Sustainability reports: environmental

friendly or a greenwashing tool?

- A study of how global mining companies use sustainability reports

Master thesis within business administration 30 ECTS

AUTHORS: Johannes Landén & Edvin Malmberg TUTOR: Professor Gunnar Rimmel

Acknowledgements

We would like to thank our tutor Gunnar Rimmel for his help and expertise as well as his constant availability when we had questions. We would also like to thank our friends for contributing to a pleasant study environment during this semester.

Jönköping 2016-05-23

_________________ _______________

Master Thesis in Business Administration

Title: Sustainability reports: Environmental friendly or a greenwashing tool

Authors: Johannes Landén

Edvin Malmberg

Tutor: Professor Gunnar Rimmel

Date: 2016-05-23

Key Words: Sustainability report, Global Reporting Initiative, Greenwashing

Abstract

Background and Problem

Recent decades have shown an increasing amount of products, services and companies claiming to be environmental friendly. Reasons for these claims have been public demand for environmental sustainability, combined with, the gap between company disclosure and the public’s ability to verify information. This has increased the pressure of conducting sustainability reporting and frameworks like the GRI has been developed. Sustainability reporting has, however, been criticized for leaving too much room for the company management to choose what information to publicly disclose. Hence, creating the possibility for companies to conduct sustainability reports not accurate providing the truth, but merely selected parts of the environmental performance.

Purpose

To investigate the information in sustainability reports from companies in the mining industry compared with information from published independent information in order to find out if the sustainability reports may be used as a tool for greenwashing.

Delimitations

The study will investigate companies in the mining sector with sustainability reports based on the GRI framework. It is limited to the largest companies in this sector as well as to reports using English. It will include reports covering the years of 2012-2014.

Method

The study uses mainly qualitative data but with few elements of quantitative data. The data has been gathered from the sustainability reports as well as from independent sources. A disclosure checklist has been constructed and Dalmas & Burbano (2011) matrix of how to define greenwashing has been used.

Empirical findings and results

The findings shows that the selected companies have been involved in several scandals and controversies, which contradicts the visions, values and strategies stated in the reports. The reports, at the first glance, give a picture of companies working actively to improve their environmental performance but numerous statements as, “whenever possible”, distances them from doing the little extra. Hence, as they do not state to have a perfect environmental performance, they have not been categorized as greenwashing firms.

Abbreviations

CSR Corporate Social Responsibly GRI Global Reporting Initiative

Definitions

GreenwashingWhen making claims about the environmental performance that are either only partially true or completely false.

Published independent information

Umbrella term for information collected concerning the scandals and controversies. Example, News articles.

GRI Indicators

The measurement for one specific impact of the organizations operations. Example, Amount of water used or energy consumption by primary source.

GRI Aspects

Table of Contents

1

Introduction ... 1

1.1 Background ... 1 1.2 Problem Discussion ... 3 1.3 Research Questions ... 4 1.4 Purpose ... 5 1.5 Delimitations ... 52

Frame of references ... 5

2.1 Greenwashing ... 5 2.2 Impression Management ... 7 2.3 Sustainability Reporting ... 72.4 Global Reporting Initiative ... 8

