Bachelor Thesis within Business Administration

Authors: Gustav Dahllöf

Erik Matsson

Julius Nilsson

Tutor: Gershon Kumeto

Jönköping May 2015

Business to Business - Electronic Invoice

Processing

A report on the challenges, solutions and outcomes for

companies switching from manual to electronic invoice handling.

Acknowledgement

We would like to thank our tutor Gershon Kumeto for his guidance and support throughout the process of writing this thesis. He has been of great value to us in regards to providing constructive criticism which have enabled us to build a solid ground for this thesis. Furthermore, we would also like to thank other students, family members and individuals for the input and criticism.

Moreover, we would like to send our special thanks and regards to the companies that have participated in our case study, without their input and valuable insight, the thesis would have been impossible for us to conduct. This also involves the input and information we received from professionals within the field, Heinz Kopfinger and Jonas Edlund.

--- --- --- Gustav Dahllöf Erik Matsson Julius Nilsson

Bachelor Thesis in Business Administration

Title: Business to Business – Electronic Invoice Processing – A report on the challenges, solutions and outcomes for companies switching to electronic invoice handling.

Authors: Gustav Dahllöf, Erik Matsson and Julius Nilsson. Tutor: Gershon Kumeto.

Date: Jönköping, May 2015.

Keywords: EDI, VAN, Electronic invoice handling, Electronic invoices, ERP, Formats, Electronic data transmission and Communication protocols.

Abstract

Electronic document handling was first used in the automotive industry in the early 1970’s, the way of communicating electronic at the time was concerned with the communication way of EDI (Hsieh, 2004). In the beginning of 2000 a new way of communicating electronic documents was introduced with the emergence of VAN-operators (Hsieh, 2004). This technology of communicating electronic invoices has shown to be less complex for the businesses than the previous EDI connections. The VAN-operators enable companies regardless of size, ERP, also known as Enterprise Resource Planning, system, formats or transaction volume to send and receive electronic invoices.

The subject of electronic invoice handling have become increasingly debated, mainly because of the legislations taking place all over Europe, and as well as the environmental impact by business transactions being sent by paper. The objective of this thesis is to examine the challenges, solutions and outcomes for companies switching to electronic invoice handling.

The data collected for the thesis is divided into two parts. The first part consist of information retrieved by previous literature as well as internet sources. The second part concerns the case studies conducted for the thesis in respect to our research questions. For this reason Scandinavian companies have been interviewed, with different precondition as in size, industry, transaction volume and IT structure.

The findings from the first and second part have been analyzed and conclusion have been made, we suggest using a VAN-operators, which have shown to be the most appropriate alternative for companies that are implementing electronic invoice handling. The result of this thesis can be used as a guideline for companies when considering a switch from manual to electronic invoice handling.

1

Table of Content

1

Introduction ... 4

1.1 Background ... 4 1.2 Problem discussion ... 5 1.3 Purpose... 7 1.4 Research questions ... 7 1.5 Interested parties ... 8 1.6 Definition of concepts ... 8 1.6.1 EDI ... 8 1.6.2 VAN ... 8 1.6.3 ERP ... 8 1.6.4 B2B ... 9 1.6.5 Languages/Formats ... 92

Theoretical framework ... 10

2.1 Solutions for electronic invoicing ... 10

2.1.1 Electronic Data Interchange ... 10

2.1.2 Value Added Network ... 12

2.1.3 Electronic Invoicing ... 14 2.2 Challenges of implementation ... 16 2.2.1 Complexity ... 16 2.2.2 Knowledge... 16 2.2.3 Integration ... 17 2.3 Outcomes of implementation ... 17 2.3.1 Cost... 17 2.3.2 Performance ... 18 2.3.3 Sustainable environment ... 18 2.4 Regulatory requirements ... 19

3

Methodology ... 21

3.1 Research approach ... 21 3.2 Research design ... 223.3 Literature and Theoretical frame ... 23

3.4 Data Collection ... 24

3.4.1 Case study approach ... 24

3.4.2 Case study design ... 24

3.4.3 Selection of companies ... 25

3.4.4 Interviews with individuals ... 26

2 3.4.4.2 Heinz Kopfinger ... 27 3.5 Quality ... 27 3.5.1 Validity ... 27 3.5.2 Reliability ... 27 3.5.3 Transferability ... 28 3.5.4 Objectivity ... 28 3.6 Delimitations ... 28

3.7 Analysis of the data ... 29

4

Empirical findings ... 30

4.1 Interviews ... 30 4.1.1 Explica entreprenad AB ... 30 4.1.1.1 Challenges ... 30 4.1.1.2 Solutions ... 30 4.1.1.3 Outcomes ... 31 4.1.2 Company X ... 31 4.1.2.1 Challenges ... 32 4.1.2.2 Solutions ... 32 4.1.2.3 Outcomes ... 32 4.1.3 Ides AB ... 33 4.1.3.1 Challenges ... 33 4.1.3.2 Solutions ... 33 4.1.3.3 Outcomes ... 33 4.1.4 Brck Dgtl Outdoor Media AB ... 34 4.1.4.1 Challenges ... 34 4.1.4.2 Solutions ... 34 4.1.4.3 Outcomes ... 345

Analysis ... 36

5.1 Challenges ... 36 5.2 Solutions ... 39 5.3 Outcomes ... 41 5.4 Summary ... 435.5 Suggestions for improvements ... 43

6

Conclusion ... 45

7

Discussion ... 47

7.1 Future research ... 488

List of references ... 49

1

Appendices ... 53

1.1 Interview template ... 533

2

Interviews ... 55

2.1 Explica Entreprenad AB ... 55 2.2 Company X ... 57 2.3 Ides AB ... 59 2.4 Brck Dgtl Outdoor Media AB ... 61Appendices

Appendix 1 Interview template. Appendix 2 Interviews. Appendix 2.2 Explica Entreprenad AB. Appendix 2.3 Company X. Appendix 2.3 Ides AB. Appendix 2.4 Brck Dgtl Outdoor Media AB.Figures

Figure 2.1 – The process of EDI, authors own illustration...8Figure 2.2 – The process of VAN, authors own illustration...10

4

1 Introduction

The introduction chapter aims to provide the reader with a general insight of the chosen topic. The background will cover different aspects, which in turn will be conduce to the problem discussion for the purpose of narrow it down to the research question guiding this thesis. It will also cover definitions of a number of key concepts that will be frequently used throughout the thesis. The chapter also covers the interest parties that we believe would benefit the most by reading the findings of our study.

