. The companies were criticized for using workers in low developed countries and for violating human rights (Jenkins, 2001). During the same time the anti globalization move-ment grew stronger around the world and a debate about companies‟ responsibility in the society was raised. This debate has spread over the world due to improved communica-tions and ability to share information worldwide (Grafström et al. 2008). Further the re-sponsibility of media has increased and today media has an important role in the society in terms of communicating information. This development has lead to companies being more scrutinized by the media than ever before. At the moment the world is experiencing a fi-nancial crisis that has gone out of proportion. This crisis is an additional example of how lack of ethical judgment in the business world hurts society, customers, employees, owners and other stakeholders (Borglund, De Geer & Hallvarsson, 2009).

The review of companies in the media is increasing as well as the demand from stakehold-ers to receive information and these factors are putting pressure on companies to meet these demands. The act of taking on an increased social and ethical responsibility is defined by the term „Corporate Social Responsibility‟, hereafter it will be referred to as CSR. The European Commission defines CSR as;

“A concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis.”

- European Commission (a)

So what are the reasons for companies to engage in CSR activities? Do they really have to care about taking on a social and ethical responsibility and who is benefitting from creased corporate social responsibility activities? Today companies are experiencing in-creased competition and customers have higher demands on both products and services as well as on the company itself. According to Löhman & Steinholtz, (2003), it is not enough anymore to have a „good‟ product; the companies have to deliver additional value in terms of emotional values. Customers feel a need to be able to identify him- or herself with what a company is representing. Companies have to be able to show customers and other stake-holders that they realize their important position in the community. Awareness of the envi-ronment and caring about employees are today important issues that companies need to address in order to stay competitive in the market.

1.1 Background

Investing in corporate social responsibility (CSR) is believed to create value for the compa-ny itself as well as for its stakeholders. In order to create this value one possible way is through the marketing of corporate responsibility (Van de Ven, 2008). Corporate commu-nication can be defined as strategic coordinated external and internal commucommu-nication with the goal to inform and build a relationship with the company‟s stakeholders. The concept

of corporate social responsibility is strongly linked to the stakeholder approach to commu-nication. (Nielsen & Thomsen, 2009). The work with corporate social responsibility activi-ties within an organization is in many ways connected to the corporate relationship with the stakeholders of the company and it is essential for the company to consider a CSR communication strategy that matches the need of interaction between the company and its stakeholders (Nielsen & Thomsen, 2009).

Much of the research performed on CSR communication has focused on how large com-panies communicates their CSR activities and CSR reporting (Holland & Gibbon 2001; Gao & Zhang 2001; Nielsen & Thomsen 2007; Burchell & Cook 2006). However, the fo-cus on CSR communication in small and medium sized firms (SMEs) has started to be-come seriously addressed recently and it is still an emerging field (Nielsen & Thomsen, 2009). The European Union defines SMEs as “ The category of micro, small and medium-sized enterprises (SMEs) is made up of enterprises which employ fewer than 250 persons and which have an annual turnover not exceeding 50 million euro, and/or an annual bal-ance sheet total not exceeding 43 million euro”(European Commission b). Spence and Lo-zano (2000) argue that it is more difficult for small firms to communicate about their busi-ness ethics due to scarce resources, informal communication within the company and lack of defined roles of the employees. This in combination with CSR being perceived as a „fuzzy‟ concept among many SME managers can create an obstacle when SMEs want to communicate or is already communicating their CSR activities.

1.2 Problem discussion

Murillo and Lozano (2006) argue that SMEs are confused with the concept of CSR and think it is problematic to relate the concept to their actual CSR activities that they carry out. If the SMEs are confused with the concept of CSR, one can make an assumption that SMEs also find it difficult to communicate their CSR activities. A recent study that was conducted among Danish SMEs concluded that many SMEs do not communicate their CSR activities frequently (Nielsen & Thomsen, 2009). This is also an indication that SMEs might find the issue of CSR communication difficult to manage. As mentioned previously the research concerning CSR and CSR communication within the SME context is limited and therefore it is an important area that needs to be addressed.

Since SMEs represent 99 % of all enterprises in the European Union, and together they provide around 65 million jobs, they are both socially and economically important (Euro-pean Commission, 2009 b). Nielsen and Thomsen (2009) argue that companies employing 100-250 employees are much more likely to externally communicate their CSR activities compared to smaller companies with fewer employees. This shows that SMEs are impor-tant to investigate when it comes to communicating CSR as they represent that many com-panies. Further, SMEs are more rooted in the society and therefore they may feel more pressure to act responsible as they are closer to their stakeholders (Spence, 2004, cited in Spence, 2007). Therefore, SMEs might also feel pressured to communicate their CSR activ-ities due to the close proximity of their stakeholders.

Previous research indicates that many SMEs perceive CSR to be a fuzzy concept and thus find it difficult to communicate their CSR activities externally. Consequently it can be in-terpreted that many SMEs struggle with their CSR communication. Some SMEs engage in CSR activities without knowing it, because they do not recognize these activities to be CSR. The authors of this thesis want to investigate how SMEs in the Småland region perceive CSR and how they communicate it externally. The reason for investigating SMEs in

Småland is because this region has long been known for its entrepreneurial spirit and many small and medium sized firms. In the region the “Gnosjö Spirit” is a familiar term which represents knowledge, quality and up-to-date industrial technology (Gnosjö Region, 2009). The authors hope to shed some light on how SMEs in the Småland region define CSR and how they communicate their CSR activities externally. It is also the authors‟ ambition that this research will be regarded as a contribution to the continuing research within the field of CSR and CSR communication within SMEs.

1.3 Purpose

The purpose of this thesis is to investigate how SMEs in the Småland region define and communicate their CSR activities towards their stakeholders.

1.4 Disposition

Below you can find the disposition of this thesis.

Chapter 5 Analysis Chapter 4 Empirical findings Chapter 3 Method Chapter 2 Frame of reference Chapter 6 Conclusions

The frame of reference contains theories that are neces-sary for this study. In this section the theories that are relevant for the purpose will be presented.

In the method chapter the authors will explain how they conducted the study, and provide the reader with a motivation for the chosen method. A closer description of the two companies and the respondents will be pre-sented.

The empirical findings of the conducted study will be presented in this section.

In this section the empirical findings will be analysed together with the theories from the frame or reference. The aim is to answer the purpose of this thesis.