2.5 Transparency and Disclosure ... 10

2.6 Stakeholder Theory ... 11

2.7 Legitimacy Theory ... 12

3

Methodology ... 13

3.1 Research strategy and approach ... 13

3.2 Studied Companies ... 15

3.3 Data collection ... 16

3.4 Credibility check ... 16

4

Findings/Empirical findings ... 17

4.1 BHP Billiton ... 17

4.1.1 Information in Sustainability reports ... 17

4.1.1.1 Information in CEO-statement ... 17

4.1.1.2 Information under the aspects sections ... 18

4.1.2 Scandals and controversies ... 19

4.1.2.1 Borneo coal mining controversy ... 19

4.1.2.2 George’s River pollution ... 20

4.2 Rio Tinto ... 22

4.2.1 Information in Sustainability report ... 22

4.2.1.1 Information in Chairman’s Letter ... 22

4.2.1.2 Information in CEO Statement ... 22

4.2.1.3 Further information of interest ... 23

4.2.1.4 Information under the aspects ... 24

4.2.2 Scandals and controversies ... 26

4.2.2.1 2012 London Olympics and Bingham Canyon Mine, Utah ... 26

4.2.2.2 Oyu Tolgoi copper mine, Mongolia ... 27

4.2.2.3 Grasberg mine. West Papua, Indonesia. ... 28

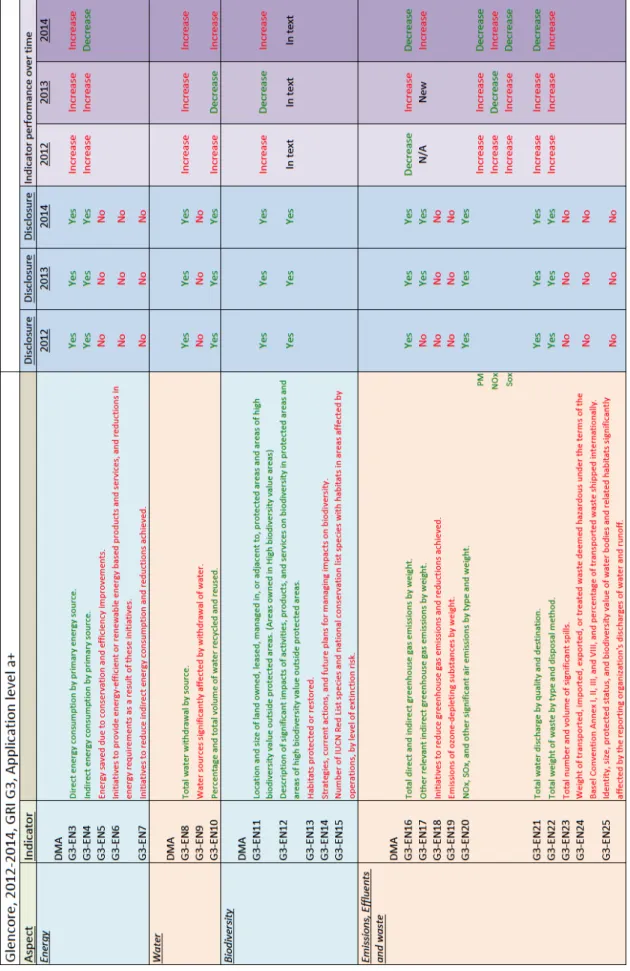

4.3 Glencore ... 30

4.3.1 Information in Sustainability report ... 30

4.3.1.1 Information in Chairman’s Letter ... 30

4.3.1.2 Information in CEO Statement ... 30

4.3.1.3 Further information of interest ... 31

4.3.1.4 Information under the aspects sections ... 31

4.3.2 Scandals and controversies ... 33

4.3.2.1 Mopani copper mine, Zambia ... 33

4.3.2.2 Luilu Refinery, Katanga province in Congo ... 34

4.3.2.3 Macarthur River Zinc Mine, Australia ... 35

4.4 Vale ... 37

4.4.1.1 Information from Board of Directors ... 37

4.4.1.2 Information from the President (CEO) ... 37

4.4.1.3 Further information of interest ... 38

4.4.1.4 Information under the aspects sections ... 39

4.4.2 Scandals and controversies ... 40

4.4.2.1 The award “World’s worst corporation of the year” ... 40

4.4.2.2 Carajás Railway ... 40

5

Analysis ... 43

5.1 BHP Billiton in the context of greenwashing ... 43

5.2 Rio Tinto in the context of greenwashing ... 44

5.3 Glencore in the context of greenwashing ... 47

5.4 Vale in the context of greenwashing ... 49

6

Conclusion ... 52

7

Discussion ... 53

8

Ethical Issues ... 54

Figures

Figure 1: A Typology of Firms based on Environmental Performance and

Communication ……….6

Tables Table 1: Disclosure checklist – Empty………14

Table 2: Disclosure checklist – BHP Billiton ………..21

Table 3: Disclosure checklist – Rio Tinto………....29

Table 4: Disclosure checklist – Glencore ………36

1 Introduction

In November 2015 a water dam, run by Brazilian iron ore miner Samarco, burst and caused a major flooding. Samarco is a 50/50 joint venture between BHP Billiton and Vale and the disaster caused 19 fatalities, ruined hundreds of homes and contaminated a major river (Reuters, 2016). The Brazilian government and Samarco later agreed upon a settlement of $5.1 billion in compensation (Reuters, 2016). Samarco has been accused of continual negligence prior to the disaster with prosecutors saying that damns like these should not be able to fail without reason and, as an example, that water testing of the water in the dam declared dangerously high levels of arsenic even though regulations are in place (abc news, 2016).

An incident like this sparked an enthusiastic curiosity on how and why environmental incidents like this occur? Previous courses of our university education have taught us about sustainability reporting and how covered aspects as the environmental impacts from global corporations are. Yet incidents like these evidentially still occur which begs the question; are corporations as responsible and trustworthy as they claim or are there major flaws in today’s company disclosures.

1.1 Background

Greenwashing is a phenomenon that is highly relevant in today’s society where the term greenwashing is connected with companies that make claims, either not accurate or completely false, about their environmental performance.

In the early 90´s surveys where handed to the public to find out their mind-set about the environment and the result of the surveys showed something that environmentalist groups had been trying to rise the concern about for decades. The result of the survey showed that most of the people asked had concerns about the environment and they where willing to change their consumption habits to make a contribution to the sustainability of the environment. The big break through here was that the general public went away from relying on the governments regulations being enough by itself and started to understand that they where a big part of the solution. With this increase of people concerned about all steps behind the finished products, companies started to capitalize on the new demand and

started to make changes, ranging from how products where made to how products where marketed.

The 90´s boom in environmental friendly products has continued to increase to this date and it has brought numerous possibilities for companies around the world. One example is the competitive advantage environmental friendly products can give is when there is only a marginal increase of price for the environmental friendly labeled products, or so called labeled products (Feinstein, 2013). One issue that have followed this increase of eco-labeling is that there is a huge amount of different labels, prices and awards, making it impossible for the general public to follow up on and make sure that the claims of the labels are accurate. As a result of this there has been room for companies to make environmental friendly claims that are inaccurate, misleading or even completely false. In 2012 TerraChoice, an environmental marketing firm, made a study of 5,296 products of which all of them had some claim of being environmental friendly. 265, or 5%, of the products where found to be as green as they claimed which gives the staggering result that 95% of these products had some kind of greenwashing in the description (TerraChoice, 2010).

As society have become more aware of the importance of long-term sustainability and the fact the there are environmental claims that are not always true, the result have been that the accountability pressure, especially for large companies, have increased substantially and society have started to demand more transparency within this area (Kolk, 2006).

One way for companies to meet this demand and to communicate their view on sustainability as well as their environmental and social performance is by conducting a sustainability report, which is a report containing most of the CSR related information society and investors now often demand. Many have welcomed the increasing demand for transparency regarding environmental and social performance but there are also people that believe the quick development and the relatively young age of these reports have increased the possibility to conduct greenwashing. This because of the comparability issues with the many sustainability reports and that the regulatory progress of the disclosures have been slower the than publics demand for this kind of information (Delmas & Burbano, 2011). As a result of the increasing pressure from stakeholders to act in a sustainable manor it has become politically risky to be an opponent to sustainable development. This change has

resulted in that it now has become a norm to embrace these actions and commitments to inflate credibility in organizations. One specific sector that has been questioned of ever being able to act in a sustainable manor is the mining sector as the nature of the business is to collect what nature has built up during centuries. As a result of this, CEO´s of large mining corporations understood the part they could play in the development of sustainability, which in the year of 2000 resulted in the creation of the Global Mining Initiative (GMI) (Young, 2005). One of the major results of this initiative was that the almost 150 members where required to conduct sustainability reports based on the GRI framework and its Mining and Metals Sector Supplement. To further try to lower the mistrust towards the sector these organizations where also required having an external assurance of these reports. (Fonseca, How Credible are Mining Corporations’ Sustainability Reports? A Critical Analysis of External Assurance under the Requirements of the International Council on Mining and Metals, 2010)

Despite the initiatives from sectors as the mining sector greenwashing still occurs in the corporate world and with the room for improvement regarding a worldwide standard and the lack of comparability among the different frameworks for sustainability reports, greenwashing will remain a problem. The many alternatives, the inadequate progression of the regulations, the lack of reliability and comparability is today some of the biggest problems within the area of sustainability reporting. (Parguel, Benoît-Moreau, & Larceneux, 2011)

1.2 Problem Discussion

Corporate social responsibility is more and more used as a communication tool to enhance companies’ image towards the public. An example of this is environmental legitimacy, which is an important part of management research since organizations tend to be more competitive if they are successful in establishing environmental legitimacy (Berrone, Fosfuri, & Gelabert, 2015).