1.1 Background

The subject of electronic document handling has been a debated topic over the last decades. The use of electronic data interchange of financial documents, in the context of business to business transactions, started in the automotive industry in the 1970’s, in order to increase the efficiency in the supply chain management processes (Hsieh, 2004). Over the past decades, there have been a rapidly increasing amount of organizations that use the internet as a tool in their day to day business (Raphael & Zott, 2001). During that time, the way of communicating electronically was focused on EDI, also known as Electronic Data Interchange, technology. The usage of EDI has since then increased and larger organizations have become specialized in setting up EDI-connections (Hsieh, 2004). EDI-professionals create a structure to increase the efficiency and decrease the cost of each connection as a result of specialization. As technological abilities boosted new ways of connecting organizations, in year 2000, VAN-, also known as Value Added Network, operators started to emerge (Hsieh, 2004). The VAN-operators primary objective is to minimize the boundaries and increase the enablement for companies to start transmitting data electronically with their trading partners regardless of the organizations internal abilities.

In 2008 the European Commission together with a consortium of 17 members from 11 countries: Austria, Denmark, Finland, France, Germany, Greece, Italy, Norway, Portugal, Sweden, and United Kingdom, created the Pan-European Public Procurement Online also known as PEPPOL (Peppol, 2015). The goal of the project was to simplify electronic transactions across borders in Europe and to create a technological standard that would increase efficiency in matters of connections as well as reducing costs, compared to previous methods of exchanging data between businesses in different countries. Since the introduction, an increasing number of countries have adopted the standard of PEPPOL as the country specific gateway and several countries have legislated electronic invoicing to governmental entities (Peppol, 2015). In the last years, the Scandinavian governments have started to require that their incoming invoices should be communicated electronically, according to the different national standards. All Scandinavian countries have been early adopters of electronic invoices handling and are all connected to the PEPPOL agreement (Peppol, 2015).

5

Previous research, within the field of electronic invoice handling, argue that companies can benefit by switching to electronic document handling due to the reduction of labor, since electronic handling require less manual intervention as well as lower material costs (Soliman & Janz, 2003). Another beneficial aspect is the improvement of supply chain management between the two trading partners exchanging document electronically, with increased accuracy and speed (Hill & Scudder, 2010). However, it is widely debated in literature what the actual outcomes of electronic data interchange are, stating that: different studies show significant difference in benefits for organizations that adopt EDI (Narayanan, Marucheck & Handfield, 2009). Key factors that has increased the usage of electronic invoice handling in the European market can be divided into two parts, one consisting of internal pressure, improvement of cash management and environmental sustainability. The second part concerns external factors, legislations and directives for communicating with trading partners electronically (Billentis, 2014).

Zhu, Kraemer, Gurbaxani & Sean (2005) argues that companies needs to be up-to-date with the new technologies arising, hence the usage of electronic invoice handling, as a part of the EDI processes, can be beneficial and result in advantages for companies compared to competitors that are not. The fact that the concept of electronic invoice handling within business to business transaction are up-to-date can be supported by the citation made by Gartner in 2014, an American consultant company widely recognized within the field of electronic document handling:

“Start evaluating e-invoicing project opportunities now, regardless of your company’s vertical industry or financial shape. The pressure to do some form of e-invoicing will increase, no matter where you are, or the size of your business. Sooner or later, you will face the hard deadline of a government mandate.” – (Gartner, 2014, p.13)

In order to get a cohesive and trustworthy contribution, the thesis will cover current literature within the field as well as qualitative data in the form of case studies with organization that have implemented or are in the process of implementing a system for electronic invoice handling. Argued is that the subject of electronic invoice handling have become increasingly more important in the global and complex environment that businesses are operating in (Zhu et al., 2006). Zhu et al., (2006) further argues that in order to stay competitive, one aspect is the importance of implementing a suitable form for electronic invoice handling for organizations today.

1.2 Problem discussion

Businesses and organizations are using different ERP-, also known as Enterprise Resource Planning, system to keep track on business processes such as procurement, accounting, production,

6

distribution and more (Hsieh, 2004). These systems speak different “languages” i.e. require data in different format structures in order to communicate digitally (Kaliontzoglou, Boutsi, & Polem, 2006). If companies want to achieve a touchless process for incoming electronic invoices, the invoices need to be received in the same format which can be interpreted by the recipients ERP system (Hsieh, 2004). The managerial and IT complexity within organizations can be a part of the barriers that organizations face when considering a switch to electronic invoice handling (Zhu et al., 2006). Since we believe that there can be a complexity in terms of formats and ways to communicate electronically, we will investigate and outline the obstacle that may occur when an organization want to implement or have implemented a system for electronic invoice handling. This leads up to our first research question:

What challenges, if any, are involved when switching to electronic invoice handling?

The first EDI connection was introduced in the automotive industry in the 1970’s (Hsieh, 2004). In the last 25 years EDI have become more adopted in various industries by large organizations and companies (Hazen & Byrd, 2012). The authors further argue that the globalization and spread of internet enabled small and medium enterprises to start benefit from EDI connections. In the last decade, service providers, also known as VAN-operators, have become an option for companies to enable electronic invoice handling (Hazen & Byrd, 2012). Since there seem to be a variety of possible solutions for organizations to communicate electronically, we will map the different solution on the market. Hence, the second research question:

What solutions are available to choose from when switching to electronic invoice handling?

The benefits with electronic invoice handling vary significantly in previous research and literature. Organizational improvements, such as less error management, time reduction and efficiency outcomes are some of the benefits when implementing a solution for electronic invoice handling (Sanders, 2007). Currently, literature also argue differently; even if the usage of EDI connections by organization have been operational for over 25 years, the gains for using this technology is inconclusive in literature (Ahmad & Schroeder, 2001). Some argue that the outcome, when switching to electronic document handling, is dependent on the company size and transaction volume (Narayanan, Marucheck & Handfield, 2009). Large organizations have greater possibilities to be more beneficial compared to smaller organizations, in terms of electronic communication. Smaller organizations usually have fewer transactions to process as well as less cash flow (Veselá & Radimersky 2014). Hazen & Byrd (2012) however argues that smaller organizations and corporations have become more able today, due to globalization with stakeholders all around the world, to gain the same benefits as large actors in the market. Since there are inconclusive outcomes

7

when implementing a system for electronic invoice handling, we will investigate how one can measure the gains, if any. Hence our third research question:

What outcomes are there when switching to electronic invoice handling?

The research questions have been chosen with caution to cover the different aspects, which companies can be interested in when switching to electronic invoice handling. The research questions will contribute to a clear and concise report and can be analyzed with the data received from the qualitative research, in forms of interviews with organizations that will be presented.

1.3 Purpose

The purpose of the thesis is to investigate the challenges, solutions and outcomes in respect to electronic invoice handling for businesses, and to provide the reader with a cohesive and revised report of aspects to consider when implementing a solution for electronic invoice handling. There are numerous solutions and options for organizations and corporations to choose from and different aspects to take into account, when switching to an electronic invoicing system in today’s market. We believe that this thesis is of interest for our audience, which are further described below in the section regarding interest parties. We argue that the topic is up-to-date, with the current legislations for electronic invoices throughout Scandinavia and Europe (Peppol, 2015). The aspect of the environmental impact of traditional paper invoices are furthermore a key driver for electronic invoices. We argue that there is a considerable interest by companies, regardless of size, transaction volume or industry for a study like ours, the result of the study will present different aspects organization needs to evaluate when implementing a solution for electronic invoice handling. As the previous literature is partly inconclusive in the results of having an electronic invoicing system within organizations, we argue that the purpose of the thesis is valuable today.