Here, the conclusions from the analysis will be pre-sented.

2

Frame of reference

The frame of reference contains theories that are necessary for this study. In this section the theories that are relevant for the purpose will be presented.

2.1 Previous research within the field of CSR and SMEs

In this section a short summary will be presented of previous research within the field of CSR and SMEs. The main reason for including this section is to give the reader an over-view of CSR and to show how difficult it can be to manage, especially for SMEs. The first section will present an overview of the main findings concerning CSR and SMEs. The second section will present some findings concerning CSR communication and SMEs. Many articles and books have been written about corporate social responsibility. In many cases the CSR agenda has been adopted by many large corporations. However there is a demand from governmental bodies to spread this agenda further to include and engage small-to-medium enterprises (SMEs). The main reason for this approach is due to SMEs being the most frequent type of business in Europe and is often influential in the local communities (Castka, Balzarova, Bamber, Sharp, 2004).

The term corporate social responsibility can be misleading and in many cases be related to multinational corporations and issues concerning the environment and human rights. The Australian Corporate Social Responsibility Standard state that the term „corporate‟ should not be taken literally and instead should be seen as a broad definition. The CSR theory is broad and can be integrated in all types of organizations, reaching from multinational en-terprises to SMEs. Much of the research that has been conducted argues that CSR is bene-ficial for the organization and therefore SMEs should engage in CSR activities because of the important role that they possess in a local community. Jenkins (2006) on the other hand argues that most CSR approaches are more focused on how large corporations have dealt with these issues and therefore CSR theories are developed for large corporations. Accord-ing to Jenkins (2006) there is an assumption that SMEs are in fact „little big companies‟ meaning that they operate and behave as large corporations. Consequently, they can take the CSR approach and adjust it to SMEs. This argument is however not true, SMEs do not behave or conduct their business the same way that large corporations do. The way that SMEs are run is dependent on the owner and the personalities of the management. SMEs do not have a formal management structure and the employees do not have specific areas that they work with. The manager is involved in many activities at once, and the interest of other tasks and issues that is not related to the day to day routines is probably not that high (Jenkins, 2006). There are no homogenous SMEs and when applying any CSR initiatives the diversity needs to be addressed. However, the main question is how SMEs perceive the CSR issue? (Castka et al, 2004).

According to Southwell (2004) there is evidence that the majority of SMEs consider organ-izations that are similar to theirs should be more aware of their social and environmental responsibilities (cited in Jenkins, 2006). Many SMEs perceive CSR to be a threat to their business and expensive due to the required resources needed for CSR to be efficient and effective. However, SMEs are starting to change their opinion concerning CSR and some enterprises see this approach as a competitive advantage (Jenkins, 2006). Madden, Scaife and Crissman (2006), present a study made on Australian SMEs which suggests that SMEs have a strong desire to contribute to local causes and to be seen as active in their local community (Madden et al. 2006).

SMEs who engage in CSR activities are not motivated by the same reasons as the large corporations. For SMEs issues that are closer to the company, such as employee motiva-tion, retention and community involvement is more important than brand management, transparency and accountability that mostly large enterprises are engaged in (Jenkins, 2006).

CSR Communication

Nielsen and Thomsen (2009) state most research that is conducted concerning CSR and CSR communication are focused on large corporations. The field of CSR communication is still emerging and needs to be addressed, especially within the SME context.

Today stakeholders are demanding more from the companies and the pressure on compa-nies to meet expectations from stakeholders and society is increasing (Cornelissen, 2004; Jenkins, 2004; Borglund, De Geer & Hallvarsson, 2009). One way for companies to satisfy the stakeholders‟ expectations is by communicating their CSR activities externally. The most common channels for CSR communication are social reports, thematic reports, codes of conduct, web sites, internal channels and cause related marketing (Birth, Ilia, Lurati & Zamparini, 2008).

Many companies invest large amount of money in policies, practices, management and re-porting systems to assure the public that the company is socially responsible. In general the public do not always respond very well to CSR communication and few companies have had successful responsibility programs. The public is often suspicious towards companies that engage in CSR activities because they question the company‟s motives for investing and engaging in these types of activities, especially if the company commits to being re-sponsible only to gain marketing advantage. Companies that want to be perceived as credi-ble need to support causes that fit with the company image and brand. Further, the organi-zations behavior has to be consistent with what they are communicating externally other-wise their corporate responsibility programs can be perceived as a marketing trick trying to cover the company‟s unethical behavior (Dawkins, 2004).

The communication of CSR is very complex as mentioned previously, however it is even more complex when businesses are small. In small firms there are limited amount of em-ployees and the proximity between the emem-ployees is not far, all these factors can enhance the communication and create trust among the employees. On the other hand, small firms lack the resources in order for them to implement a dialogue within the company, together with scarce resources and the lack of defined roles among the employees can create many problems when wanting to communicate about business ethics (Spence & Lozano, 2000). A recent study made among 1071 Danish SMEs showed that they are not communicating CSR to external stakeholders frequently. Only 36 percent of the enterprises communicated their CSR activities externally. Further 40 percent of these enterprises communicated CSR activities externally on a regular basis. Further, the results showed that the communication of CSR lacked a strategy and was in many cases improvised by the middle managers. The communication within the company and decision making was handled in an informal and personal manner. The authors also argue that this approach to communication does not take into account important issues such as stakeholders relations, corporate communication and reputation, which are important issues for SMEs to consider when doing business with organizations worldwide. The CSR engagement in SMEs is affected by the manager‟s per-sonal views concerning ethical concern and commitment. The study concluded that most

SME managers put more emphasis on internal communication than external communica-tion (Nielsen & Thomsen, 2009).

2.2 Definition of CSR

The corporate social responsibility section will first be introduced by Carroll‟s definition of CSR, since he is amongst the famous researchers within the field of CSR. The authors also included the three-domain model of CSR as it is a new concept that was developed from Carroll‟s pyramid of CSR. These two models will help the authors answer the purpose and define how, the two companies that are investigated in the thesis, define their CSR. These two models will also be used as a base when creating the questions for the qualitative inter-view.