However, the strategically well-designed advertisements used can be problematic to truly control, making it hard to sort out what companies are or are not truly as CSR-aware as they claim. This provides companies with an incentive to use greenwashing (Parguel, Benoıt-Moreau, & Larceneux, 2011). Greenwashing has been defined as “the practice of making unsubstantiated or misleading claims about a firm’s environmental impact”

(Berrone et al., 2015, p. 315). It can be difficult for stakeholders to get enough information about environmental footprints of various organizations in order to evaluate if the organizations’ environmental statements are accurate, causing an information asymmetry (Berrone et al., 2015). Laufer (2003) expresses concerns about the potential to engage in GRI-reporting as a tool for greenwashing giving companies a marketing advantage.

In recent years, a vision of sustainable mining has increased among mining corporations, particularly large global mining corporations (Fonseca, 2010). It can, however, be questioned if the mining industry can be sustainable or environmentally friendly at all (Mallet, 2008). Mallet (2008) refers to MiningWatch Canada, which claims that there is no such thing as a environmental friendly mining company. Fonseca (2010, p. 356) states that “despite the apparently paradoxical nature of the expression ‘sustainable mining’, past years have witnessed a proliferation of initiatives promoting this vision. Among the most notable are the ones carried out by global mining corporations”.

The emergence of sustainability reporting has created an uncertainty about how reliable company disclosures really are. A discussion about the fact that companies have a lot of freedom in altering the information in sustainability reports has been started, where the organizations ability to describe confident and positive views in the message delivered to report-readers is in focus (Fonseca, 2010).

According to Fonseca (2010), disclosing corporate social responsibility based on the GRI framework can in some cases be meaningless since a matter of “what we are doing” shines through more than critical changes or damages. He argues that sustainability assessments need a deeper reflection of the socio-ecological systems where they are conducted. He even goes to the length of claiming that GRI-reports can misinform readers and disguise corporate unsustainability, thus causing a problem of an information gap between readers and companies (Fonseca, 2010).

1.3 Research Questions

• How do companies in the mining sector use sustainability reporting and the GRI framework and can any indications of greenwashing be found when comparing them to published independent information?

1.4 Purpose

The purpose of the report is to investigate the reporting of the environmentally preservative actions global mining companies claim to do. Furthermore, the results of the reports released by the companies in question will be examined and analyzed to ultimately discover if the global mining companies actually work actively towards their stated environmental goals or if greenwashing occurs.

1.5 Delimitations

This thesis is limited to events and reports covering the years of 2012-2014 since the 2015 sustainability reports were not yet released by all four companies at the time of the investigation. This thesis is also limited to the GRI framework aspects: Energy, Water, Biodiversity, Emissions, Effluents and Waste as the information related to the study is concentrated to those particular aspects. The thesis includes the largest companies in the mining sector based on market value in 2015, where China Shenhua Energy, which is the fourth largest has been replaced by Vale. This was due to the fact that China Shenhua Energy only releases sustainability reports based on Chinese which none of the researchers have adequate knowledge about in order to be able to treat them in the same way as the other companies.

2 Frame of references

2.1 GreenwashingThe term greenwashing, or more specific the illusion a company wants to create when stating that they are doing good towards the environment when they in reality do not or even do the opposite, have it origins from the environmentalist Jay Westerveld’s essay about the hotel industry. He noticed the hotel industries usually had a “save-the-towel” project, a project which asked quests to put the towel back on its place if it where to be reused. He claimed that it was merely a way for the hotels to cut down on laundry costs while the hotels claimed that it was an initiative to act for the environment (Sanders & Wood, 2015).

The concept of greenwashing can be divided into two different levels, where one is the firm-level greenwashing where a company tries to give the public a picture of the company´s environmental performance which, is not completely true or even false. The

other one is the product-level greenwashing where a company gives false information about the environmental benefits of its products. Delmas & Burbano (2011) uses a matrix to describe when greenwashing occurs. Companies with good environmental performance are called green companies and

companies with bad environmental performance are called brown companies. Further the authors describe the companies that positively communicate their environmental performance as vocal companies and companies that do

not communicate their

environmental performance as silent. As figure 1 shows, companies that have a bad environmental performance and at the same time communicate positively about their

environmental performance are categorized as greenwashing firms. Dalmas & Burbano (2011) further describes the drivers of greenwashing as first and foremost being a result of the monitoring and pressure of media and non-governmental organizations as well as the lack of regulations regarding greenwashing.

This combined with drivers as consumers demand for certain labels on products, the competitive pressure, the characteristics of the firm and optimistic bias of the manager’s are some examples for why greenwashing is conducted.

Du’s (2015) study of how markets react to greenwashing shows that markets are more prone to relay on earlier impressions of the company when the environmental claims are proved wrong and that the investors and the market´s trust towards companies future statement will be damaged if these claims are not followed through. It further shows that the media plays a big part in making the market react on greenwashing, especially in developing countries as the business ethics and the governmental regulations generally are not as evolved as in developed countries.

Figure 1: A Typology of Firms based on Environmental Performance and

2.2 Impression Management

The study of how people display themselves in order to strengthen their image towards others is called Impression management. It lies within the field of social psychology and has been defined as “the conscious or unconscious attempt to control images that are projected in real or imagined social interactions” (Hooghiemstra, 2000, s. 60). Impression management as a theory has, even though originally being aimed against individuals, been used considerably in order to describe the actions taken by organizations facing legitimacy threats (Hooghiemstra, 2000). CSR can, according to Hooghiemstra (2000) be used as impression management and can contribute to an organization’s image. Merkl-Davies & Brennan (2011) lists four theoretical perspectives on managerial impression management in order to improve the knowledge regarding a corporate reporting matter, which are Economic-, Social psychology-, Sociology- and Critical perspective.

The Economic perspective reflects how there is an information asymmetry, which is being used by managers in order to manipulate the disclosure of information and thus maximizing their personal wealth. In this case, corporation-written documents are used to disclose a corporate performance ideal for personal interests. Regarding the Social psychology perspective, managers tend to use impression management as a tool in the reporting process when expecting an evaluation of their performances. Managers accountable towards external stakeholders can use this to avoid certain negative consequences by responding in advance with acceptable reports and results. The Sociology perspective is focused on the effect of stakeholder groups or society at large and how organizations make their disclosure decisions in accordance to “consensually developed systems of norms and values”. Lastly, the Critical perspective challenges the conventions of instrumental rationality. To achieve rational decision-making, managers may use corporate-written documents where decisions are assumed not to be made in accordance with “self-interest”. (Merkl-Davies & Brennan, 2011)

2.3 Sustainability Reporting

A Sustainability report is a non-financial report that organizations publishes to state what economic, environmental and social impacts their activates have on society. It also states the values of the organization, the governance model, the strategy of how to achieve goals and what they are currently doing towards society. (GRI, 2015) One of the major goals

with sustainability reporting is to gain acceptance by key stakeholder as government or employees as well as pressure groups as environmental protection groups and human rights associations (Schaltegger, Bennett, & Burrit, 2006).