1.4 Research questions

The following research questions will be used for our thesis:

Research question 1: What challenges, if any, are involved when switching to electronic invoice

handling?

Research question 2: What solutions are available to choose from when switching to electronic invoice

handling?

8

1.5 Interested parties

This thesis turns to all types of organizations, regardless of size, transaction volume or ERP system. It is designed to provide a guideline for companies that are considering or are in the process of or already have implemented a solution to communicate invoices digitally. We believe that the following groups within an organization can find this information useful; IT or supply chain consultants, supply chain managers, system developers, project managers, procurement managers and e-business managers who already have some previous knowledge within the field of electronic invoicing. As we further argue, knowledge is an important aspect of electronic invoicing and it is our aim to provide our interested parties with the knowledge needed.

1.6 Definition of concepts

1.6.1 EDI

EDI, an abbreviation of Electronic Data Interchange, is a solution for communicating electronically between two server environments in or between organizations (Hoogeweegena, Streng & Wegenaar, 1998). It is used to increase the efficiency, traceability and speed when communicating information. It enables swift access to data, which moreover can be done in between different environments, both internally and externally with or within organizations and corporations (Clemons, Reddi & Row, 1993). Henceforward, the concept Electronic Data Interchange will be referred to as EDI.

1.6.2 VAN

VAN, an abbreviation of Value-Added-Network, is cloud based service that enables different methods of connecting possibilities to the platform, where the translation in-between the different formats can be performed. The VAN acts as an intermediary between different trading partners to ease the ability to interact with different business partners globally. This provides the ability for organizations to use one standardized business process for all trading partners that are connected to the platform. This way of communicating electronic data is used by organizations, regardless of size or transaction volumes, to minimize the need for internal IT competence and resources for enablement of electronic data transfer (Bailey & Bakos, 1997). Henceforward Value Added Network will be referred to as VAN.

1.6.3 ERP

ERP, an abbreviation of Enterprise Resource Planning, is a software used by organizations to manage various types of data such as inventory, shipments, manufacturing, sales, marketing, production capacity and costs. An ERP system combines different types of data into one viewable

9

business process (Klaus, Rosemann & Gable, 2000). ERP systems are commonly used among businesses globally since it is seen as a vital tool for keeping track of various functions within organizations business processes, as the ERP system stores all data centrally (Hendricks, Singhal & Stratman, 2007). An ERP has the ability to combine data from several different departments and systems within an organization, which gives the user an ability to monitor the business as a whole. (Klaus, Rosemann & Gable, 2000). Henceforward, Enterprise Resource Planning will be referred to as ERP.

1.6.4 B2B

B2B, an abbreviation of Business to Business, is referred to a trade transaction in between to organizations e.g. when a buyer organization buys products from a supplier, then a B2B transaction is accruing. Henceforward, Business to Business will be referred to as B2B (Hawkins, Pohlen & Prybutok, 2013).

1.6.5 Languages/Formats

Sending/receiving electronic data in B2B transactions requires that an organization has the ability to handle different formats (Kaliontzoglou et al., 2006). This is due to the fact that suppliers and buyers are using different ERP systems that are based on different types of programming languages such as JAVA, C++, JAKO, PHP (Kopfinger, H personal communication, 2015-04-01). The diversity of minds behind the ERP systems as well as the different programming languages has resulted in that the languages/formats from ERP system that can extract/import differs from ERP to ERP. The format structure might also differ depending on which version of an ERP system the company are using. When EDI was introduced, the communication format EDIFACT, an abbreviation of Electronic Data Interchange for Administration, Commerce and Transport, was created (Hoogeweegena, Streng & Wegenaar, 1998). In order for companies to use the EDIFACT format, their ERP system needed to build support for extracting/importing the files into their system, if not, the companies had to do the conversion of the formats by themselves outside their ERP system. As the technology has developed over time, a new format, more commonly used for importing/exporting data from/to have introduced. This format is known as XML, also known as Extensible Markup Language (Kopfinger, H personal communication, 2015-04-01). EDIFACT and XML are different formats structures that can be used to transmit data in-between business, the difference is the format syntax (Bussler, 2001). Henceforward, the structure of the information transmitted between businesses will be referred to as formats.

10

2 Theoretical framework

The chapter of theoretical framework will include theoretical discussions and a presentation of previous literature in a conceptual framework. It will cover the parts that are of interest for our research questions and analysis: EDI, VAN-networks and electronic invoice handling. Thereafter the chapter will cover aspects in regards to consideration of implementation, including drivers of implementation such as cost, performance and regulatory requirements, concerning corporations based on previous literature and interviews.

2.1 Solutions for electronic invoicing

2.1.1 Electronic Data Interchange

In the past four decades, EDI, as a way of communicate electronically have become an increasing part of the supply chain and procurement departments within large organizations (Narayanan, Marucheck & Handfield, 2009). EDI as a point to point or computer to computer way of communicating B2B transactions electronically is one of the most used tools for electronic data exchange. EDI has become an increasingly crucial part within some organizations, as it is used as a platform to communicate and exchange data with suppliers, distributors, manufacturers and other trading partners (Ahmad & Shroeder, 2001).

Global corporations with trading partners around the world could, with the help of EDI, exchange business documents in a faster and more secure manner. EDI enabled companies to have a unique traceability by sending the documents electronically, which enabled safer business relations. With the development of internet and computer usage the numbers of corporations using EDI increased and the knowledge of EDI was spread so that organizations had the possibility to be more beneficial in establishing these connections (Zhu et al., 2006).

Issues with EDI connections later occurred regarding the formats and protocols which complicated the setup and administration for companies and organizations. EDI connections are a point to point solution, where the two trading partners need to agree on certain formats and protocols in order to communicate. (Ratnasingam, Gefen & Pavlou, 2005). Ratnasingam et al., (2005) further argues that once a new setup is occurring, the same procedure has to be made once again, with the agreement and development of certain formats and adjustments in order to have a functioning EDI connection.

EDI has the possibility to reduce manual handling as well as limit inventory levels, turnaround level and increase productivity within organizations. Argued is that the benefits of EDI can be overseen by the actual cost of implementing the system. The aspects one needs to consider are if the company has appropriate hardware or software and knowledge within the organization. It is further argued that the decision to implement EDI needs to be made mutually by the two trading partners,

11

since both trading partners need to agree on several parameters for it to work (Saunders & Clark, 1992).

Companies adopting EDI as their way of communicating electronically needs to take into account that their existing system can be modified in order to support the EDI setup. The internal system of each company should have an accessible interface that supports different program languages, in order to make it easier for the user. Secondly, the trading partners need to agree on format standard and how they should translate data between each other. Since, organizations must translate and convert documents to different formats in order to use them properly in the organization (Massetti & Zmud, 1996). The communication protocol also needs to take into account the possibility for the users to maintain the daily work, such as tracing and providing the audit log and provide secure access (Janssen & Cuyvers, 1991).