The corporate social responsibility stances theory is also included in this section as it will facilitate for the authors to understand how the two companies deal with the CSR issues. The corporate social responsibility stances theory will also be incorporated in the analysis. There has been a discussion during several decades about the relationship between business and society. Even though many have tried to define CSR, the concept is still unclear and ambiguous. When trying to defining CSR there are two schools of thought, one focuses on the business aspect meaning the business is only required to maximize their profit within the limitations of law and ethical constraints. While the other viewpoints suggest that the business should increase their responsibility towards the society. Archie Carroll tried to overcome these separate point of views by proposing a new definition of corporate social responsibility; “The social responsibility of business encompasses the economic, legal, ethical, and discre-tionary expectations that society has an organizations at a given point in time” (cited in Schwartz & Carroll, 2003 p. 503). Carroll later integrated his four-part categorization of CSR into a framework called the “Pyramid of Corporate Social Responsibility” (Schwartz & Carroll, 2003).

Even though Carroll‟s four-part model was highly valued, his use of a pyramid to demon-strate the framework was seen as confusing and not applicable to all situations. Some per-ceived the pyramid framework as a hierarchy, meaning that one responsibility was seen as more important than the other. Further, the pyramid framework does not consider over-lapping of the CSR domains, a weakness of the framework recognized by Carroll. All these factors lead to a new concept called the three-domain model of CSR. The model consists of three responsibility areas namely; economic, legal and ethical. The three responsibility areas are consistent with Carroll‟s four-part model and are overlapping (Schwartz & Car-roll, 2003).

Figure 2 The three-domain model of CSR. Source: Schwartz and Carroll, (2003)

2.2.1 Economic domain

The economic domain contains all activities which have either a positive indirect of direct effect on the economic situation in a corporation. The positive economic effect in a corpo-ration consists of two criteria‟s, the maximization of profits and maximization of share value. Actions such as the intention to increase sales or avoidance of lawsuits are examples of direct economic activities. Indirect activities are actions taken from the corporation in order to improve the company‟s image or motivate the employees. According to Schwartz and Carroll, any measures taken from the corporation with the intention to improve profits or share value are economically motivated. Most corporate activities will have a positive ef-fect on the economic situation; however there are some activities that are excluded from the economic domain. When a corporation chooses an activity that will not generate any profit over an activity that is more profitable, or when a corporation is involved in a project without considering the financial outcome of this involvement, these types of activities are not included under the economic domain (Schwartz & Carroll, 2003).

2.2.2 Legal domain

The legal domain refers to how responsible a firm is to legal expectations that is created by the society in terms of federal, state and local jurisdiction. There are three categories of le-gality; compliance, avoidance of civil litigation and anticipation of law. The compliance category imply that the company does what it can in order to follow laws, some companies do it intentionally and some by haphazardness. Avoidance implies that a company is moti-vated to follow the law in order to avert possible or future legislations. The third category, anticipation of law, entails that the company change their activities in order to comply with forthcoming laws (Schwartz & Carroll, 2003).

2.2.3 Ethical domain

The ethical domain refers to the ethical behavior of a corporation that is demanded by the society and the stakeholders. The ethical domain consist of three general ethical standards; conventional, consequential and deontological. Convetional standard means that there have been a set of rules or norms where for instance the society, the organization or industry have accepted these norms of how a business should be operated. Consequential standard promotes the idea that includes both egoism and utilitarianism. According to this view an action that is taken and that provides good both for the individual and society while at the same time it produces the greatest net benefit can be considered to be ethical. Deontologi-cal standard implies that one should engage in activities that reflect on the company‟s own duty or obligation (Schwartz & Carroll, 2003).

2.2.4 Other perspectives on CSR

CSR is a concept that has been widely discussed among many authors. There are two schools of thoughts when approaching the term CSR, some authors argue that the primary goal for a company is to maximize the profit while others believe that a company should go beyond and above what is legally required and behave ethically.

Milton Friedman has a traditional view about business, and how it should be conducted. Friedman explains that business managers represent the shareholders and are accountable for engaging in activities that benefit the company. The main task for the business manag-ers is to maximize the firm value. Further, business managmanag-ers should not engage in CSR ac-tivities when they do not generate any profit for the company. Friedman also states that business managers should not refrain from investing in profitable projects that have ful-filled all legal requirements but do not comply with the beliefs of the business manager (Pava & Krausz, 1996). Friedman is of the opinion that engaging in CSR can be harmful for the company since the manager will spend time and resources on CSR activities instead of running the business as efficiently as possible. However, Margolis and Walsh conducted a study where 127 published empirical studies were examined between 1972 and 2002, which dealt with the issue concerning socially responsible behavior and companies‟ finan-cial results. The study indicated that there was a positive relationship between these two factors (cited in Blowfield & Frynas, 2005). Consequently the findings from Margolis and Walsh are contradictory to Friedman‟s perception of CSR and business, companies can be ethical and engage in CSR activities and still be profitable.

Steve Wadell (2000) argues that when it comes to planning and implementing the CSR agenda within firms, in general these efforts are quite poor or inadequate. The main reason for this is due to lack of monitoring these CSR efforts and that the state is not involved. As

a result initiatives such as codes of conduct loses its function, they are not precise and are not consistent throughout the company. However, CSR can reform and become a useful tool by improving for instance the codes of conduct or engaging in partnerships (cited in Blowfield & Frynas, 2005).

2.2.5 Corporate Social Responsibility stances

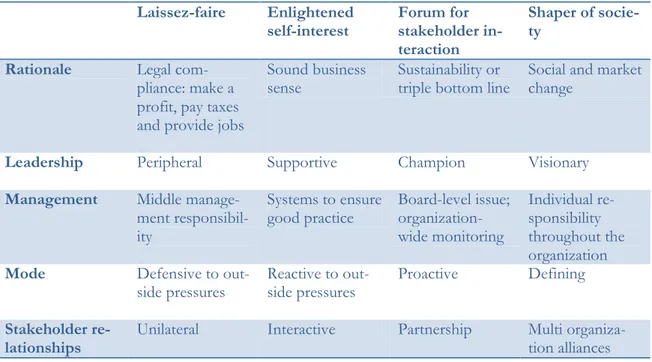

Table 1 Corporate Social Responsibility Stances. Source: Johnson, Scholes & Whittington, 2008, p 146

Many organizations have different approaches concerning corporate social responsibility. The stances illustrate four stereotypes of how organizations can deal with CSR issues. With the help of the framework corporate social responsibility stances (Table 1) the CSR activi-ties of the two investigated companies in the study can be identified. This framework would facilitate the analysis of how the two SMEs in the study work with and perceive CSR.