According to KPMG (2015) there has been an increase in usage of sustainability reports which have made researchers aware of the need and importance of development regarding standards, guidelines and frameworks to enhance comparability between the reports and to lower the costs of conducting the reports (Christofi, Christofi, & Sisaye, 2012) (Kitzmueller & Shimshack, 2012). Progress have, however, been made in this area and as a result of the European Unions initiative on Corporate Social Responsibility the European parliament amended the 2013 Accounting directive for so-called public interest entities with more than 500 employees. The amendment will require these companies to disclose relevant non-financial information as environmental matters, social and employee-aspects, respect for human rights, anti-corruption strategies, bribery issues and the diversity of the board of directors. It will start to be mandatory reports released in 2018 covering the financial year of 2017-2018 (The European Parliament and The Council of The European Union, 2014). There has been critique about whether or not sustainability reporting is something that actually has a positive effect on the management, making them act in a more responsible way, or if it just is a way to handle their public relations (Blanding, 2011).

2.4 Global Reporting Initiative

GRI is an international independent organization, which educates organizations on how to manage disclosures of different impacts business operations has on important sustainability concerns such as climate change. (GRI, 2016a). Global Reporting Initiative primarily focuses on promoting economic, environmental, and social sustainability (Fernandez-Feijoo, Romero, & Ruiz, 2013). In doing so, GRI provides all companies and organizations with a comprehensive framework on sustainability reporting, which is commonly implemented around the globe (Fernandez-Feijoo, Romero, & Ruiz, 2013). This enables the reporting on sustainability to be more easily applicable and more comparable between organizations.

The Global Reporting Initiative was first introduced in 1997 when the Coalition for Environmentally Responsible Economies (CERES) discovered some flaws in companies’ sustainability reporting (Willis, 2003). Requests for information about environmental and social reporting and the inconsistence and incompletion among reports causing incomparability were some critical factors inspiring change (Willis, 2003). In 1998, a multi-stakeholder Steering Committee was formed in order to navigate the organization correctly (GRI, 2016b). The committee issued a pivotal mandate to do more than the environment, widening the range of interest to social, economic and governance issues. In 2000, the first edition of the guidelines was released, becoming the first global framework for sustainability reporting (GRI, 2016b).

The framework has through the years been developed to the current guidelines of today, the G4-guidelines, which is structured into two main parts. The first part is called Reporting Principles and Standard disclosures and focuses on reporting principles, standard disclosures, and criteria to be applied in order to prepare an organizations sustainability report (GRI, 2013a). The second part is called the Implementation Manual and primarily contains details of how to apply the reporting principles, how to prepare the information and an explanation of the concepts in the framework (GRI, 2013a). This framework is the fourth line of main editions of the GRI and was publicly revealed in May 2013 (GRI, 2013b). It has been called “a major step forward in the evolution of sustainability reporting” by experienced reporters (GRI, 2013b).

Indicators, briefly mentioned above, constitute an important part of the GRI report. They are divided into different aspects, used as headlines, where the specific indicators are listed accordingly. For example, under the water-aspect the different water specific indicators are listed. The usage of indicators is a way to monitor economic, environmental and social performance and also to measure what kind of impacts an organization has had (GRI, 2013a). Material aspects are the most significant impacts from activities performed concerning both the organization itself, but also concerning the various stakeholders (GRI, 2013a).

Skouloudis et al. (2010) made a study about the GRI framework and its quality. They came to the conclusion that the reports studies had major gaps and that many of the companies failed to achieve the key purposes of the reports, which is to promote stakeholder

engagement and to follow trough on the organizational accountability towards society. They further found that the vision and strategies disclosed as well as the statement from company leaders where more related to self-laundry than to achieve its real purpose which is to clarify the companies approach towards its stakeholder.

2.5 Transparency and Disclosure

As a result of the recent decades financial and environmental scandals, the pressure for corporate transparency and disclosure have increased. This pressure comes from stakeholders such as institutional shareholders, regulators and banks as they need to monitor the organizations in order to trust the information given (Choi & Sami, 2012). Andersson (2008) write about transparency as a word that in everyday language often have been somewhat misused and that people often believe that transparency is the exact same word as openness, which is not completely true even if they are closely related. He continues by saying that only a handful of the people have an idea of what means more to the word transparency than just openness. In order to achieve this real transparency the organization must disclose all relevant information, they must make sure that the entire market have the same possibility to get the information without any cost and the market agents as analyst and institutions must be able to analyze and to share their view of the information. This has to be done in a proper way to achieve real transparency, as transparency is the cornerstone of building trust between organizations and society.

The disclosures of the organization can take many different forms ranging from eco-labeling notices, treatment of employees to the organizations climate change related risks. By improving disclosures customers can choose between products and services that are environmental friendly or potential employees can look into the organization and see whether the values and performance of the company attracts them. Disclosures like these may lead to a competitive advantage for the organizations that manage this well (Matisoff, 2013).

There is always a trade-off for the organization when deciding on the amount and what kind of information to publicly display and whether the benefits of these disclosures exceed the costs (Choi & Sami 2012). For example, when having the stockholders interest at heart it is not uncommon that the protection of the environment will be put in second priority or

that misuse and abuse of the labor force occurs. At the same time, if having the societal interest at heart this often is at the expense of the stockholders as it cost money to take care of the environment, not using child labor or paying fair salaries to the employees (Hearit, 1995). Therefore it is important for the organizations to disclose information about their vision and strategy and how they are affecting various segments of society, especially if the organization operates in a sector that is known for releasing large amounts of pollution or violating human rights. The organizations often cope with these issues by engaging in corporate sustainability reporting to show the society that their actions are legitimate and that they are acting for the society and not against it (Hooghiemstra, 2000).

2.6 Stakeholder Theory

Stakeholders are defined as “any group or individual who can affect or is affected by the achievement of the corporation’s purpose” (Freeman, 2010, p. iii). He also states that stakeholders are any group that help or hurt the corporation. Therefor, Stakeholder theory can be described as a managerial theory that places the stakeholders in the center of attention of the organizations strategic thinking (Freeman, 2010).

The stakeholder theory can be divided in to two branches (Gray, Adams, & Owen, 2014). The first branch, called the ethical branch of stakeholder theory, that focus on the responsibility towards the whole society and all its stakeholders is based on the assumption that the organization and stakeholder relationship is constructed on a number of social interaction that affect all stakeholders and as a result the organization is accountable to the entire society (Deegan & Unerman, 2011). According to Gray et al. (1997) the theory has limited power regarding how it can help and explain the social interaction in the context of social accounting.