The technology of EDI requires a project based setup and is suitable for trading partners with high transaction volumes. In order to have an efficient setup of EDI connections, the companies should have their own IT department that has previous knowledge within the field. The setup of a new EDI connection can, if new formats and communication protocols are complex, be time consuming and costly. Frequently used communication protocols for EDI connections include AS2, SFTP and FTP which is used to transport data securely. (Kopfinger, H personal communication, 2015-04-01). Kopfinger further argues that the possibilities of EDI connections are not limited to invoices, but the trading partners need to agree on the format structure on all document types. The formats on the document types can vary and can result in a greater workload (Kopfinger, H personal communication, 2015-04-01). Further on, Massetti and Zmud (1996) argue that there is a large variety of documents types that can be sent through an EDI connection, and is seen as complex and important aspect in the organization.

12

Figure 2.1 – The process of EDI, authors own illustration

Explanation of figure 2.1: Company A creates an invoice in their ERP system, the invoice format is then sent to the “EDI Translator” in order to convert the format into the agreed format between the two business partners “Company A” and “Company B”. The invoice, the EDI data, is then sent via the communication software to “Company B”. The communication setup is called EDI and is a way of transmitting electronic documents, usually an AS2 or any other secure internet protocols. Same process goes for “Company B”; once the data is received, an “EDI Translator” is needed to convert the “EDI Data” to the recipients own format in order for “Company B” to read the invoice in their system (Kopfinger, H personal communication, 2015-04-01).

2.1.2 Value Added Network

VANs are provided by third party partners that take on the responsibility of delivering electronic documents between organizations. When corporations and organization invest in a solution to communicate digitally via a VAN-operator, the technical knowledge and skills of transferring electronic documents does not have to be developed in-house. Therefore, VAN-operators used to be described as an alternative when an organization was not able to cope with the complexity of sending electronic documents (Massetti & Zmud, 1996). The VANs acts as an intermediary, between different trading partners to ease the ability to interact with one another. This provides the ability for organizations to use one standardized business process for all trading partners that are connected to the platform. VAN-operators generally promote interoperability agreements, in order for companies to use one service provider instead of several, when exchanging electronic documents. This enables companies to no longer have to be concerned about the different formats

Communication software Communication software

EDI Data Internal format

EDI Data Internal format

Point to Point Communication (EDI)

Company A Company B

EDI

13

and communication protocols when sending electronic messages (Ratnasingam, Gefen & Pavlou, 2005), which is further argued to improve the benefits of using a VAN-network. Moreover, Massetti and Zmud (1996) argue that VAN-operators were established in order to help organizations cope with the challenges of sending electronic documents.

Ratnasingam et al (2005) argue that the use of VAN-networks are likely to improve the institutional trust, which is described as the relationship between companies, viewed as a central part of an organization when managing a business successfully. The authors further argue that the trust and security for corporations and organizations are improved when using VAN-networks in comparison of communicating through traditional paper usage.

VAN-operators are providing a scalable solution, with a vast amount of different ways to connect to the network. The structures of VAN-operators are to offer companies a many to many solution, which results in that trading partners, regardless of size and volume, have the possibility to send and receive electronic invoices. The formats are managed by the VAN-operator and are instantly available and beneficial for all trading partners in the network. A lot of the VAN-operators also have interoperability agreements which enable companies to send and receive electronic invoices from other VAN-networks using their chosen VAN-operator (Edlund, J, personal communication, 2015-03-16).

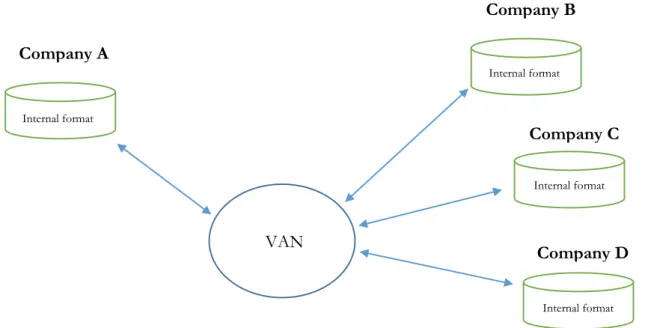

Figure 2.2 – The process of VAN, authors own illustration

Explanation of figure 2.2: Company A creates an invoice in their internal format. The invoice is then distributed to the VAN-operator, using a communication way, such as a virtual printer, SFTP, FTP or AS2. The invoice is then converted to Company A’s trading partners “Company B/C/D” formats. Company A make one connection to the VAN-operator and has, thereafter, the possibility

Company A Company B Internal format Internal format VAN Company C Company D Internal format Internal format

14

to reach all trading partners connected to the network structure (Edlund, J, personal communication, 2015-03-16).

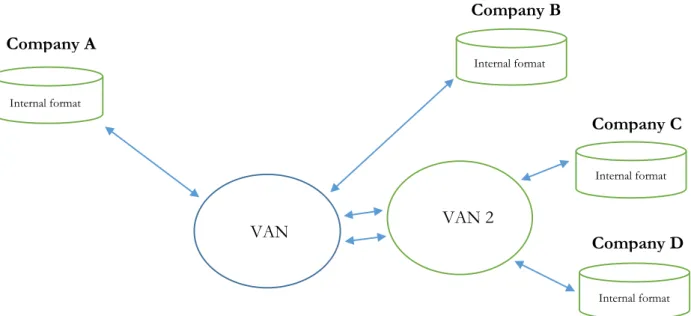

Figure 2.3 – The process of VAN interoperability, authors own illustration

Explanation of figure 2.3: Company A creates an invoice in their internal format. The invoice is then distributed to the VAN, using a communication way such as virtual printer, SFTP, FTP or AS2. The invoice is then distributed from the VAN-operator to the trading partners, as “Company B/D” is using another VAN-operator, an interoperability agreement between the VAN-operators enabling them to exchange invoices. This enables Company A to use one channel regardless of whether their trading partners are connected to other VAN-operators or not (Edlund, J, personal communication, 2015-03-16).

The VAN-operator’s architecture is often built on the concept of SOA, also known as Service Orientated Architecture, which implies that their platform is viable for others to use via the internet. The VAN-operators’ architecture is usually not limited to any business message. The structure consists of an open network approach, with public recipient and sender registers accessible through web services (Brun & Lanng, 2006). The communication setup take approximately five days and do not require any standard format because it is based on a new technology, compared to the traditional EDI setups. The VAN-operator works as a “translator hub” for the trading partners and the companies using this way of communicating only have one connection to maintain (Pramatari, 2007).