The Laissez-faire view entails the organizations only obligation is to make a profit, pay tax-es and create job opportunititax-es. The government creattax-es laws and regulations and the or-ganization will obey these set of laws but will not do more than it is required of them. If it is expected of the organization to practice social duties that are beyond this, in worst cases can damage the authority of the government. This stance is exercised by executives that be-lieve in this ideology or by smaller businesses that do not have resources to take on more responsibilities than to comply with the required regulations and laws. This view sees social good is practiced when the company improves their profitability. According to the laissez-faire view, a company would do well if social obligations were a necessity when wanting to obtain contracts or to protect the company brand. The responsibility for these types of ac-tivities would depend on the middle managers instead with the chief executive. The rela-tionship between the organization and its stakeholders would be unilateral and not interac-tive. The downfall with this view is the public perception; they would not want a company to behave in this manner. Many executives are aware of the stakeholder expectations on how an organization should act, and understand that a company needs to take on a more proactive role (Johnson et al. 2008).

Laissez-faire Enlightened

self-interest Forum for stakeholder in-teraction

Shaper of socie-ty

Rationale Legal com-pliance: make a profit, pay taxes and provide jobs

Sound business

sense Sustainability or triple bottom line Social and market change

Leadership Peripheral Supportive Champion Visionary

Management Middle manage-ment responsibil-ity

Systems to ensure

good practice Board-level issue; organization-

wide monitoring

Individual re-sponsibility throughout the organization

Mode Defensive to

out-side pressures Reactive to out-side pressures Proactive Defining

Stakeholder

The enlightened self-interest view recognizes that the long term financial benefit to the shareholders and good relationship with other stakeholders are very important. This view sees corporate social responsibility to be a sound business sense. The reputation of a com-pany is very important and can provide a long-term financial success, but the reputation must be handled with care, that is why taking on a more proactive approach to social re-sponsibility is perceived to be a good investment. Further, a good reputation could for ex-ample, attract new staff members or help to retain them (Johnson et al. 2008).

The enlightened self-interest view would require that managers have to take on a responsi-bility not only to the organizations shareholders but also to the stakeholders. Therefore, a more interactive approach would be necessary when communicating with the stakeholders. Further, some managers would implement systems or policies such as certifications, ISO 14000, prevent child labor etc. The organization would monitor their corporate behavior and make sure that corporate social responsibility activities would be integrated and im-plemented in the company (Johnson et al. 2008).

Forum for stakeholder interaction stance takes in multiple stakeholders‟ interest and expec-tation into consideration when the organization creates its strategy and purpose, as op-posed to the shareholders being the only ones to influence this process. This stance be-lieves the organization‟s performance can be measured in more ways than one. The organi-zation can keep uneconomic units in order to retain staff, not produce goods that are „anti-social‟ and are willing to decrease the profitability for the social good (Johnson et al. 2008). When having to consider many expectations and opinions from different stakeholder it can affect the company in a negative way because they have to balance between different inter-ests constantly. Consequently, it takes longer for the organization to create or develop new strategies. Different CSR activities are elevated to the board-room, where these issues are discussed and monitored across its global operations (Johnson et al. 2008).

Shapers of society want to change the norms in the society and therefore see the financial aspect as secondary when conducting business. Some businesses were founded only for the reason to give back to the society. Therefore, these types of organizations often have part-ners or collaborating with other organizations to fulfill their purpose. For a company to be able to take this stance, need to be privately owned and not be liable to different stakehold-ers (Johnson et al. 2008).

2.3 Corporate Communication

The communication section of the frame of reference will be introduced with overview of corporate communication, as it is a base for other communication theories. The section will also include stakeholder theory and communication. Within CSR, stakeholders are very important and therefore the authors chose to include the stakeholder theory and communi-cation model. This model will used as a base when creating questions for the qualitative in-terview and will also be used in the analysis when analyzing the empirical findings. The last theory of this section is the strategic CSR communication model; this model will also be used as a base when creating the questions for the qualitative interview and will also be used to answer the purpose of this thesis.

According to Van Riel (1995) there are three main forms of corporate communication; marketing communication, organizational communication and management communica-tion. Management communication is perceived to be the most important form of commu-nication. It is here where the communication between the managers and the stakeholders occur. The term marketing communication is used to cover areas such as advertising, sales promotion, direct mail, sponsorship etc. Organizational communication includes areas such as public relations, investor relations, labor market communication and environmental communication (Van Riel, 1995).

2.3.1 Management Communication

The management holds key function within the organization. The term management entail the work that is accomplished in the company is depended on individuals within that com-pany. Common managerial task are planning, organizing, commanding, coordinating and controlling. The management can only function if the employees want to be managed. Therefore, communication is a vital part when wanting to persuade the employees to comply with the goals of the organization. The responsibility of communication is ex-tended within the entire company. Senior, middle and junior management use communica-tion to fulfill results such as:

Creating a common vision of the corporation within the firm

Create and maintain trust in the top management within the corporation Authorize and motivate the staff

The management and CEO of the company must be able to communicate the company image and vision externally to the stakeholders when needed (Van Riel, 1995).

2.3.2 Marketing Communication

Marketing communication is made up of communication that strengthens the sale of prod-ucts or goods. Most authors within this field argue that advertising is the most important element in the marketing communications mix. Rossiter and Percy (cited in Van Riel, 1995) see advertising as a form of persuasion from the company in order to create a positive im-age and the purchase of a product. According to Jenkins (cited in Van Riel, 1995) sales promotion are a set of activities where the goal is to support sale representatives and the distributors. Other forms of communication that is used in the marketing field are; spon-sorship, direct mail and personal selling (Van Riel, 1995).

2.3.3 Organizational Communication

All forms of organizational communication are focused on reaching different target groups. These target groups are groups that the company shares a relationship with, usually an indi-rect relationship. The main difference between organizational communication and market-ing communication is the way the communication is used to influence the target group. Organizational communication is more an indirect approach when attempting to influence the target groups that the organization depends on. Some examples of different target groups are public authorities, civil servants or financial journalists (Van Riel, 1995).

Organizational communication is embedded within the entire company and does not be-long to a department or function. Consequently, organizational communication can be de-scribed as “all forms of communication used by the organization, other than marketing” (Van Riel, 1995, pp 12).