The second branch, called the managerial branch of stakeholder theory, which is based on which stakeholders the organization deems most important (Deegan & Unerman, 2011). Mitchell et al. (1997) gives a further understanding by saying that the more salient an organization finds a stakeholder, the more effort should be put into the particular stakeholder. They can then use the information in a more specified way to better manage the stakeholder in order to gain approval and support (Deegan & Unerman, 2011).

2.7 Legitimacy Theory

Legitimacy theory can be explained as the idea that organizations only can continue to exist and to grow if the societies, in where the organizations are conducting their business, perceive them as legitimate. It can be said that there is a social contract between the organization and the society and because of this contract the organizations perform actions that can contribute to a better society. The organizations need to disclose information regarding these actions in order for society to be able to see them as legitimate (Deegan & Unerman, 2011; Guthrie & Parker, 1989 & Gray et al., 2014). If the organizations are not successful in communicating their commitments towards society and if society feels that this social contract has been violated, the soul survival of the organization can be in jeopardy (Deegan C. , 2002).

The theory can be divided into two different sub-theories, which are the institutional legitimacy theory and the Strategic legitimacy theory (Tilling, 2010). The institutional legitimacy theory have a macro level perspective and deals with how the legitimatization of concepts as capitalism or existence of governments and how these gain acceptance from society. The strategic legitimacy theory on the other hand has an organizational perspective and focuses on the surrounding environment of the organization, or as Kaplan & Ruland (1991, p. 370) explains it: “Underlying organizational legitimacy is a process, legitimation, by which an organization seeks approval (or avoidance of sanction) from groups in society”. Here, legitimacy can be seen as a resource, just as money, that is needed for the organization to continue their operations.

Suchman (1995, p. 574) define legitimacy as “Legitimacy is a generalized perception or assumption that the actions of an entity are desirable, proper or appropriate within some socially constructed system of norms, values beliefs, and definitions”. He continues with saying that in order for society to experience the organization as legitimate the organization has to be able to prevent events that will harm their legitimacy. Lindblom (1994) have identified four legitimation strategies in order to prevent events as these: educating its stakeholders, change the stakeholders perceptions of the issue, distract (i.e. manipulate) the attention from the issue of concern or seek to change external expectations about its performance.

3 Methodology

3.1 Research strategy and approach

Bryman & Bell (2011) explain research strategy as the way that data is collected and analyzed and he explains the two major strategies to choose from, qualitative and quantitative. The terms qualitative and quantitative are a way to differentiate data, both in collection and in analysis, where the biggest difference between the two is whether the data is numerical or non-numerical. Quantitative data is mostly used if the data the researcher is collecting or analyzing generates or uses numerical data and this data often have very little meaning in its raw form. For this data to be useful it needs to be quantified which can be done with analysis techniques as charts or tables. Qualitative data, on the other hand, can be said to be when the data generates or uses non-numerical data which can been seen as understandable at the first glance but in order to be fully understood it, it has to be analyzed (Saunders, Lewis, & Thornhill, 2009).

This report will use qualitative data since the majority off the data is text based and also because it is better applicable when doing a deeper study, as the purpose of this report requires. When using this kind of data one can use both an inductive and a deductive approach where the biggest difference is whether a clear theoretical position is developed before the collection of data, deductive approach, or if the aim is to develop a theory after the data is collected, inductive approach (Saunders et al., 2009). This study has a deductive approach as it is built on the discussion of the framework that discusses relevant literature as well as theories within the subject and the guidelines of sustainability reporting.

Numerical data will also be used in this report, but as this data already have been quantified and put together in way that is easy to understand, there where no need to implement any quantitative methods in the research. This because the companies use these charts and tables as a mean to give a better understanding to what is being stated in the text sections. The analysis of the data in this report is considered secondary data analysis, which is “the analysis of data by researchers who will probably not have been involved in the collection of those data, for purposes that in all likelihood where not envisaged by those responsible

for the data collection” (Bryman, 2012, p. 312). Since the timeline of this thesis is quite narrow, performing secondary data analysis saves both time and money (Bryman, 2012). When analyzing the data a disclosure checklist was created to get an overview of the companies performance based on the indicators. An empty checklist, Table 1, can be seen below and it is based on the chosen aspects, with underlying indicators, from the GRI framework. The checklist shows what indicators the companies used each year where the boxes after the indicators will have a “Yes”, “No” or “Partially”, depending on how or if that specific indicator has been used. The checklist also covers if there has been an increase or a decrease of these indicators from the previous year. A few of the indicators have been explained by text in the sustainability report and as these indicators could not be measured with an increase or decrease these boxes have been marked with “In Text”.

Together with the checklist the content from the sustainability reports was thoroughly analyzed. However, as the reports alone did not give sufficient information to achieve the purpose of the thesis a decision was made to include information from published Table 1: Disclosure checklist -‐ Empty

independent sources such as newspapers and articles. To get an as complete picture of the companies environmental performance as possible the information from the different sources was compared in the hopes of getting an unbiased view of the companies. To give aid in the analysis weather these companies where involved with greenwashing or not Delmas & Burbano’s (2011) definitions and terms of when greenwashing occurs was used.

3.2 Studied Companies

To manage the short timeframe of the study, a non-probability sampling was conducted where the starting point of our sample selection was the usage of the GRI-framework. The convenience and necessity due to language limitations pointed the report towards sustainability reports in English only. This type of non-probability sampling is called convenience sampling and while considered the most suitable for this particular study, it limits the opportunity of making general statements about the industry as a whole while reasonable assumptions can, however, still be made (Bryman, 2012).

The companies chosen for this study are some of the largest mining companies in the world. Since a lot of reading of sustainability reports is required in order to evaluate the companies’ claims, the list has been limited to four companies. Another criteria is that the companies chosen are all conducting their reporting based on the GRI G3 framework in order to make an accurate comparability and a fair interpretation possible. The four companies in the study were all chosen after market value in order to investigate the most relevant market players in the industry.