2.1.3 Electronic Invoicing

There are numerous ways of distributing/receiving electronic invoices also how corporation and organizations choose to exchange these documents. It has been widely debated among organization

Company A Company B Internal format VAN Company C Company D Internal format Internal format VAN 2 Internal format

15

and institutes what should be regarded as a true electronic invoice (Edlund, J, personal communication, 2015-03-16). Distributing an invoice via e-mail, with an attached PDF-file representing the invoice is not regarded as a true electronic invoice. Nevertheless, to do so is common among organizations today. However this is not preferable since it requires a manual handling of the invoice due to it cannot be automatically processed for importation to the ERP system (Veselá & Radimersky, 2014). Both the distributer and the receiver of the invoices will need to use manual interventions to fulfil the transactions. The distributing party will have to export the content from the ERP system and attach it to an e-mail prior to distribution. The receiving party needs to either manually enter the content of the invoice into the ERP system, or alternatively use the process of printing the PDF-file and then scan the content in order to receive a file that can be imported into the organizations ERP system (Edlund, J, personal communication, 2015-03-16). Today, many corporations and organizations handle all, or parts of, their inbounding or out bounding invoices manually in their supply chain and procurement processes. This is considered to be a loss of efficiency and moreover, a more costly process compared to having a system that allow invoices to be digital throughout the entire process, from the step of distributing to receiving the invoice (Zhu et al., 2006). As long as there needs to be manual interventions, such in the event of a PDF distributed invoice via email, it is not regarded as a true electronic invoice (Edlund, J, personal communication, 2015-03-16).

A true electronic invoice needs to be electronic from wall to wall. The exported file from the sender party needs to be imported by the recipient, this can be achieved through the usage of EDI or VAN solutions. By using EDI or VANs, no manual intervention needs to be added in-between and it is therefore regarded as the full electronic way to distribution information and therefore also electronic invoices. However, although there is an increasing amount of corporations and organizations that handle their invoices electronically through EDI and VAN connections, it remains a problem that all cannot be handled electronically since all organizations are connected to though EDI or VAN-operations, therefore invoices need to be handled manually as well (Edlund, J, personal communication, 2015-03-16).

The most common issue is that companies are not sending fully automated electronic invoices. Instead, as mentioned earlier, they send a PDF as an attachment in an e-mail (Edlund, J, personal communication, 2015-03-16). Furthermore, this is an inefficient and unsustainable way of handling invoices since there are solutions that easily allow invoices to be efficient to organizations. It is argued that using EDI to distribute electronic invoices between corporations and organizations is one way of increasing the economic value and a vital decision to prepare for the future of invoicing

16

within and in between organizations (Narayanan, Marucheck & Handfield, 2009). When sending an invoice electronically via EDI or a VAN-network, the invoice can contain a digital signature which increases the credibility and integrity of the invoice. It can also be richer in content compared to paper invoices that the software can read and log for the future (Kaliontzoglou et al., 2006). The system creates the invoice digitally, sends it in required format via EDI or a VAN-network and the invoice is thereafter received by the recipients system and handled automatically and fully digitally. This is mainly done and used by large corporations today with more than 250 employees (Veselá & Radimersky, 2014), it is argued that these companies have the ability to benefit the most by having an automated electronic invoice handling, since companies with high transaction volume can save significant amount of money and resources by handling their invoices electronically. Smaller organization, with less transaction volumes, generally feel that they lack administrative resources and knowledge (Karjalainen & Kemppainen, 2008).

Widely argued is the fact that an electronic invoice can be distributed in an efficient and secure way, which can minimize manual handling and provide traceability. It is further stated that electronic invoice handling can be more beneficial for large corporations, as previously stated, since it can improve control of the economic situation it is easy to track with the receipt handling, providing a unique traceability, something that is more difficult when sending paper invoices (Sammon & Hanley, 2007).

2.2 Challenges of implementation

2.2.1 Complexity

The technical complexity can be a barrier for companies when they consider implementing a solution for electronic document handling. EDI standards and setups are often complex and time consuming for companies which have no prior knowledge about EDI setups in their organization and it is argued that maintenance of EDI connections requires certain technical skills (Zhu et al., 2006). Edlund argues that that the technical complexity that organizations face with EDI is not present when connecting to a VAN-network. Further, VAN-operators have scalable solutions which can be customized according to the technical needs of the organizations. VAN-networks share the same benefits as EDI in respect to electronic document handling but offer an easier solution for companies (Edlund, J, personal communication, 2015-03-16).

2.2.2 Knowledge

Knowledge of electronic invoicing is one important aspect to consider when implementing a solution that enables electronic invoicing (Hong & Kim, 2002). The knowledge need to cover

17

technical and basic aspects on how to cooperate with systems which enable electronic invoice handling in an organization in order to benefit from. The knowledge inside organizations needs to cover aspects such as organizational and IT structure (Hazen & Byrd, 2012). Having an IT-infrastructure that is well functioning and connected with partners is an important aspect for organizations to be beneficial from e-procurements. This includes having a system that handles electronic invoices with the knowledge in-house or in the case of a VAN-operator where the knowledge can be outsourced (Ratnasingam et al., 2005). Ratnasingam, et al., (2005) further argue that institutional trust is an essential aspect of being successful and without knowledge within the organization, the institutional trust is affected negatively. This aspect is necessary in order to maintain good relationships within the organization and also with stakeholders such as partners, customers and clients. Hazen & Byrd (2012), stresses that the understanding of the issue is crucial to be successful with the adoption of e-procurements in the long run.

2.2.3 Integration

The integration can be achieved through regular EDI or by connecting to a VAN-network, which enables companies to send and receive electronic invoices. It is crucial for corporations when implementing an electronic invoicing system, to do it successfully and lean. Firms that are stuck in an old system and refuse to update due to any reason, runs the risk of losing their possible competitive advantage towards others (Zhu et al., 2006). The integration part is more described in the section of 2.1.1 EDI and 2.1.2 VAN.

2.3 Outcomes of implementation

The usage of electronic invoicing is becoming a more common occurrence in all types of businesses, and there are several strong forces that drive corporations and organizations to implement a system that can enable electronic invoicing. Current literature lists several crucial forces to why corporations implement a system, but the literature is inconclusive regarding why some corporations and organizations benefit more than others in regard to switching to electronic invoice handling (Ahmad & Schroeder, 2001).

2.3.1 Cost

The cost aspect is an important part for organizations when considering switching to electronic document handling and it is argued that organizations can reduce the cost per invoice with as much as 60-80%, compared to if organizations would send/receive paper invoices (Veselá & Radimersky, 2014). It is further argued that the ROI, also known as Return of Investment, period for switching to electronic invoice handling is 0,5-1,5 years (Billentis, 2009).

18

Implementing cost is a significant barrier to cross for companies when considering implementing a system for electronic invoice handling. Further argued is that companies need to consider the implementation costs in relation to the current cost with higher manual handling and material cost. In the long run, the investment in a system, which enables electronic invoice handling is likely to pay off, as there are significant savings to be made: time as in labor cost as well as material cost such as the cost of paper, ink, envelops and stamps (Zhu et al., 2006).