2.4 Stakeholder theory and Communication

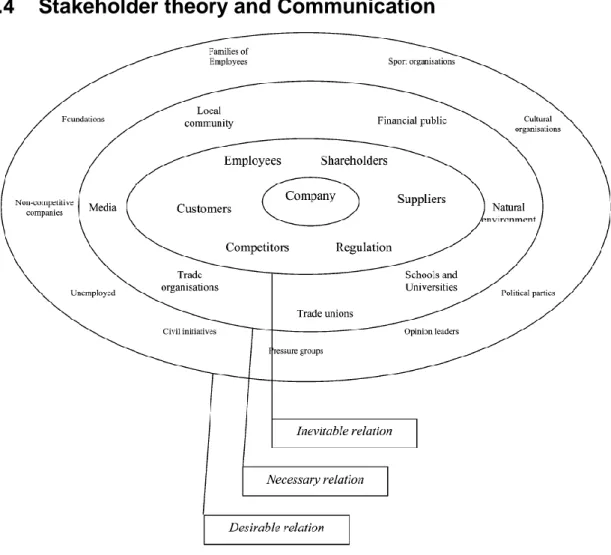

Figure 3 Three level Model of exchange and communication. Source: Podnar and Jancic, (2006)

In the stakeholder theory it is implied that the company consists of interaction with its stakeholders. According to the stakeholder theory, companies are part of a social system and therefore are involved in exchange episodes with various social subjects. Companies are bound to a “new social contract” which refers to obligations and responsibilities of

each involved company in the social environment. Besides economic and legal issues, the contract requires that companies are accountable for their actions and expect them to per-form ethically. As a result, the company‟s management has to deal with different stakehold-er issues. The stakeholdstakehold-er theory also involves communication with diffstakehold-erent stakeholdstakehold-ers. It is vital for the company to identify their stakeholders and to investigate the apprehen-sions and interest they feel towards the company (Podnar & Jancic, 2006).

Many authors advocate that the companies should consider the different stakeholder groups when formulating a communication plan. Most common stakeholder groups are; employees, consumers, shareholders, business partners, the government, competitors, the media etcetera. Several attempts have been made to create appropriate criterions in order to categorize different stakeholders (Podnar & Jancic, 2006).

Jancic (1996) presented the idea that not all stakeholders are vital for the company and its communication. According to Jancic, there are three main levels of exchange and commu-nication with different stakeholders. The three levels of exchange consists of; inevitable-, necessary-, and desirable communication. Inevitable communication refers to the most im-portant stakeholders that a company has. These groups are the primary stakeholders for the company and the relationship is very important. “The second level presents stakeholders with whom exchange is necessary, and the final level represents those stakeholders with whom communication is desirable” (cited in Podnar & Jancic, 2006, p 300).

According to the framework different levels of exchange, it is very important for the com-pany to customize the communication to different stakeholders in order to develop and maintain good relationship with the different groups. Depending on how strong the rela-tionship is between the company and the key stakeholders, it will have an impact on the ef-fectiveness of the marketing communication strategy.

Another theory that advocates a close communication between a company and its stake-holders it the framework „Strategic CSR communication‟ and can be found in the next sec-tion. In this model Morsing and Schultz (2006) have identified three types of communica-tion strategies that can occur between the company and their stakeholders. These two theo-ries relate to each other as both the communication and stakeholders are a central part of the model. Further, both theories argue that a close communication between a company and its stakeholders is important and beneficial for both of them. A company should strive to have a dialogue with its stakeholders.

2.5 Strategic CSR communication

When it comes to communication of CSR within a company, it is crucial to consider the stakeholders as the communication of CSR is most likely to concern the dialogue between the company and its stakeholders (Morsing & Beckmann, 2006). Participation, involvement and dialogue are significant regarding the stakeholder theory. By using dialogue as the tool, agreement and compromises can be seen as the keys on which to base further decisions and plans for actions. This provides for the continuation of the collaboration between the company and its stakeholders. Due to the fact that stakeholder‟s expectations concerning CSR are increasing, companies need to take this into account on a continuous basis (Mors-ing & Schultz, 2006).

2.5.1 Stakeholder Communication Strategies

Morsing and Schultz, (2006), have identified three possible types of relations between a company and its stakeholders in terms the communication of CSR, the authors have based these types of relations on Grunig and Hunt‟s (1984) categorization of models of public re-lations. Grunig and Hunt (1984) argued in the public relations theory that only 35 % of all companies practiced two-way communication processes whereas 50 % practiced one-way communication and this was done in terms of public information to their stakeholders (cited in Morsing & Beckmann, 2006). Morsing & Schultz (2006) argue that there is an in-creasing need to develop more sophisticated two-way communication processes when companies are to communicate their CSR activities, while some argue that the frequency of public information, which is commonly a one-way communication process, is also a true picture of today‟s process of corporate communication. It is not sufficient for a company to only rely on one-way communication of CSR activities, although it is indeed necessary, when it comes to building and maintaining legitimacy (Morsing & Schultz, 2006).

1. Stakeholder information strategy

In this strategy the information flow is handled one-way. That is, the flow of information goes from the company to its stakeholders. This one-way communication approach pro-vides no availability to interact between the two parties; rather the purpose of this commu-nication approach is for the company to simply inform the public about the organization. Different types of applying the stakeholder communication approach are for the company to participate in press relations programs along with providing the media with news and in-formation. Brochures, pamphlets and magazines are other examples of applying this com-munication strategy. In order to build and maintain positive support from its stakeholders, the top management believes that what they need to do is to efficiently inform the general public that they are doing „the right thing‟. In this way, ensuring that positive corporate CSR activities and decisions are communicated in an effective way to the stakeholders is a strategic move in the stakeholder information strategy (Morsing & Schultz, 2006).

2. Stakeholder response strategy

This communication strategy is based on a two-way asymmetric communication model, which means that the flow of communication is between the company and the public on a two-way basis. The term asymmetric means in this situation that there is an imbalance from the effects of public relations and the impacts on the company. This means that the com-pany attempts to change the attitudes and the behavior of the public rather than to change themselves according to the public‟s attitudes. In order to be able to succeed with this the company needs to make the corporate actions and decisions that are relevant for the

stake-holders as the company is dependent on the external support from its stakestake-holders. Two ways of applying this communication strategy is for the company to conduct a market sur-vey or an opinion pull to receive feedback on the opinion of the public. According to Morsing and Schultz (2006) the stakeholder response strategy is, although it is a two-way approach, still a quite sender-oriented approach since the company is only interested in the convincing its stakeholders of its attractiveness and not really interesting in changing their existing strategies (Morsing & Schultz, 2006).