The four companies selected are organized based on market value from highest to lowest as follows: BHP Billiton, Rio Tinto, Glencore and Vale. These are all major corporations with high incentive to have a proper sustainability approach, which gave the possibility to exclusively examine properly prepared reports. For this reason, it was deliberately sought after to only examine companies considered as large and relevant as the chosen ones. Table 2: Selected Companies

Company name: BHP Billiton Rio Tinto Glencore Vale

Market value (US$): 122.3 billion 77.1 billion 55.5 billion 27.9 billion

Initially, the study was aimed at Swedish mining companies. However, after careful consideration it was decided that the source of relevant companies for this particular study

was to slim. The same conclusion was reached after expanding to all Scandinavian countries. Ultimately, after researching the matter, it was found that in order to accomplish this paper with the best possible outcome the focus needed to be changed to a global perspective.

3.3 Data collection

The data has been collected from companies using sustainability reports based on the GRI framework and these reports have been gathered from the GRI database. Doing so enables a certainty that the reports contain the GRI indicators and provides an assurance to find the data searched for. In the reports, the Chairman´s letter and the CEO statements of the different years have been examined in order to see what their focus has been and if their vision for the future has been followed up. Furthermore, the sustainability reports have been studied, with the focus on the information under the environmental aspects, in order to locate information that could benefit the research. To achieve an understanding whether the companies have improved, a comparison between the statements and the indicators chosen have been made with the same statements and indicators from former years. Additionally to this, different media, newspapers and databases containing news articles have been examined. This was done in order to find published information regarding the companies environmental related work as the information disclosed by the companies was found, in some cases, to be insufficient or nonexistent.

Since the companies in this study have operations all around the world, direct contact with company-representatives was deemed difficult. However, because of the importance of sustainability reporting for large companies and the fact that the purpose has a stakeholder-oriented scope, it was considered reliable to trust the information provided by the sustainability reports.

3.4 Credibility check

In order to reduce the risk of ending up with false answers from analyzing false data, ensuring the credibility of the data collected is of grave importance. This can be done by inspecting the rationality and the validity (Saunders, Lewis, & Thornhill, 2009). Testing the rationality can, according to Saunders et al. (2009), be performed by asking the following three questions:

1. Will the measures yield the same results on other occasions? 2. Will similar observations be reached by other observers?

3. Is there transparency in how sense was made from the raw data?

Since the raw data exclusively consists of publicly available information in the form of released reports and statements, there is little to none room for what Saunders et al. (2009) calls participant errors where, for example, interviewees may answer differently depending on mood. Because of the fact that we merely examine these kinds of raw data, the three questions above can be answered positively without hesitation.

Additionally there is validity, which concerns if the findings are in fact what they seem to be and that conclusions are drawn with integrity (Saunders et al., 2009 & Bryman, 2012). It is important to be certain about whether or not there is clear causality between the data, the purpose we use it for and the conclusions we reach when analyzing it.

4 Findings/Empirical findings

4.1 BHP BillitonBHP Billiton is the world’s largest mining-company based on market value in 2015 (Statista, 2015). According to the their website, their purpose is to create long-term shareholder value through the discovery, acquisition, development and marketing of natural resources.

4.1.1 Information in Sustainability reports

4.1.1.1 Information in CEO-statement

Throughout the different sustainability reports in the 3 years of examining, the CEO-statements constantly focus a lot of attention towards health and safety of their workers, calling it paramount. They have a continuing goal of zero fatalities in their operations every year, which they however did not accomplish in 2012 with 3 fatalities, nor 2013 with another 3. 2014 was a fatality-free year for BHP Billiton. The CEO also reports that in 2012 they did not reach two of their health metrics. There was no reporting of health metrics in 2013 while 2014 was reported as a year with record-low amounts of injuries. When fatalities and large amounts of injuries have been reported in the CEO-statement there is regularly mentioning’s that they learned a lot from their mistakes and that these accidents have occurred despite improvements in injury trends.

When it comes to the environmental issues of BHP Billiton’s operations, the CEO-statements repeatedly explain how they continuously strive to reduce and eliminate environmentally harmful events and minimize the environmental footprint of their operations. The CEO statements mention various environmental achievements where in 2012 states that BHP Billiton failed to achieve their goals for land rehabilitation to beat the baseline of 2006; in 2013 their greenhouse gas emissions were lower than the 2006 baseline, keeping them on route for achieving the goal of staying below the baseline until 2017; in 2014 the CEO again stated that the greenhouse gas emissions stayed below the base line of 2006.

Overall there seems to be a continuously great majority of focus on health and safety towards their own opposed to environmental safety in the CEO-statements.

4.1.1.2 Information under the aspects sections

Air

BHP Billiton discusses that their operations and products are exposed to potential financial risks from regulations controlling greenhouse gas emissions and that they probably will see changes in the cost-arrangements at the operational sites with significant their greenhouse gas emission. According to BHP Billiton, all of their operations must assess and implement projects that reduce greenhouse gas emissions and they claim to have set a goal to maintain their total greenhouse gas emissions below FY2006 level, which they during the investigated time period have accomplished. They continuously discuss different ways of how they are in line with accomplishing their goals while keeping up the same or increased production by using new innovative production procedures. An example of this is their petroleum facility in Pakistan, which has optimized compression equipment to achieve lower discharge pressures, resulting in lower fuel consumption and thus reduced amounts of emissions in the air.

Waste

BHP Billiton states that a number of controls are used to handle, reduce and recycle drilling waste. They claim that their procedure for managing waste materials specifies the storage, transportation, disposal, and monitoring of the waste and contains a worker protection plan to minimize exposure.

Biodiversity

In 2013, BHP introduced new biodiversity targets. The first target focused on a core business requirement to develop land and biodiversity management plans that include controls to prevent, minimize, rehabilitate and offset impacts to biodiversity and ecosystems services. They also claim to have targets to “finance the conservation and continuing management of areas of high biodiversity and ecosystem value that are of national and international conservation significance”, where they work in an alliance with Conservation International (a leading no governmental organization). Some examples where they say they are working to preserve land are Cradle Mountain and Lake St Clair in Tasmania, Australia (11,000 hectares), the Los Rios region, Chile (50,000 hectares) and new Mexico Coal asset in the, USA.

Energy

“Efficiently using energy” is stated early when discussing BHP Billiton’s energy usage. They continuously explain their annually increasing energy usage with the increase in operations while they at the same time claim to search for new technology to constantly decrease their usage. This can be seen in the disclosure checklist.

Water

Environmental and economic values as well as expectations from stakeholders are mentioned as factors for the importance of water management. In 2014 it is explained that in order to reach sustainability within their operations it is crucial to manage water through appropriate quality/quantity and responsible/appropriate amount of usage. During 2011-2014 they developed over 500 projects to install leak monitoring and they also continued studies about water footprint. BHP discusses different risks associated with their different operational sites and how they implement quantitative water balance models to predict and support the management of water inputs, use and outputs and to enable timely management responses to water-related risks.