Electronic invoice handling can also generate cost savings with respect to improved business processes: minimization in error and labor time spent on invoice handling. This generates a more efficient use of human resources; time previously spent on invoice handling can now be used for more value-generating activities (Veselá & Radimersky, 2014).

2.3.2 Performance

The aspects of performance related to switching to electronic document handling are widely debated in existing literature. One aspect is that electronic invoice handling improves performance in terms of faster processing, less error management and faster approval cycles (Veselá & Radimersky, 2014). Electronic invoice handling also provides a financial security for organizations, because of the traceability an electronic invoice provide compared to the postal delays and disappearance of paper invoices. (Haq, 2007, Berez & Sheth, 2007).

Electronic invoices also offers e-procurement the opportunity to decentralize some parts of the operational management processes within an organization. This provides the opportunity to focus on the central parts of the strategic and management procedures. As a result it provides a better control of the administrative routines, electronic invoices provides better traceability and storage in a digital system that does not demand daily and manual control by organizations (Puschmann & Alt, 2005). Implications of electronic market places suggest that organizations change their strategy, leading to that organizations are able to increase the efficiency of the business (Yannis, 1991). The complexity of documents exchange in-house is high and can be seen as risk factor. Organizations that establish a system need to plan the management and strategy well in order for the organization to cope successfully (Truman, 2000).

2.3.3 Sustainable environment

Traditional paper invoices require material and transportation in order to be delivered to the recipient, this handling can be argued to be unsustainable in terms of the environment. The benefits for the environment are directly connected to the decrease in paper and printing from the previous manual invoicing handling (Moberg, Borggren, Finnveden, Tyskeng, 2010). Every invoice causes

19

approximately 0.029 kg Co2 pollution (SEB, 2015). The stated number of pollution is just for the creation of the paper, the printing and an envelope and does not contain the pollution statistic for the transportation which contributes to the largest part of pollution in terms of manual invoice handling. However, the electronic invoice has no Co2 pollution and only requires electricity which is more sustainable in the long run for the global environment (Kloch, Petersen & Madsen, 2011).

2.4 Regulatory requirements

In a global perspective, there is much to be gained when businesses are switching to electronic invoice system, since it provides a more sustainable society and is environmental friendly. As a result, governments have introduced legislations and requirements for organizations and corporations on how to send electronic invoices (Riksdagen, 2015). The directive for PEPPOL from the European Commission is to mandate electronic invoicing and forbid paper invoices by law in 2018 (Peppol, 2015). In this thesis, we have focused on the Scandinavian market and their status and standardization for electronic invoicing.

In Scandinavia, invoice handling has during the latest years been regulated in the sense that all invoices that are received by the government need to be electronic. Sweden proposed the standard in 2003 by a law and legislated it in 2012 and have been under progress since, this is now the standard in Sweden (Riksdagen, 2015). However, the Scandinavian countries all have their own standardization system on electronic invoices but have all agreed to follow standards as for the European Commission (Peppol, 2015).

PEPPOL is an initiative by the European Commission to reach standards for e-procurements. This origins from the European Union’s directive in the early 2000’s which desired a more homogenous market for invoices throughout the member states (Kaliontzoglou et al., 2006). It is designed to be a standard to transmit business information where the system is connected to all local systems and function no matter the local legislation and standardization in each country within European Union (Kloch et al., 2011). The members of PEPPOL are growing annually, even with countries outside the boarders of the European commission (Peppol, 2015).

The local standards in Scandinavia vary; in Denmark the standard is called Nemhandel, in Norway it is called PEPPOL and in Sweden the standardization is called STFI. Nemhandel works in similar way as PEPPOL and is designed to connect business partners through a system and is demanded by law in both countries for VAN-operators to be connected and working with when conducting business with the public sector in Denmark (Nemhandel, 2015). The experiences and outcomes of

20

Nemhandel have laid ground to much of the content in PEPPOL protocols, since Denmark was one of the pioneers within legislated e-invoicing (Kloch et al., 2011).

Norway got assigned the task from the European Commission to design and create PEPPOL and has the PEPPOL agreement as a standard with Difi, an agency for eGovernment in Norway. The e-procurement infrastructure has PEPPOL as a standard and Norway has a high degree of compatibility regarding e-invoicing, with national and international business partners. The government have started introduced demands for their partners that they need to send invoices electronically in a specific format. It has been a national implementation with more than 30 000 companies that are using the same standard and connected to PEPPOL (Peppol, 2015).

In Sweden, the standard is called SFTI, an abbreviation to Single Face To Industry, and is closely connected to PEPPOL. SFTI is a government owned agency for the public sector that handles the standardization and verification of electronic invoicing (STFI, 2015). The format “Svefaktura” was established in the early 2000 and SFTI demanded that public institutions were to be able to receive electronic invoices by the year 2005. It was designed to work with standardized systems used in the Scandinavian countries (STFI, 2015). SFTI recommends Swedish service providers to use PEPPOL as a standard for electronic invoices and other electronic documents. The goals for SFTI is to set PEPPOL as a standard to facilitate the documents of e-procurements in one system, increase the involvement of e-invoicing within both public and private sectors and to help organizations and corporations to overcome barriers of electronic invoicing which, according to the European commission, is an issue today (Peppol, 2015).

21

3 Methodology

The chapter includes descriptions of how the research have been conducted. The chapter starts with the research approach and design, concerning how the thesis has been constructed throughout the process. Thereafter, the data collection process is described. The section covers the theoretical frame and literature review, the case study approach and design including information and descriptions of the personal interviews with professionals within the subject of electronic invoicing. The chapter ends with the quality section, delimitations of the research and descriptions of how the data conducted has been analyzed.

3.1 Research approach

A method is the design and approach used as a tool to attain the research results and goals. The method is chosen in respect to the problem addressed and challenges of the academic work, research questions or desired result. The content within the research is crucial to be able to create a solid ground in order to analyze it and choose the most suitable and preferable research approach (Hsieh & Shannon, 2005). To fulfill the research, a philosophy approach needs to be chosen. The philosophy is the underlying assumption of the general view from the researcher’s point of view, which furthermore inspire and affect the research and the result (Saunders et al., 2009).

There are three approaches when conducting research: inductive, deductive and abductive (Saunders et al., 2012). The deductive approach is commonly when doing research on existing theory and on different hypothesis testing, which is often used in scientific researches. The inductive approach is more flexible and suitable for smaller samples where one can make theory out of the result from the analysis based on the research question (Saunders et al., 2007). The abductive approach starts with a theory and from that, conclusions that follows the theory are made from an observation. Alternatively, an observation is achieved and from that, develops a theory. The research form in this thesis is an inductive approach; we argue that this is most suitable since no hypothesis testing will be made. This method is beneficial when making conclusions from statements in a qualitative study, (Saunders et al., 2012) and therefore the preferable alternative for this study.