3. Stakeholder involvement strategy

In this communication strategy there is a more balanced relation between the company and its stakeholders. Dialogue is the base for the communication and persuasion may be present however, it comes from the company itself as well as from its stakeholders. Both parties are likely to change as a result of pressure from the two parties respectively. This communication strategy encourages continuous negotiations between the company and its shareholders as well as accepting necessary changes whenever the need may occur. By hav-ing this dialogue it enables for the company to keep up with the changhav-ing expectations from the stakeholders as well as its own possible influence on those expectations, but also letting the company be influenced by the same expectations. The different ways how to take on the stakeholder involvement strategy are for the companies to frequently engage in a dialogue with its stakeholders. This is an efficient way since it allows the stakeholders to be more involved and for the company to understand and adapt to their concerns when it comes to CSR initiatives (Morsing & Schultz, 2006).

Three CSR Communication Strategies

Table 2 Three CSR Communication Strategies. Source: Morsing & Schultz, (2006)

The stakeholder information strategy

The stakeholder

re-sponse strategy The stakeholder in-volvement strategy Communication

ideal: (Grunig &

Hunt, 1984)

Public informa-tion, one-way communication

Two-way asymmetric

communication Two-way communication symmetric

Communication ideal: sense-making and sense-giving Sense-giving Sense-making Sense-giving Sense-making

Sense-giving –in iterative progressive processes

Stakeholders: Request more in-formation on corporate CSR ef-forts

Must be reassured that the company is ethical and socially re-sponsible Co-construct corporate CSR efforts Stakeholder role: Stakeholder influ-ence: support or oppose Stakeholders respond to corporate actions

Stakeholders are in-volved, participate and suggest corporate actions

Identification of

CSR focus: Decided by top management Decided by top man-agement, investigated in feedback via opi-nion polls, dialogue, networks and part-nerships

Negotiated continuously in interaction with stake-holders

Strategic com-munication task:

Inform stake-holders about fa-vorable corporate CSR decisions and actions

Demonstrate to stakeholders how the company integrates their concerns

Invite and establish fre-quent, systematic and pro-active dialogue with stakeholders, i.e. opinion makers, corporate critics, the media, etc.

Corporate communication department’s task: Design appealing concept message Identify relevant stakeholders Build relationships

Third party en-dorsement of CSR initiatives:

Unnecessary Integrated element of surveys, rankings and opinion polls

Stakeholders are them-selves involved in corpo-rate CSR messages

3

Research Design and Method

In the method chapter the authors will explain how they conducted the study, and provide the reader with a motivation for the chosen method. A closer description of the two companies and the respondents will be presented.

3.1 Research approach

The role of the researcher is to create a link between theory and what occurs in practice. However, there is not an easy straightforward way to approach this. In general there are two different research approaches to take on when it comes to the relationship between theory and research, deductive and inductive approaches (Zikmund, 2000).

The authors of this thesis did regard neither the deductive nor the inductive approach, in their pure ways, to be appropriate for the type of research that was the focus for this thesis. This was due to the fact that the deductive approach prefers large samples of sufficient numerical size in order to enable for the researcher to generalize the results (Saunders, Lewis, & Thornhill, 2007). As the purpose of this research was to find out how certain SMEs in the Småland region defines and communicate CSR, the authors did not regard the deductive approach to be relevant. The reliability and ability to generalize the developed theory is somewhat threatened when using an inductive research approach. This is because the developed theory is only relying and applicable to a specific situation, time or group of people (Patel & Davidsson, 2003). Consequently, the authors of this thesis did not consider the inductive approach to be appropriate either for this research. Instead a combination of the deductive and inductive approach was used.

Abduction is a combination of the inductive and deductive research approach. If a re-searcher uses a strict inductive or deductive approach, they may be „locked‟ to their strict approaches. When taking on an abductive approach the researcher is more „free‟ to carry out the research (Patel & Davidsson, 2003). The previous research concerning CSR and communication suggest different perspectives on how to define CSR and how to commu-nicate it. What could be found in previous research was also that different companies ap-proaches and uses CSR in different ways. Due to this, the authors considered the abductive approach to be the most appropriate research approach for the purpose of this thesis. Re-levant scientific theories were chosen and the aim was to try to confirm the empirical re-sults by relating to the theories.

Depending on the purpose of the research, the researcher can consider different types of research study approaches. These different research strategies are depending on the nature of the purpose of the research. The purpose of the research can be exploratory, descriptive, or explanatory. For this thesis the authors applied a combination of the explanatory and exploratory studies.

3.2 Literature Review

During the early stages of this research, background information was gathered in the form of previous research within the field of CSR and SMEs and CSR communication. This in-formation was needed in order for the authors to get inin-formation about the background to the problem. The literature was also used as a base for the frame of reference as well as a base for the study. These sources were found using the electronic databases provided by the university library. Using these databases the authors could find relevant scientific

ar-ticles as well as books concerning the areas of interest. Finding previous research about CSR was relatively easy compared to finding information about CSR and SMEs. It became obvious to the authors that CSR communication and SMEs was a relatively new area in the research about CSR and this fact also contributed to the final focus and purpose of the study.

When searching for relevant articles regarding CSR communication and SMEs, the authors used a so called snowball sampling, which means that when finding one relevant article this lead on to other relevant articles through its cited references (Saunders et al., 2007). Con-cerning CSR and CSR communication relevant articles and books could more easily be found without using the snowball sampling.

Concerning the accuracy and reliability of the used literature, the authors have considered this when relating to the literature. General information about CSR have been used from a variety of sources, both older sources and newer. Since researcher has started to focus on CSR and SMEs during the last couple of years, these sources are more recently. The au-thors consider the accuracy of the information to be good since the sources are both up-to-date when it comes to CSR and SMEs and well established when it comes to information about CSR.