4.1.2 Scandals and controversies

4.1.2.1 Borneo coal mining controversy

Information in sustainability reports

Published independent information

In October 2013, BHP Billiton encountered heavy opposition from JATAM (The Indonesian Mining Advocacy Network) when they were preparing to open seven coal concessions, which together would cover 3,500 km2 of rainforest in Borneo, Indonesia.

Part of the operation is in the transnational “Heart of Borneo” conversation area, described as “The lungs of Asia” (London Mining Network, 2013). Coal mining operations in these areas were said to be disastrous for the local people as well as the environment and that it would cause health problems, pollution and human rights abuses. Among other statements, Hendrik Siregar of JATAM claimed, “BHP Billiton, backed by UK shareholders and investors, tells the world that it is resourcing the future. Local communities in Central Kalimantan are telling us that coal mining is destroying their future.” (London Mining Network, 2013)

4.1.2.2 George’s River pollution

Information in sustainability reports

There is no information in the sustainability report regarding this incident. Published independent information

In 2012, Endeavour, a BHP Billion subsidiary was accused of releasing high levels of zinc, copper, nickel, arsenic and aluminum into Brennan's Creek, which flows into the George's River south of Sidney. The water in George’s River had, among other things, been used for swimming, fishing, watering veggie patches and leisure purposes but local communities were never notified if the polluted water could have a negative impact on health (ABC News, 2012). BHP Billiton, however, rightfully claimed they had license to distribute waste in the area (ABC News, 2012). There was a long going investigation about this matter, which in April 2013 resulted in Environment Protection Authority (EPA) conducting a license variation notice, basically giving BHP continued right to dump waste and pollute the river. At the same time, however, the EPA also added to the license that BHP Billiton were required to perform a program of works to achieve 95% species protection in Brennan’s Creek and the George’s River by December 2016 with the addition of ongoing controls (EDO NSW, 2013).

4.2 Rio Tinto

Rio Tinto is the world’s second largest mining-company based on market value in 2015 (Statista, 2015). They state that they collaborate with neighboring communities to seek a sustainable improvement for climate change, water & air.

4.2.1 Information in Sustainability report

4.2.1.1 Information in Chairman’s Letter

The focus of the chairman’s letter in 2012 was to gain the financial trust back as this trust was damaged due to of a number of events within the organization. The material events were the impairment of US$14.4 billion in the beginning of the year, a discussion of the management of capital and the executive remuneration linked to board effectiveness. Because of these events the former CEO stood down and was replaced.

In 2013, the focus was on Rio Tinto’s strong financial results and the restoration of the financial trust that was lost the previous year. It also focused on health and safety for the workers as a result of the three fatalities that occurred this year. The chairman also makes the statement: “We believe earning the trust of our host communities and governments is vital in creating sustainable shareholder value” (Rio Tinto, 2014).

2014´s chairman’s letter is the first of these letter that mentions the environmental impacts of the company and it states that as society’s expectations regarding this matter is increasing they strive to create mutual value. It also mentions that environmental investors seek strength, reliability and consistency and that the company will deliver sustainable returns to shareholders. In addition to the environmental issues they mostly write about their positive results, the increase in dividends and the addition of new board members.

4.2.1.2 Information in CEO Statement

In the 2012 CEO statement the newly appointed CEO Sam Walsh writes about Rio Tinto’s safety improvements and how it, despite these improvements, were fatalities within the organization. He continues with writing about the importance of achieving zero unnecessary cost and that the focus for him as a new CEO in the coming year will be on managing the business portfolio by exploring new potential operations and letting go of the ones with little or no future. Regarding the environment, he writes about the Oyu Tolgoi

mine in Mongolia, which he mentions in the context of being a big part of Rio Tinto’s growth investments.

In 2013, the CEO put a lot of focus on the environment and that it is important to minimize the impact on the stakeholders to deliver long-term business value in order for Rio Tinto to uphold their social license to operate. Further in the statement, he mentions that they met their 5 year goal from 2008 to lower greenhouse gas emission by 10% and that new goals will be set in 2015. He further mentions safety and that Rio Tinto, despite their improvements in this area, still have much to do, that this is the focus of all employees and that nothing is more important.

In the beginning of the 2014 statement he once again talks about safety. He says that even if there has been improvement within this area there have still been fatalities, which is not acceptable in Rio Tinto’s organization. Due to this they have revised and refreshed the 2014 safety strategy. There is a small section covering environmental information where they state that their 2015 target for greenhouse gas emission that was met last year now have decreased by 18% since 2008. Moreover he writes that they have got awards related to environmental work for their sustainable development of 2014. He ends with saying that the focus for the coming year is both safety for the employees and the work for the environment and its surroundings.

4.2.1.3 Further information of interest

When creating value, one of the most important steps for Rio Tinto is to maintain their operations in the long-term and to achieve its legitimacy from society by how they handle the closedown and rehabilitation of operational sites. They mention Flambeau, Wisconsin in the USA as a former mine that is now a healthy mix of woodland, grassland and wetland. They also mention a former mineral sand mine near Punakaiki in New Zeeland which is currently being transformed into a corridor of native forest. In New Zeeland they are working with the government and voluntary organizations in order to restore the eco-system in a proper way.

Further on in the report Rio Tinto writes that during the whole value creation chain, from planning and development to operation and closure, they engage with stakeholders, as they believe that it is vital to face challenges in order to minimize the risk of operations and to

capture upcoming opportunities. They write that maintaining a good relationship with stakeholders is crucial to maintain their social license to operate and to deliver a sustainable growth.

Under the environmental section in all sustainability reports during this time period they use statements as “Wherever possible we prevent - or otherwise minimize, mitigate and remediate - harmful effects that our operations may have”.

4.2.1.4 Information under the aspects

Air

In 2008, Rio Tinto started an engine idle reduction program, a program that was completed in 2014, which helped lower greenhouse gas emissions with a great amount while simultaneously reducing money spent on fuel. Rio Tinto´s fully owned subsidiary Richards Bay Minerals also won the ”Annual National Association of Clean Air Award for Industry” in South Africa for its efforts to handle the quality of the air.

Under the Air section Rio Tinto mostly write pure facts about the specific emissions, as from where it origins and what health effects it can have. Here the greatest changes were, based on the GRI indicators, an increase in particulate matter/emissions (PM) in 2012 due to increased investment, an increase in NOx in 2013 as a result of higher fuel oil usage, of

which mostly is related to the shipping fleet, and a decrease in SOx as a result of the

divestment of a copper smelter in Palabora.