Within social research there are two main large philosophies, interpretivism and positivism (Ritchie & Lewis, 2003). Interpretivism is the more recent of the two major philosophies (Saunders et al., 2009). It deals with differences among people in the social society and integrates the human interest and understanding of the society. Positivism regards facts and information from individuals in order to pursue a quantitative research with statistical analysis that answers research questions and is considered to be a more complex procedure in many research situations compared to interpretivism (Saunders et al., 2007).

22

We argue that the preferred philosophy for this thesis is interpretivism. Hence, the interpretivist research philosophy has been chosen for this study. Because, in a qualitative research approach, it is crucial to discover, understand and analyze patterns of the result (Hsieh & Shannon, 2005) and concerns the soft data, which is gathered from the case study. The research questions of our study are not regulated by different hypothesis testing; instead they are focused and designed to discover patterns of challenges and possibilities in order to come to a conclusion of what aspects companies should take into account when implementing a system that enables electronic invoice handling. The interpretivism approach suggests understanding of details compared to positivism that is strongly focused on hypothesis testing and forecasting (Ritchie & Lewis, 2003), which further argues for an interpretivist approach to be applied to this study.

Therefore, we argue that the philosophy of interpretivism is the best choice for us since we have based our theory and come to conclusions from the case study result and analysis. As we have applied the interpretivism as a philosophy on this qualitative study, theory has constantly been developed throughout the research process, which we argue is important for us in order to contribute from this study and give directions for future research.

In this process, it is crucial to formulate the research questions that are to be answered. This is done by selecting a sample of the research to be analyzed, outline the process, implement and fulfill the approach and analyze the data and literature in respect to their trustworthiness (Hsieh & Shannon, 2005).

3.2 Research design

The method chosen is to combine an inductive analysis of existing literature and a qualitative research method achieved by case studies in the forms of interviews. The concept behind an inductive approach is that theory is a result of different observations (Saunders et al., 2007), which is suitable for a qualitative research design. The background to this thesis is to map the possible challenges, benefits and outcomes for companies implementing a solution for electronic invoice handling. We therefore see that the inductive research method as the best and most rational choice for this thesis combined with qualitative research. According to Saunders et al (2007), as a result of our case studies we obtain primary data, which will be analyzed to form conclusions.

With the qualitative research design and methods, we intend to achieve a greater and deeper understanding for the issue addressed, which gives the opportunity to expand and improve the topic. In general, qualitative research design consists of words and images, compared to quantitative research design that consists of numbers and hypothesis testing (Denscombe, 2007). One crucial

23

aspect of qualitative research and main purpose is to use examples that can contribute to conclusions for the research (Hsieh & Shannon, 2005). It is important to compare and analyze the trustworthiness of the qualitative data that is gathered and to compare results with respect to the individual. Since the data is possibly affected by the personal beliefs and ideas of the individuals a part of the case study, we will do our outmost to neglect and set aside our personal beliefs and ideas to ensure the quality and accuracy of the paper. However, as we see it, the inductive approach and a qualitative case study is the superior method for us to use throughout the thesis. The qualitative method regards emotions and impressions of individuals of how individuals interpret the subject (Denscompe, 2007). Therefore it was preferable for us to use this approach when we gathered the data as we have had interviews at different times and at different places.

Four corporations of different size and in different stages of the implementation process have been the interviewed, in order to answer our interview questions based on different experience, this is the foundation of qualitative data collection. The qualitative method with an inductive approach has therefore been a good tool when analyzing and presenting the data in this study. Analyzing the data from the case study with the qualitative research method with the inductive approach has been suitable when building theory and conclusions as according to Saunders et al. (2012), Saunders et al., (2012) further argues that the authors needs to understand the values and emotions of the participants of the study. The empirical data is the center of the research process, and furthermore, it contributes to the development of a theory that is trustworthy and testable. Moreover, the inductive approach on the study is useful when studying the “how”, which has been beneficial for us to investigate when answering our research questions in this study (Saunders et al., 2009).

3.3 Literature and Theoretical frame

In order to get a good overview of the subject we will use different databases to obtain information, such as: Scopus, Wiley, Jönköping University Library Database and Google Scholar. These databases will be used in order to find literature with many citations, peer reviewed and from trustworthy publishers, which can be a suggestion that the information found is accurate. Credibility and trustworthiness can be argued by reliability of the author(s), peer debriefing, engagement, persistent observations and analysis (Hsieh & Shannon, 2007).

In order to find suitable literature and research data, the following keywords will be used when searching for information: “EDI”, “VAN”, “Electronic invoice handling, “Electronic invoice, “ERP,

24

In order to get a good overview that cover all aspects that want to investigate, we will cover the following areas in our interviews; background, implementation process and the outcome when implementing an electronic invoicing system. The questions that will be asked concerned our research questions, identifying the challenges, options and possible benefits or negative aspects regarding the implementation and the outcome of electronic invoice handling within the corporations. We will divide companies in two segments; the first segment consist of companies that have implemented an electronic invoice handling prior to our thesis. The second segment consist of companies that are in the process of switching to electronic invoice handling.

3.4 Data Collection

3.4.1 Case study approach

When conducting a case study, the first approach is to choose the topic of research and form questions for the sample to answer, by the involved companies or individuals that have been chosen by different characteristics or randomly. The data collection is done by doing interviews and/or observations and/or surveys. A case study approach in a study can highlight smaller events (Denscombe, 2012), which is preferable in this study compared to a wider scope. We will choose a selection process that involves a clear set of companies that are in the process or have a solution that enable electronic invoice handling. We received the data from the case study by interviewing the companies that we have chosen. The interviews will be held by at least two persons: it is argued that this approach enables the interview to be viewed from different perspectives and provides richness to the data (Eisenhardt, 1989). The author further states that the interview group can consist of one person handling the interview questions and the other person will be observing and taking notes during the interview (Eisenhardt, 1989). The outcome of the interviews will be summarized when presented in this thesis, not be presented as an unedited version, as the summarized method is argued to be more efficient (Dahlqvist, 2003).

When considering a case study, the focus is an important aspect, what focus one has in respect to the questions asked (Baxter & Jack, 2008). In our case we will focus on the processes and people involved in the electronic invoice handling at the companies.

3.4.2 Case study design

The design of the case study will be a multiple, exploratory case study. The results from the case studies differ as the companies are in different phases regarding electronic invoicing. However, to do a single case study is likely to question the trustworthiness of the study (Yin, 2009). Therefore,

25

this study benefits more from a multiple case study including four different companies, as this increases quality.

The interviews for the case study that will be conducted for our thesis will be limited to companies that are in the process or already have implemented a solution that enables electronic invoice handling. When these requirements are met, the following interview guide (appendix 1.1) will be used. It is important to treat the companies as one connected group and not to sample completely randomly (Kumar, 2011). We argue that this case study will fulfill these requirements.