3.3 Data Collection

There are different techniques when it comes to gathering primary data. Which technique to use is much depending on the nature and purpose of the study (Saunders et al., 2007). In order to fulfill the purpose of this study, the authors needed to collect both primary and secondary data. The primary data was the actual investigation of the selected companies and the data from this study was then related to the scientific research that has been col-lected for the frame of reference.

3.4 Qualitative Data collection

According to the aim of the study a researcher can collect data that is either of quantitative or qualitative character. Quantitative data is characterized by numbers and are focusing on quantity, amount and number of variables that can be analyzed statistically. A quantitative approach is suitable in a situation where the researcher already has knowledge about what is going to be tested and for testing hypotheses. Studies which are characterized by the use of text, words and actions are qualitative studies. The main focuses of such studies are to understand the „whole picture‟ in a certain situation. This is more important than the un-derstanding of specific parts (Christensen, Engdahl, Grääs, & Haglund, 2001).

When a researcher wants to investigate a deeper meaning within a context, qualitative stu-dies are suitable. This is because qualitative stustu-dies require data collection methods that are sensitive to an underlying meaning when collecting and analyzing the data (Merriam, 2001). In this study the authors decided to conduct data of a qualitative character since they aimed at receiving more in-depth information about specific SMEs in the Småland region. The authors had no ambition in making any analysis that could be generalized for the whole population of SMEs in the Småland region. Rather it was the authors‟ ambition to look at two companies in particular and study them in-depth in order to understand them tho-roughly in this context. The reason for this was that since CSR is such a complex term and many companies, and SMEs in particular, find the term a bit confusing (Murillo & Lozano,

2006) it might be reason to believe that different companies define and work with CSR in different ways.

3.5 Case study approach

One way to conduct data of qualitative character is to study one or more cases. A case study is an investigation of a small limited group. It can be a group of individuals, an organ-ization or a specific situation. One can also study more than one case for example two or-ganizations (Patel & Davidsson, 2003). Qualitative case studies are investigations that are intensive and analytical descriptions of one single entity. When it comes to the case study approach, there are no common methods for how to collect and analyze the empirical data, in opposition to how to collect data for experiments and survey investigations. Any me-thod for collecting data can be used for the case study approach, although some meme-thods are more common than others (Merriam, 1994). According to Stake (1995), a case study approach is used in order to catch the complexity of a single case that is of very special in-terest in itself. When a researcher wants to understand the complexity, distinctiveness and the activity of a specific case in a given circumstances, the case study approach is relevant (Stake, 1995).

There are two types of case studies. The intrinsic case study which a study is called when the case is given. The researcher does not choose the case to be studied because he or she is interested in this particular case or to learn about some general problem by just studying this case, rather because the researcher needs to learn about one particular case that is al-ready pre-selected with no alternatives. In another situation there might be a need for a general understanding of a phenomena and the researcher might get an insight into a ques-tion by just studying a particular case. This is called an instrumental case study and allows the researcher to get an understanding of something rather than an understanding of a par-ticular case. There is also ability for the researcher to study more than just one instrumental case. By applying the collective case study approach the researcher allows studying more in-strumental cases where each case is studied in itself but also in coordination with other cas-es (Stake, 1995).

The authors of this thesis considered the case study approach to be the most relevant me-thod for the purpose of this thesis since this approach would enable for the authors to in-vestigate how certain SMEs in the Småland region work with CSR and how they communi-cate it. The concept of CSR can be considered to be somewhat fuzzy by some companies and this might imply that different companies work differently with CSR. Due to this as-sumption, the authors never aimed at generalizing the findings on all SMEs in the Småland region. The collective case study approach was chosen by using instrumental case studies, since the purpose of the study was to investigate how CSR is defined and communicated in SMEs in the Småland region. It was not the focus of the study to investigate an already giv-en case.

3.6 Selection of cases

According to Stake (1995) there is no point in selecting a few samples with the aim of mak-ing them representative or typical of other cases, since a sample of one or just a few cases is not likely to be a strong representation of other similar cases. The reason for this is that the researcher does not study one case in order to understand other cases, rather to understand this one particular case (Stake, 1995). Since the purpose of this study was to investigate how SMEs define and communicate their CSR activities there was no aim at trying to in-vestigate cases that could be representative for the entire population. As Stake (1995) ar-gues, it is more interesting to investigate one particular case to see how it behaves and not to see whether the results can be representative or not.

The authors chose to investigate two cases and the reason for this was simply to see any potential differences or similarities in relation to the purpose of the study. As the aim of the study was to investigate how SMEs define and communicate CSR, the authors chose to investigate SMEs in the manufacturing industry. This was based on the assumption made by the authors that it would be relatively easy for companies in this type of industry to talk about their CSR activities since it is relatively easy to measure and give actual examples from a manufacturing point of view. When decided on the manufacturing industry the se-lection was even further detailed by choosing companies in the building module manufac-turing industry. This was based on the fact that there are many SMEs in the Småland re-gion operating in this particular type of manufacturing industry.

Instead of investigating one single case, the authors choose to investigate two different cas-es within the same industry. One Busincas-ess-to-Consumer, (B2C) case and one Busincas-ess-to- Business-to-Business case, (B2B), case. The reason for choosing two different samples was first to learn about the two samples specifically and also to see any potential differences or similarities between the two cases. This was not done in order for the authors to draw any general conclusions or assumptions between B2B and B2C companies, rather to investigate the dif-ferences and similarities between these two samples in particular.