The 2008 goal to reduce greenhouse gas emissions by 10% to 2015 was met in 2013 where the reasons for the decrease of emissions were the divestments and closures of different smelters together with improved measurement in the Australian coalmines. Rio Tinto’s view on these matters and its effect on the climate change is that it is important both in maintaining their social license to operate as well as how the climate change can affect their operations.

Waste

Rio Tinto’s waste management has not been under any major changes during these years. Regarding their mineral waste, all operations must have a developed mineral waste management plan with the focus to minimize the environmental impact. They have during the years stated that the acid rock drainage is the most dangerous of the mineral waste as it

has affects that need long-term solutions. Rio Tinto is currently a member in The International Network for Acid Protection (INAP) where they promote acid rock drainage (ARD) research and control, and they state that they are constantly aim for improving the handling of ARD.

Biodiversity

The section about biodiversity start with the statement that Rio Tinto are fully aware of the impacts that their operations might have on the environment. To cope with the complexity of biodiversity in the mining sector Rio Tinto implemented a biodiversity strategy in 2013 to make all sites aware of the importance of managing the biodiversity and the related risks when dealing with this issue. If the sites prove to have a high or very high biodiversity risk they must develop an action plan in order to “help understand and minimize impacts, and, where appropriate, implement actions to achieve a net positive impact” (Rio Tinto, 2015). The stages of this action plan are to first seek to avoid damage to the biodiversity, when that is not possible, seek to minimize impact and when the operation is done, rehabilitate and try to achieve a net positive impact. In 2013, 24 of 33 high or very high sites had an action plan and in 2014 the number of sites with an action plan decreased to 21 out of 32. It was stated in 2013 that the goal is for all of them to have a biodiversity action plan ready by the end of 2015.

Rio Tinto ends with writing about a planned coalmine in Mount Pleasant, Australia. The project would operate where the surrounding area holds species that are only living in that specific area. They discuss that the biggest issue about this project is to balance the economic benefits with the social benefits the mine would provide in order to ensure the protection of the biodiversity in the long run.

Energy

Under the energy section, Rio Tinto states that the global energy and climate change challenges are best being met by companies, governments and society working together and the usage and choice of energy is a big part of the solution. They recognize the need for new and more effectiveness-enhancing energy technology and that renewable energy sources are important ingredients in coping with this issue. Rio Tinto’s view on this matter has not changed dramatically during the investigated years. They are striving for more and better use of renewable sources and they know that they need to build a portfolio of these

projects. They are looking into new commercial renewable energy projects and now have a big focus on solar technology. The decrease in energy use has been a mix of operational changes and an effect of Rio Tinto’s efficiency work at their operations. As mentioned, they are striving for sustainable energy and in 2014 75% of electricity came from renewable sources as hydro plants.

Water

As each of Rio Tinto´s sites have different challenges with water, some having water surplus and some having water scarcity, every operational site must set own ways to cope with these issues. All operation, however, focuses on minimizing water use, maximizing water recycling and to return clean water to the environment. All operations should base their water management on the group water-target and the group standard as well as meeting regulatory limits. Rio Tinto works with external parties to find which operations are in water scarce environment and 2014 around 34 % of the freshwater withdrawals were from 35 operations in water scarce areas.

In between 2012-2013 one of their group targets was to lower freshwater withdrawal by 6% and the water standard included that all operations should measure the water use and reduce impact on water sources.

In 2014, water use rose by 7% to 555 billion liters. This result is said to not truly show their work for better efficiency in water use as the increase mostly was a result of them having to manage the water surplus when mining below the groundwater table.

4.2.2 Scandals and controversies

4.2.2.1 2012 London Olympics and Bingham Canyon Mine, Utah

Information in sustainability reports

There is nothing to be found in the sustainability report regarding this issue, information that mentions the event can only be found on their webpage where Rio Tinto shortly describe what kind of metal the mine delivered for the Olympic medals.

Published independent information

One event that got Rio Tinto a lot of attention was when they where to deliver the metal for the Olympic medals to the Olympic games in London 2012. This was because the Olympics in London had the goal to be the most sustainable Olympics ever arranged, covering every aspect of the games. The critique given included thoughts related to Rio Tinto’s comment that participation in the arrangements of the games could show the world how sustainable they where. The critique was based on the thought that Rio Tinto used this as a way of providing a picture of the company as being sustainable when a lot of organizations and individuals did not share that picture, hence they got critique for greenwashing (Al Jazeera, 2012).

The mine in Utah that provided the metal for the medals faced a lawsuit for air pollution a year after the Olympics and had, according to doctors consulted in the article, polluted the air for at least five years in way equivalent to smoking 20 cigarettes a day for people in the surrounding areas. People had reacted to the statement the former CEO Tom Albanese made when they won the 2012 Olympics contract. In this statement he said, “Being ethically responsible is a thread that runs through everything we do. We aim to bring long-lasting positive change to the communities where we work, respecting human rights, bringing economic benefits and looking after the environment … we have rigorous standards for air quality, ecosystems, biodiversity, climate change, the use of energy, land and water and waste disposal“ (The Guardian, 2013).

4.2.2.2 Oyu Tolgoi copper mine, Mongolia

Information in sustainability reports

In the sustainability report Rio Tinto mentions this location but only address the deep-water aquifer they built on the site.

Published independent information

In 2013 Rio Tinto made headlines regarding their US$5 billion expansion in the Oyu Tolgoi copper mine in Mongolia. This because the mine was located in the desert and that they had not shown any plans on how they would get enough water to sustain the operations of the mine. The concerns where that the mine would take a huge part of the scarce amount of water available in the desert where the most affected group of people was

the nomads who were in great need of their wells and water holes to be filled (Global Post, 2014).

The result of Rio Tinto’s operation was that they built a deep level aquifer to avoid using the surface water but they had to redirect a river to go around the plant. Because of the redirection of the river, they had to create a new spring to deliver water to the animals where the result was that it took water from the nomads wells and greatly disrupted their routines.

4.2.2.3 Grasberg mine. West Papua, Indonesia.

Information in sustainability report

There was no information in the sustainability report regarding this incident. Published independent information

The surroundings of the Grasberg mine in West Papua has been a victim of extreme pollution. The river, coming down from the mine and the mountain, that once where crystal clear and full of fish in some places got a color similar to coffee and the surroundings where in some places similar to dessert. The inhabitants that once lived from the mountain and the river have experienced a dramatic change of their lifestyles as of this pollution (Earth Island, 2013 ). As a result of Rio Tinto being involved in this mine Norway’s government let go of all investments related to Rio Tinto as the Norwegian government did not want to have any part in such extensive environmental destruction (BBC, 2008).