In the beginning of the interview, the following information will be noted:

Name of the person being interviewed

Organization/Company name

Position within the organization

Place

Date

The interview guide, which will be used during the interviews, will be focused on answering the research questions stated in the section 1.4, “Research questions”. The outline of the interview guide can be found in Appendix 1. All companies and individual from the company that have been interviewed, has been informed about anonymity and confidentiality. They have been informed in advance about the different aspects of the case study in order to give trustworthy and correct information (Saunders et al., 2012). One company and an individual chose to be anonymous, hence that company is called “Company X” and the individual from Company X that has been interviewed has the fictitious name “Jan Svensson”. The interviews have been conducted in the native language of the person interviewed and have been translated with caution in order to not miss any important part of information from the case studies. After the interview, the answers, given by the respondent, were compiled and then sent via email to the person being interviewed for approval. We offered them the possibility to correct any misconceptions.

3.4.3 Selection of companies

Since we wanted to cover companies in different industries that had different pre-conditions the following process was applied when choosing companies that were to be interviewed. A list of 100 companies within the Scandinavian market, consisting of companies we previously worked with or heard about, was created. The companies were then divided into ten different categories depending on which industry vertical they operated in. The ten categories consisted of: Construction,

26

Technology, Retail, Media, Automotive, Energy, Food and Beverage, Healthcare, Banking, Transportation and Engineering. We then contacted two companies within each industry we identified and asked for the possibility to make an interview. As a result, four companies agreed on being interviewed for this thesis. The companies that were interviewed were all operating in different industries which enabled us to provide with a more general, and not industry specific, insight in respect to electronic invoice handling.

3.4.4 Interviews with individuals

The interviews with Heinz Kopfinger and Jonas Edlund that have been conducted are used to get an enhanced perspective with respect to our research area. The persons interviewed were chosen to provide a second alternative to literature. The interviewed persons have several years of experience within information technology and electronic document handling. They have different experience as regards the solutions enabling electronic invoice handling; Kopfinger as a previous specialist in EDI connections and Edlund working at a VAN company. Each interview was based on a structure concerning only their background of electronic invoicing, leaving more personal questions aside. From this, we reached a higher level of understanding of the technical aspects of electronic invoicing today and how it affects companies working with it. It gave us the opportunity to get a wider scope and a deeper knowledge which we agree, enhances the quality of this study. It is crucial to minimize possible harm and misunderstandings when conducting primary data (Saunders et al., 2012). Therefore, the interviewees were informed about the topic in advance in order to be able to prepare accurate answers. They were informed about the usage of the data and that their names had been used, which none of the interviewees considered an issue. In order to secure the individuals in regard to the information they gave us the interviewees were given anonymity by the ethical codes of informed consent. (Saunders et al., 2012).The interviews of individuals were conducted in Swedish and the information has, with caution, been translated into English.

3.4.4.1 Jonas Edlund

Jonas Edlund has been interviewed, mainly to provide us with a better understanding of the VAN-operators currently present on the market. Jonas Edlund currently holds the position of Chief Marketing Officer at Pagero AB. Pagero is a service provider that has been operating within the field of electronic invoice handling since 2006. Jonas Edlund previous engagement includes CEO of two IT companies; Vendimo AB and Diamo AB during 1990-2004.

Jonas also holds a master degree from Chalmers University of Technology, Gothenburg, Sweden within the field of Computer Science & Engineering.

27 3.4.4.2 Heinz Kopfinger

Heinz Kopfinger has been interviewed, in order for us to understand the usage of ERP and EDI connections. Heinz is the co-founder and previous Chief Technology Officer at IFS. IFS was founded in 1983 and is one of the largest ERP systems in the world. Heinz has a broad and extensive knowledge within the field of ERP as well as EDI connections.

Heinz also holds a master degree from The Institute of Technology at Linköping University, Linköping, Sweden within the field of Economic Engineering, with a major in Data Information.

3.5 Quality

For this research to be trustworthy, the quality of the analyzed existing literature and the case study must be high. Reducing the number of possibilities to be wrong or uncertain is crucial and it is therefore of great interest that all research is credible and valid and in that sense, of high quality (Saunders et al., 2007). It is important that the questions of the case study are correct and leave no room for misunderstandings or interpretations. Furthermore, to be certain of the quality, all corporations that are being involved in the case study, a mail will be sent of similar question, meaning that they are aware of the topic and have thought about it. All the case studies and interviews will also be recorded to enhance the trustworthiness of our analysis of the answers given.

3.5.1 Validity

The validity of data that is obtained by the case study interview is affected by the personal opinion of the respondent. One must take into account that the respondent can choose to respond to the questions in a specific way. There is also the possibility of there being internal conflicts regarding sensitive information, which can determine the responses (Saunders et al., 2007). We therefore borne this in mind when conducting the interviews in order to keep a high quality and validity for the data collected with the interviews.

3.5.2 Reliability

According to Saunders et al. (2007) there are complications with reliability that one should be aware of when handling research. The context in which a study is done have great impact on the result and awareness of that is needed in order to be able to analyze the results/outcomes of the research made in a professional way (Hsieh & Shannon, 2005). Moreover, there are a few steps and checkpoints one can use to measure the reliability of the research and the analysis;

Another research of the same subject should be able to reach the same results

28

The room for errors should be minimized

(Hsieh & Shannon, 2005)

3.5.3 Transferability

When investigating the degree of transferability it is necessary to decide whether or not the study could be made somewhere else and in another case (Denscombe, 2008). We see that legislation of electronic invoicing is being developed all throughout Europe but with different paragraphs and descriptions. Therefore, we argue that this study could be achieved in another country in Europe with a low psychic distance and still reach similar results. We argue that the findings are likely have taken effect all through Europe, however as different countries has reached different stages of development, we believe that it is likely to take place during a time interval of several years. Further on, we argue that we have given the interested parties more insights on the status of electronic invoicing today, which is positive regarding the transferability of this study (Denscombe, 2008).

3.5.4 Objectivity

In order to get trustworthy data, in the study, the three authors of this thesis have tried to be as objective as possible. We have tried to not take into account our own values and beliefs when achieving the case studies. The objectivity is crucial for the study in order to reach conclusions (Denscombe, 2008), Which is something we have borne in mind from the beginning of the study in order to not be affected by information that may make us believe that one kind of solution is better than another when handling electronic invoices.

3.6 Delimitations

The thesis will cover both the theoretical parts within the theoretical framework as well as feelings and thoughts from the case studies regarding the thesis questions. Because of this, we will focus on challenges and outcomes that can be specific to different organizations and may therefore vary in the specific nature, but also what alternatives there is on the market and how organizations can be most beneficial when implementing an electronic invoicing system (Narayanan, Marucheck & Handfield, 2009). We are aware that the solutions that enable electronic invoices can also be used for other documents, this fact will be taken into account when writing the thesis.

The case studies will be made with organizations that are in the process of implementing or have implemented a system that enables electronic invoice handling. We have delimitated the study to the Scandinavian market to have a smaller scope in order to, as we argue, perform a better analysis with stronger conclusions.