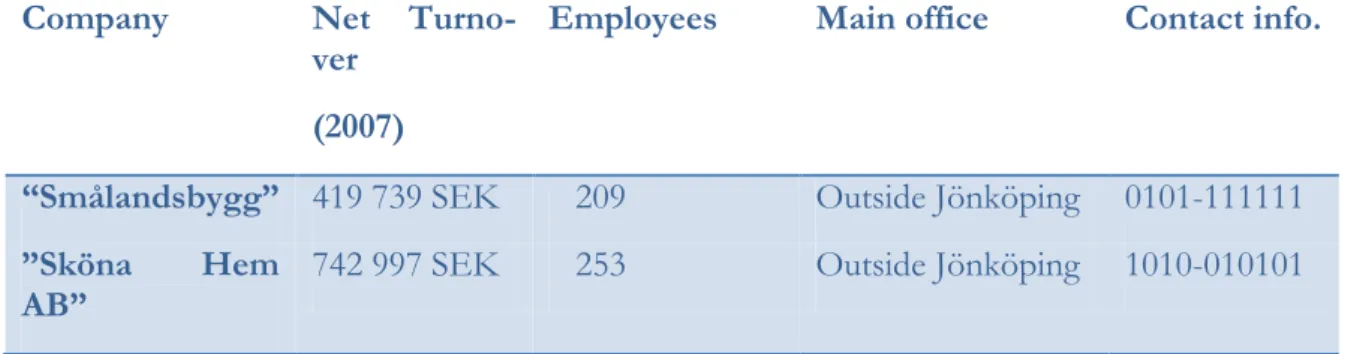

In order to create the sample of case studies, probability sampling was used by the use of a database. UC webSelect is a database containing financial information about all registered companies in Sweden. The user of the database is able to select a sample of companies based on his or her preferences. The authors of this thesis chose a number of criteria‟s in order to create the sample of cases. Turnover, County/Municipality/Zip code, numbers of employees, industry- both primary and secondary activity was selected in order to create a sample. When these criteria‟s were selected, samples of seven companies were created. The authors wanted two case companies that were rather similar in size, in order to make rele-vant comparisons between the two. Previous research suggests that SMEs that have more than 100 employees are more likely to communicate their CSR activities, and due to this fact the authors made an additional selection form the seven companies to get a sample of companies that had more than 100 employees. When this was done, three companies were left in the sample; Smålandsbygg, Sköna Hem AB and Smålandsvillan AB. When contact-ing all three companies, Sköna Hem AB and Smålandsbygg choose to participate while the authors had a hard time getting in contact with Smålandsvillan, whereby the authors ap-plied convenience sampling and choose the first two to participate in the study. Due to the fact that the company representatives wanted to appear anonymous in the report, the names of the companies are fictional.

Company Net Turno-ver

(2007)

Employees Main office Contact info.

“Smålandsbygg” 419 739 SEK 209 Outside Jönköping 0101-111111

”Sköna Hem

AB” 742 997 SEK 253 Outside Jönköping 1010-010101

Table 3 Case Selection, Source: UC webSelect. Selection created 2009-04-14

3.6.1 Presentation of Case Companies Smålandsbygg

Smålandsbygg is a B2B (Business to business) company in the office, school and other offi-cial buildings producing industry. The company produces and sells building modules to other companies that are building schools and other official buildings. The company has head quarters and production facilities in a small town outside Jönköping. In 2007 the company had a turnover of 419 739 SEK and had 209 employees. The representatives cho-sen to participate in the study were;

Vice CEO

The SHEQ manager (Safety, Health, Environmental and Quality) Production manager

Marketing manager Sköna Hem AB

Sköna Hem AB is a house producing company with headquarters in a small town outside Jönköping. The company produces and sells prefab house modules to private consumers all over Sweden. In 2007 the company had a turnover of 742 997 SEK and had 253 em-ployees. The representatives chosen to participate in the study were;

CEO

The SHEQ manager (Safety, Health, Environmental and Quality) Production manager

Sales manager

As the aim of this study was to investigate how SMEs define and communicate their cor-porate social responsibility, the authors considered it to be crucial to talk to persons in the companies that are likely to be responsible for these types of issues. The aim was to talk to as many company representatives as possible at corporate management level. As the se-lected companies are relatively small in size, they did not have more than three to four per-sons at the corporate management level. That is the reason for why these four perper-sons were selected to participate in the study. The reason for why the vice CEO has participated instead of the CEO at Smålandsbygg is because the authors were not able to get in touch

with the CEO after several attempts. However, it is the authors‟ perception that interview-ing the vice CEO instead of the CEO did not affect the results of the study to any suffi-cient degree.

3.7 Qualitative Interviews

The case study approach allows several different data collection techniques. The use of qualitative interviews is common when it comes to conducting qualitative data in case stu-dies. There are several different types of qualitative interviews. In general there is a low lev-el of standardization when it comes to qualitative interviews. That is, the questions that the interviewer poses to the respondent give him or her ability to answer using their own words. The purpose of using a qualitative interview approach is for the researcher to be able to discover and identify characteristics and distinctiveness of something i.e. a person‟s perception about something (Patel & Davidsson, 2003).

The authors of this thesis chose to apply qualitative interviews in order to receive qualita-tive in-depth information from the respondents about CSR. As the aim of the study was to investigate a rather wide term as CSR, the authors argued that qualitative interviews could provide in-depth answers as the respondent is allowed to answer „freely‟ on the questions posted during the interview. It also allows for the respondent to ask the interviewer ques-tions if they would not understand some quesques-tions or words used. Applying qualitative in-terview technique would also allow for the inin-terviewer to pose follow-up questions if needed. Since some of the aimed questions were open and complex, it would also be most appropriate to apply qualitative interviews (Christensen et. al, 2001). Again, due to the fact that the authors aimed at investigating the definition and communication is such a wide term as CSR, it was appropriate to apply qualitative interviews.

The initial aim was to use face-to-face interviews as this type of interviews enables more and better control over the interview situation for the interviewer, compared to for exam-ple interviews conducted over the phone. Personal interviews also allow more comexam-plex questions to be posted (Christensen et. al, 2001). However, when approaching the respon-dents, none of them was interested in devoting the time and extra cost a personal visit would inquire. Due to that, the authors decided to use phone interviews instead which was accepted by the respondents. It is not the authors‟ perception that using phone interviews instead of personal interviews has had any affects on the results from the study, as the res-pondents would probably not have answered differently on the questions in a face-to-face interview than they did during the phone interview. This is due to the fact that CSR is not a „sensitive‟ subject to discuss, where personal emotions can affect the respondents answers compared to for instance a subject like personal bankruptcy which is a much more emo-tionally charged subject. CSR can rather be considered a fairly „easy‟ subject to discuss with anyone.

The interviews were conducted at home at one of the authors, during the weeks 18-20 and they lasted for approximately 45-60 minutes. In order for the respondents to feel conve-nient and to be able to express themselves correctly, the interviews were held in Swedish. A tape recorder was used to record the interviews in order for the authors to easier go back and listen once more to the interviews. The results were presented in the empirical find-ings. It is the authors‟ perception that the respondents, in general, had some difficulties answering the questions related to CSR. This is most likely due to the complexity of the term corporate social responsibility. The respondents tended to make pauses and sigh